Advertisement

- United States

- /

- Electric Utilities

- /

- NasdaqGS:XEL

How Investors May Respond To Xcel Energy (XEL) Announcing a $60 Billion Spending Plan Amid Margin Pressure

Simply Wall St

Reviewed by Sasha Jovanovic

- Xcel Energy recently announced at the EEI Financial Conference in Florida a US$60 billion five-year capital spending plan, as presented by Vice President of Corporate Development Justin Tomljanovic.

- This major investment announcement comes despite the company reporting shrinking margins, declining third-quarter earnings, and cautionary signals about its financial and regulatory outlook.

- We'll examine how concerns around Xcel Energy's ambitious capital plan and financial pressures could reshape the company's investment narrative.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 27 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Xcel Energy Investment Narrative Recap

To believe in Xcel Energy as a shareholder, you need confidence that the company’s multi-billion dollar grid and clean energy investments will ultimately translate into sustainable, regulated earnings growth, despite near-term headwinds. The recent US$60 billion capital spending plan doesn’t materially impact the most immediate catalyst: favorable regulatory approvals for planned projects, but it does heighten the current risk of shareholder dilution and further margin compression due to ongoing funding needs.

Among recent developments, Xcel’s third-quarter earnings release stands out: despite increased year-over-year revenue, net income and earnings per share both declined, reflecting the pressure on margins that is now compounded by larger capital obligations. This is particularly relevant as the company’s aggressive investment plans require both regulatory support and ongoing access to affordable capital, factors that remain sensitive catalysts for share performance heading into 2026.

On the flip side, investors should be aware that persistent equity issuances and high interest costs could leave existing shareholders facing diluted returns if...

Read the full narrative on Xcel Energy (it's free!)

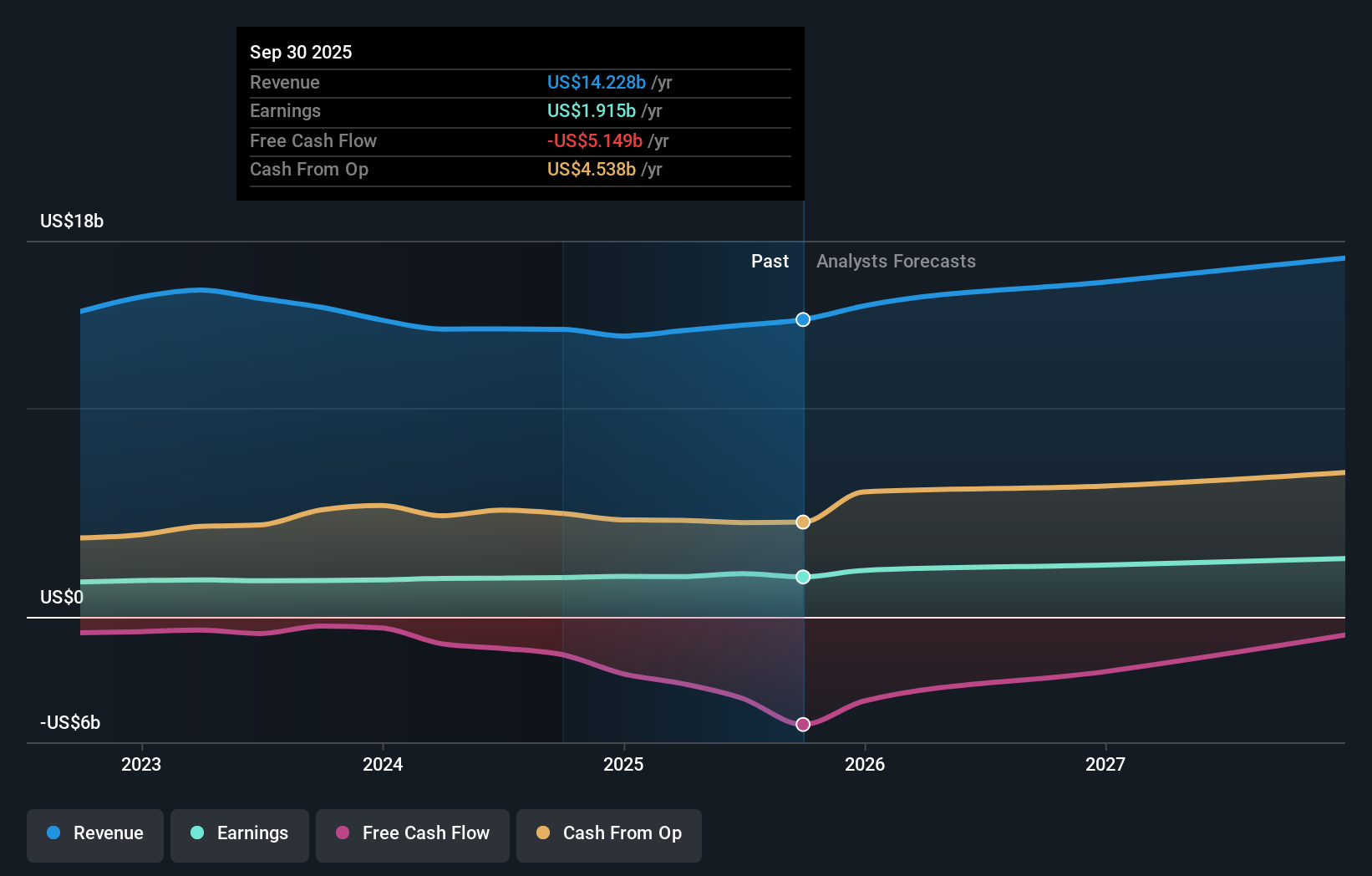

Xcel Energy's outlook anticipates $17.4 billion in revenue and $2.9 billion in earnings by 2028. This scenario is based on a projected 7.6% annual revenue growth and a $0.8 billion increase in earnings from the current $2.1 billion level.

Uncover how Xcel Energy's forecasts yield a $88.35 fair value, a 9% upside to its current price.

Exploring Other Perspectives

Three members of the Simply Wall St Community estimated Xcel Energy’s fair value between US$65.71 and US$88.35. With ambitious capital spending plans raising the potential for dilution, be sure to consider this range of opinions and explore several viewpoints.

Explore 3 other fair value estimates on Xcel Energy - why the stock might be worth 19% less than the current price!

Build Your Own Xcel Energy Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Xcel Energy research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Xcel Energy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Xcel Energy's overall financial health at a glance.

Want Some Alternatives?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 37 best rare earth metal stocks of the very few that mine this essential strategic resource.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:XEL

Xcel Energy

Through its subsidiaries, engages in the generation, purchasing, transmission, distribution, and sale of electricity in the United States.

Average dividend payer with questionable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor