- United States

- /

- Logistics

- /

- NYSE:UPS

Is UPS Stock Offering Value After Recent Rebound and Ongoing Cost Cutting Efforts in 2025?

Reviewed by Bailey Pemberton

- If you are wondering whether United Parcel Service is a bargain or a value trap at current levels, you are not alone. Today we are going to unpack what the market might be missing.

- The stock has bounced about 1.1% over the last week and 10.5% over the past month, even though it is still down 17.6% year to date and 13.2% over the last year. This hints that sentiment may be starting to turn after a tough few years.

- Recently, investors have been reacting to ongoing cost cutting initiatives, network optimization efforts and strategic partnerships that aim to improve efficiency in a cooler e commerce environment. At the same time, macro headlines around global trade volumes and parcel demand have kept risk perceptions elevated. This helps explain why the share price recovery has been cautious rather than explosive.

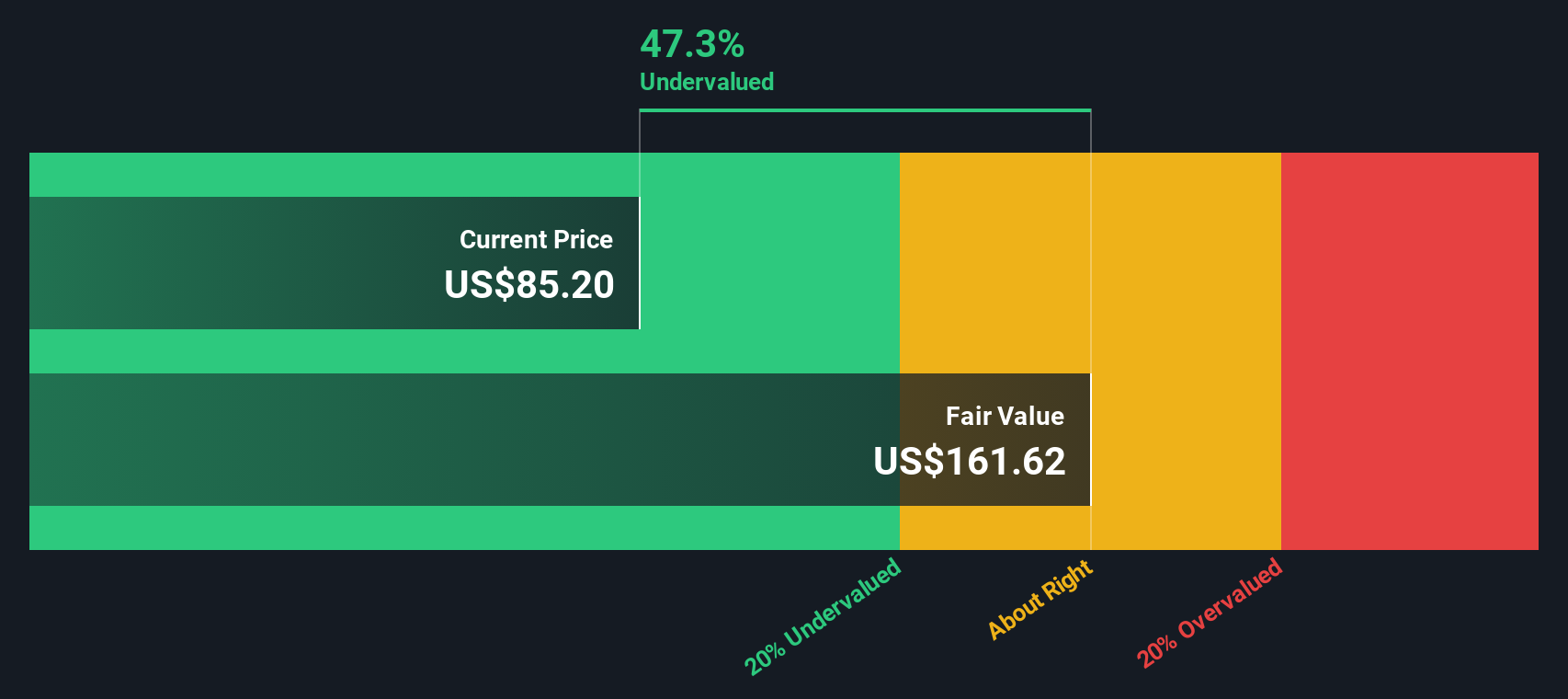

- Despite that backdrop, UPS currently scores a 5 out of 6 on our valuation checks, suggesting it screens as undervalued on most metrics. Next we will walk through the main valuation approaches we use, before finishing with a more holistic way to think about what the stock is really worth.

Find out why United Parcel Service's -13.2% return over the last year is lagging behind its peers.

Approach 1: United Parcel Service Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a business is worth today by projecting the cash it can generate in the future and discounting those cash flows back to today using an appropriate rate.

For United Parcel Service, the model starts with last twelve months free cash flow of roughly $3.7 billion. Analyst forecasts and Simply Wall St extrapolations point to free cash flow rising to about $6.2 billion by 2029, with further steady growth assumed over the following years. These projections are based on a 2 Stage Free Cash Flow to Equity framework that captures a faster growth phase followed by a more mature, slower growth period.

When these future cash flows are discounted back to today, the DCF model suggests an intrinsic value of about $135.30 per share. Compared to the current market price, this implies the stock is trading at roughly a 24.6% discount. This indicates that the market may be overly cautious about UPS cash generation prospects.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests United Parcel Service is undervalued by 24.6%. Track this in your watchlist or portfolio, or discover 916 more undervalued stocks based on cash flows.

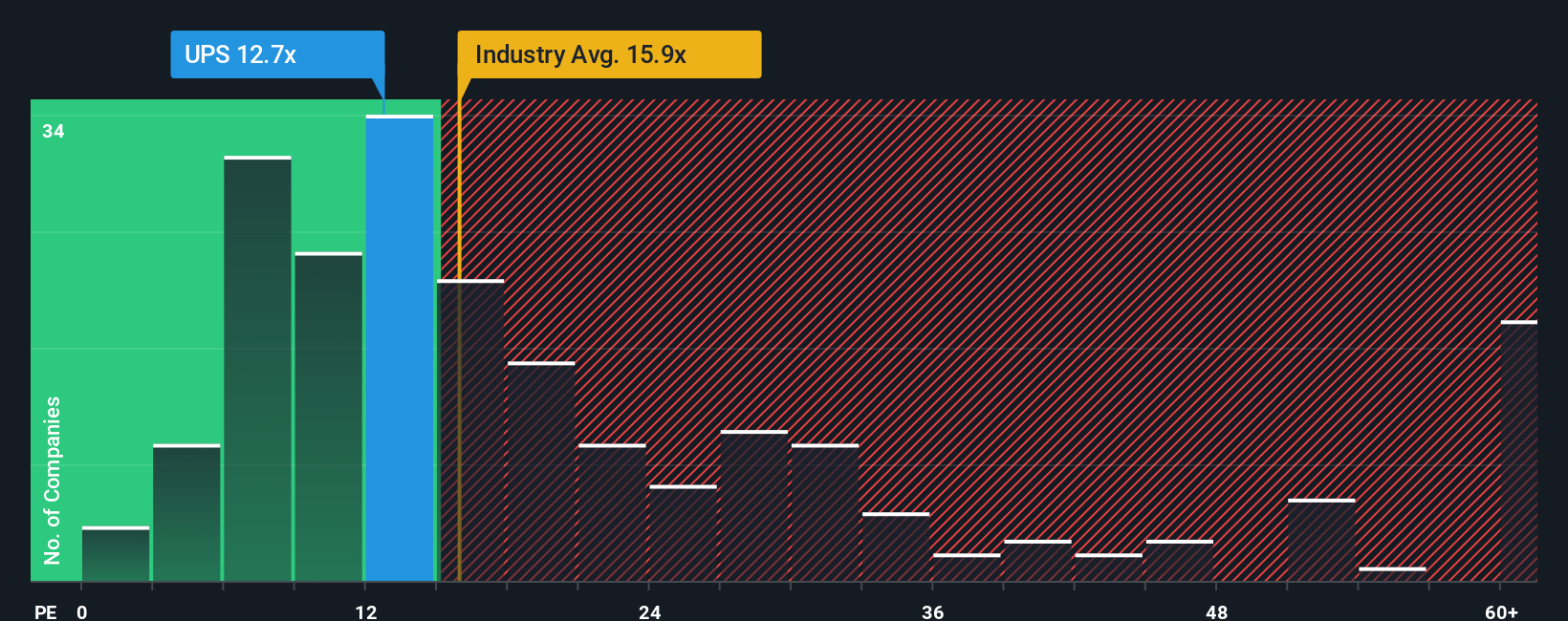

Approach 2: United Parcel Service Price vs Earnings

For a mature, profitable business like United Parcel Service, the price to earnings ratio is a useful way to gauge how much investors are paying for each dollar of current profits. It directly links the share price to the bottom line, which tends to be more stable than revenue or book value in established companies.

In general, faster expected earnings growth and lower perceived risk justify a higher normal PE ratio, while slower growth or higher uncertainty call for a lower multiple. UPS currently trades on about 15.7x earnings, which is slightly below the Logistics industry average of roughly 16.0x and well below the broader peer group average of around 21.6x. On the surface, that discount suggests the market is assigning relatively modest growth and some lingering risk to the story.

Simply Wall St also calculates a Fair Ratio of 19.5x for UPS, a proprietary estimate of what the PE should be given the company earnings growth profile, margins, industry, market cap and risk factors. This makes it more informative than a simple comparison with peers or sector averages, which can overlook important differences in quality and outlook. With the current PE of 15.7x sitting below the 19.5x Fair Ratio, the multiple analysis points to the shares being undervalued rather than fully priced.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1455 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your United Parcel Service Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives, a simple way to attach a clear story about UPS business to your own assumptions for future revenue, earnings, margins and therefore fair value, then compare that fair value to the current share price to decide whether you think it is a buy or a sell.

A Narrative on Simply Wall St links three things together: the company story you believe, the financial forecast that flows from that story, and the fair value estimate that those numbers justify. Because Narratives live inside the Community page used by millions of investors, they are easy to browse, create and tweak without needing a spreadsheet.

These Narratives also update dynamically as new information, like earnings releases or major news, comes in, so your view is never frozen in time. You can immediately see whether the gap between your fair value and the live UPS share price has widened or closed.

For example, one UPS Narrative on the platform currently implies a cautious fair value of about $95 per share, while another, more optimistic Narrative supports a fair value closer to $122. This shows how different but well structured perspectives can coexist and give you a clear framework for deciding where your own view sits.

For United Parcel Service, however, we will make it really easy for you with previews of two leading United Parcel Service Narratives:

🐂 United Parcel Service Bull Case

Fair value: $122.00 per share

Implied discount to fair value: 16.4%

Assumed revenue growth: 1.99%

- Argues that rapid automation, network reconfiguration and cost cutting will drive sustainable margin expansion and free cash flow above current consensus.

- Highlights healthcare logistics and shifting global trade routes as high margin growth drivers that diversify revenue and support a higher long term earnings base.

- Aligns with the bullish end of analyst targets, requiring confidence that UPS can lift margins, grow earnings to around $8.0 billion by 2028 and justify a higher PE multiple.

🐻 United Parcel Service Bear Case

Fair value: $95.21 per share

Implied downside from current price: 6.7%

Assumed revenue growth: 1.75%

- Focuses on rising costs, governance frictions and labor tensions that could keep profitability under pressure even as UPS restructures its network.

- Flags higher leverage and interest costs from recent debt issuance as a constraint on future flexibility if efficiency gains disappoint.

- Sees only modest upside from today share price to its $95.21 fair value, implying the stock is vulnerable if execution on Efficiency Reimagined or new partnerships falls short.

Do you think there's more to the story for United Parcel Service? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:UPS

United Parcel Service

A package delivery and logistics provider, offers transportation and delivery services.

Undervalued with adequate balance sheet and pays a dividend.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion