- United States

- /

- Gas Utilities

- /

- NasdaqGM:RGCO

RGC Resources' (NASDAQ:RGCO) Upcoming Dividend Will Be Larger Than Last Year's

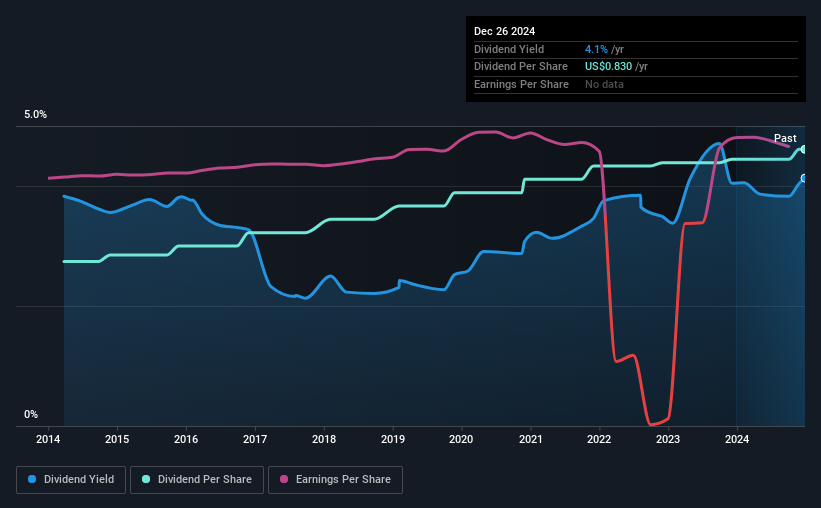

The board of RGC Resources, Inc. (NASDAQ:RGCO) has announced that it will be paying its dividend of $0.2075 on the 1st of February, an increased payment from last year's comparable dividend. This takes the annual payment to 4.1% of the current stock price, which is about average for the industry.

See our latest analysis for RGC Resources

RGC Resources' Payment Could Potentially Have Solid Earnings Coverage

We like a dividend to be consistent over the long term, so checking whether it is sustainable is important. Based on the last payment, RGC Resources' earnings were much higher than the dividend, but it wasn't converting those earnings into cash flow. Since a dividend means the company is paying out cash to investors, this could prove to be a problem in the future.

Over the next year, EPS could expand by 1.2% if recent trends continue. If the dividend continues on this path, the payout ratio could be 73% by next year, which we think can be pretty sustainable going forward.

RGC Resources Has A Solid Track Record

The company has been paying a dividend for a long time, and it has been quite stable which gives us confidence in the future dividend potential. The dividend has gone from an annual total of $0.493 in 2014 to the most recent total annual payment of $0.83. This means that it has been growing its distributions at 5.3% per annum over that time. Companies like this can be very valuable over the long term, if the decent rate of growth can be maintained.

RGC Resources May Find It Hard To Grow The Dividend

Some investors will be chomping at the bit to buy some of the company's stock based on its dividend history. Although it's important to note that RGC Resources' earnings per share has basically not grown from where it was five years ago, which could erode the purchasing power of the dividend over time. Growth of 1.2% may indicate that the company has limited investment opportunity so it is returning its earnings to shareholders instead. This isn't necessarily bad, but we wouldn't expect rapid dividend growth in the future.

In Summary

Overall, we always like to see the dividend being raised, but we don't think RGC Resources will make a great income stock. With cash flows lacking, it is difficult to see how the company can sustain a dividend payment. We would probably look elsewhere for an income investment.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. For example, we've identified 4 warning signs for RGC Resources (2 are concerning!) that you should be aware of before investing. Is RGC Resources not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:RGCO

RGC Resources

Through its subsidiaries, operates as an energy services company.

Average dividend payer with acceptable track record.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion