Advertisement

- United States

- /

- Marine and Shipping

- /

- NYSE:ZIM

ZIM Integrated Shipping Services (NYSE:ZIM) Faces Turkish Port Ban—A Fresh Look at Valuation After Regulatory Shakeup

Simply Wall St

Reviewed by Simply Wall St

If you’re holding ZIM Integrated Shipping Services (NYSE:ZIM) or considering it, you are probably closely watching today’s headlines. On August 22, a new Turkish regulation barred vessels with Israeli links—including ZIM’s fleet—from Turkish ports, forcing the company to reroute ships that were scheduled for Turkish calls. This sudden change is not just political theater; it directly affects ZIM’s operational plans and introduces a new variable into the company’s regional strategy. For investors, the main question is not just what changes on paper, but how this might impact revenue, routes, and long-term competitiveness.

This regulatory shakeup arrives as ZIM was beginning to show signs of improvement after a challenging year. Over the last twelve months, shares have gained 16 percent, representing a rebound after a year-to-date decline and a significant shift from the uneven results seen in recent earnings, where Q2 net income dropped sharply compared to last year. The company’s dividend payout also decreased, reflecting tighter financial conditions, but there are indications that momentum was beginning to build again. However, new operational obstacles like those in Turkey could make the path to recovery more challenging.

With these shifts in place, the question is whether the current market pricing of ZIM Integrated Shipping Services reflects just a short-term risk, or if there could be a potential long-term opportunity.

Most Popular Narrative: 1.7% Overvalued

According to community narrative, ZIM Integrated Shipping Services is considered slightly overvalued based on analysts' projections of future earnings and margins. These projections are influenced by challenging industry trends and regulatory headwinds.

"The projected imposition of a new port charge on Chinese-made vessels, if enacted, could increase operational costs significantly. This could affect net margins, as the company might need to undertake costly logistical adjustments or face higher port fees. The potential for a trade war and tariff increases between the U.S. and several key trading partners poses a risk of reduced shipping volumes and disrupted trade routes. This could negatively impact revenue as global trade patterns shift."

What is the real story behind this valuation? The narrative suggests rapidly shrinking profitability and a dramatic reset in future earnings multiples, but the exact assumptions may be surprising. Are you interested in learning about the bold analyst forecasts and the one critical financial shift that could change everything? Discover the numbers the consensus is considering and see if you agree with their view of ZIM’s future.

Result: Fair Value of $14.23 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, a modern and fuel-efficient fleet, or additional gains in shipping volumes, could boost margins and challenge the prevailing view that the company is overvalued.

Find out about the key risks to this ZIM Integrated Shipping Services narrative.Another View: What Does Our DCF Model Say?

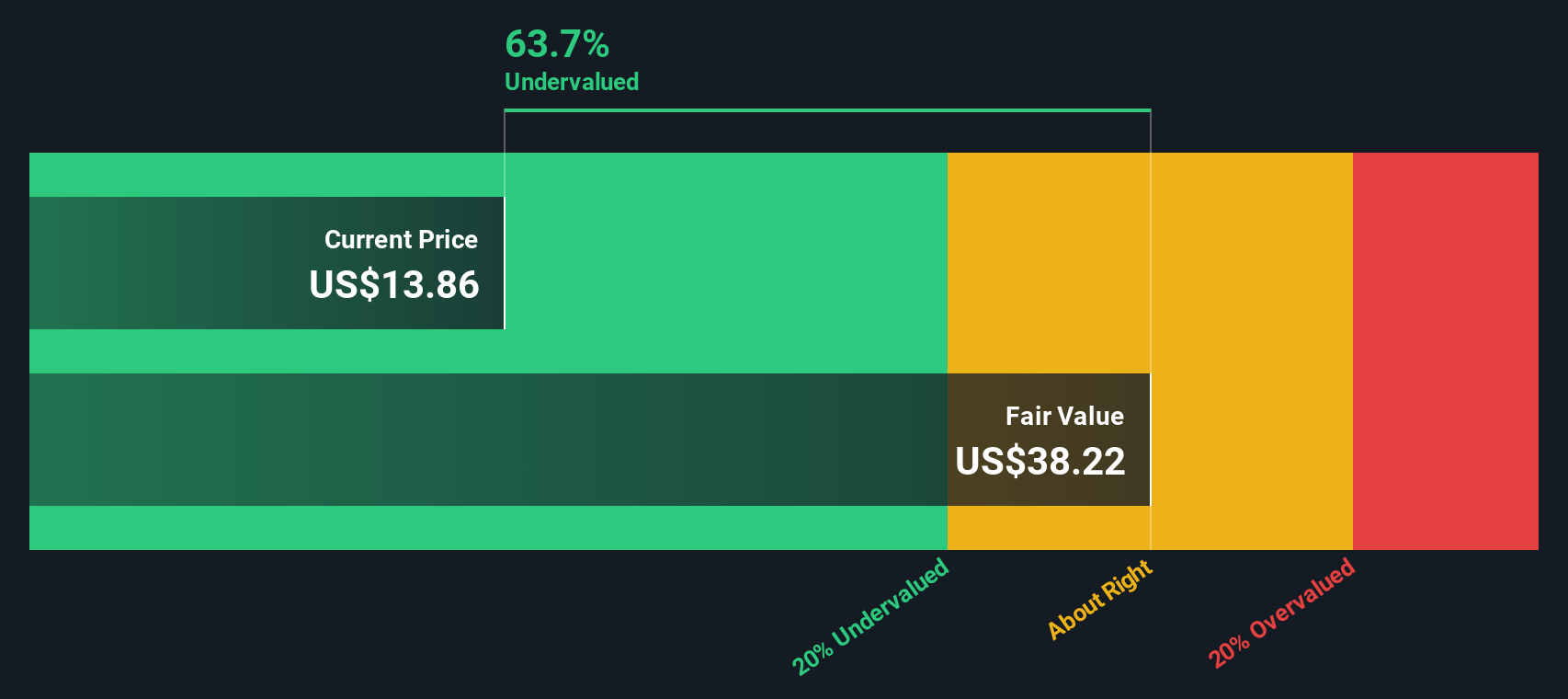

While the community focuses on earnings and future multiples for valuation, our SWS DCF model presents a very different perspective. It suggests ZIM is significantly undervalued if you trust the discounted cash flow calculations and assumptions. Which outlook aligns more with your view?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out ZIM Integrated Shipping Services for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own ZIM Integrated Shipping Services Narrative

If you see things differently or want to dive into the numbers on your own terms, it's quick and straightforward to build your own view in just a few minutes. Do it your way

A great starting point for your ZIM Integrated Shipping Services research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Staying ahead of the market means being open to fresh opportunities. Don’t let your portfolio miss out on the next big trend. Set your sights on stocks with game-changing potential using the Simply Wall Street Screener. Here’s where you can take action right now:

- Pinpoint companies reimagining healthcare by tapping into breakthroughs with healthcare AI stocks.

- Lock in the advantage of reliable cash flow and attractive yields. See which firms offer impressive payouts through dividend stocks with yields > 3%.

- Spot value-packed stocks trading below their worth and seize the best price potential with undervalued stocks based on cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if ZIM Integrated Shipping Services might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:ZIM

ZIM Integrated Shipping Services

Provides container shipping and related services in Israel and internationally.

Undervalued with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Defense AI: A Robotic Response to America’s Security Gaps

Fair Value US$12.00|51.2% undervalued

MA

Community Contributor

Figma (FIG): The S&P 500’s Design Standard Turning Into an All-in-One Platform

Fair Value US$65.70|6.7% overvalued

TI

Community Contributor

Sleep Cycle's Revenue Set to Rise 10% with Strong Revenue Model

Fair Value SEK 38.04|24.6% undervalued

MA

Community Contributor

Has JB Hi-Fi Lost Its Point of Difference?

Fair Value AU$76.00|53.6% overvalued

RO

Community Contributor