Advertisement

- United States

- /

- Marine and Shipping

- /

- NYSE:ZIM

New Forecasts: Here's What Analysts Think The Future Holds For ZIM Integrated Shipping Services Ltd. (NYSE:ZIM)

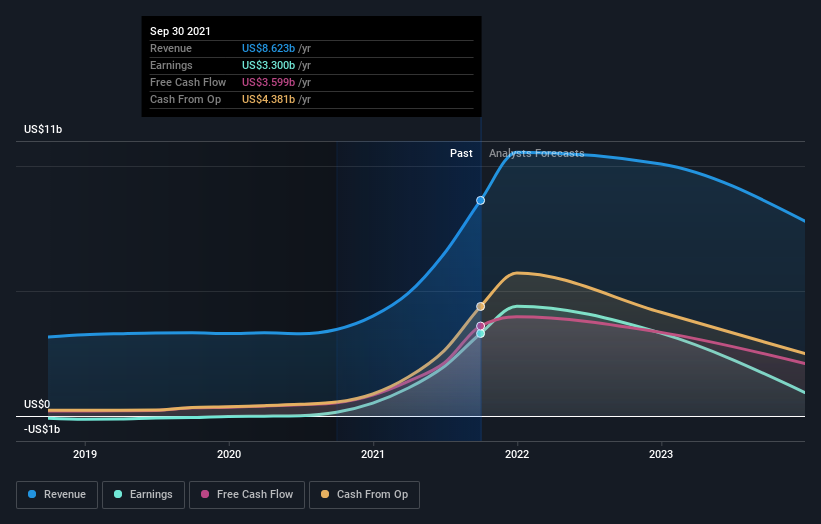

ZIM Integrated Shipping Services Ltd. (NYSE:ZIM) shareholders will have a reason to smile today, with the analysts making substantial upgrades to next year's statutory forecasts. Consensus estimates suggest investors could expect greatly increased statutory revenues and earnings per share, with analysts modelling a real improvement in business performance. ZIM Integrated Shipping Services has also found favour with investors, with the stock up a remarkable 13% to US$65.41 over the past week. Could this upgrade be enough to drive the stock even higher?

Following the upgrade, the latest consensus from ZIM Integrated Shipping Services' six analysts is for revenues of US$11b in 2022, which would reflect a major 22% improvement in sales compared to the last 12 months. Statutory earnings per share are forecast to be US$27.53, approximately in line with the last 12 months. Prior to this update, the analysts had been forecasting revenues of US$9.4b and earnings per share (EPS) of US$20.83 in 2022. So we can see there's been a pretty clear increase in analyst sentiment in recent times, with both revenues and earnings per share receiving a decent lift in the latest estimates.

View our latest analysis for ZIM Integrated Shipping Services

It will come as no surprise to learn that the analysts have increased their price target for ZIM Integrated Shipping Services 8.5% to US$75.58 on the back of these upgrades. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. The most optimistic ZIM Integrated Shipping Services analyst has a price target of US$90.00 per share, while the most pessimistic values it at US$43.04. Note the wide gap in analyst price targets? This implies to us that there is a fairly broad range of possible scenarios for the underlying business.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the ZIM Integrated Shipping Services' past performance and to peers in the same industry. The period to the end of 2022 brings more of the same, according to the analysts, with revenue forecast to display 17% growth on an annualised basis. That is in line with its 19% annual growth over the past five years. Compare this with the broader industry, which analyst estimates (in aggregate) suggest will see revenues grow 2.0% annually. So although ZIM Integrated Shipping Services is expected to maintain its revenue growth rate, it's definitely expected to grow faster than the wider industry.

The Bottom Line

The biggest takeaway for us from these new estimates is that analysts upgraded their earnings per share estimates, with improved earnings power expected for next year. Fortunately, analysts also upgraded their revenue estimates, and our data indicates sales are expected to perform better than the wider market. With a serious upgrade to expectations and a rising price target, it might be time to take another look at ZIM Integrated Shipping Services.

Still, the long-term prospects of the business are much more relevant than next year's earnings. We have estimates - from multiple ZIM Integrated Shipping Services analysts - going out to 2023, and you can see them free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

Valuation is complex, but we're here to simplify it.

Discover if ZIM Integrated Shipping Services might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:ZIM

ZIM Integrated Shipping Services

Provides container shipping and related services in Israel and internationally.

Excellent balance sheet with proven track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor