Advertisement

- United States

- /

- Airlines

- /

- NYSE:LUV

Can Southwest (LUV) Turn a Weaker 2025 Outlook into a Stronger Long-Term Revenue Model?

Simply Wall St

Reviewed by Sasha Jovanovic

- In early December 2025, Southwest Airlines cut its 2025 earnings outlook to about US$500 million after weaker demand during the U.S. government shutdown and higher fuel costs, even though bookings have since returned to earlier expectations.

- Ahead of launching assigned seating, extra-legroom options, and a broadened international network through partners like Condor in 2026, Southwest is reshaping both its revenue model and customer experience at the same time it absorbs these cost and demand shocks.

- We’ll now examine how the downgraded 2025 earnings outlook, driven by shutdown-related demand softness and fuel costs, reshapes Southwest’s investment narrative.

We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Southwest Airlines Investment Narrative Recap

To own Southwest today, you need to believe it can restore earnings power while overhauling its product and pricing. The cut to 2025 EBIT guidance to about US$500 million sharpens focus on execution: the key near term catalyst is monetizing assigned and premium seating in early 2026, while the biggest risk is that softer or choppier demand and higher fuel costs keep squeezing margins longer than expected. The latest guidance change does not remove that risk, it simply makes it more visible.

Among the recent announcements, the new Condor partnership stands out as most relevant. It expands Southwest’s role as a feeder for transatlantic traffic just as the airline shifts to assigned and extra legroom seating from January 27, 2026, giving it more ways to price seats and test whether these product upgrades can offset cost pressure and support the earnings recovery investors are watching for.

But even if bookings hold up, investors should still be aware of how exposed Southwest is to fuel price swings and...

Read the full narrative on Southwest Airlines (it's free!)

Southwest Airlines’ narrative projects $32.6 billion revenue and $1.9 billion earnings by 2028. This assumes 5.9% yearly revenue growth and an earnings increase of about $1.5 billion from $392.0 million today.

Uncover how Southwest Airlines' forecasts yield a $34.23 fair value, a 10% downside to its current price.

Exploring Other Perspectives

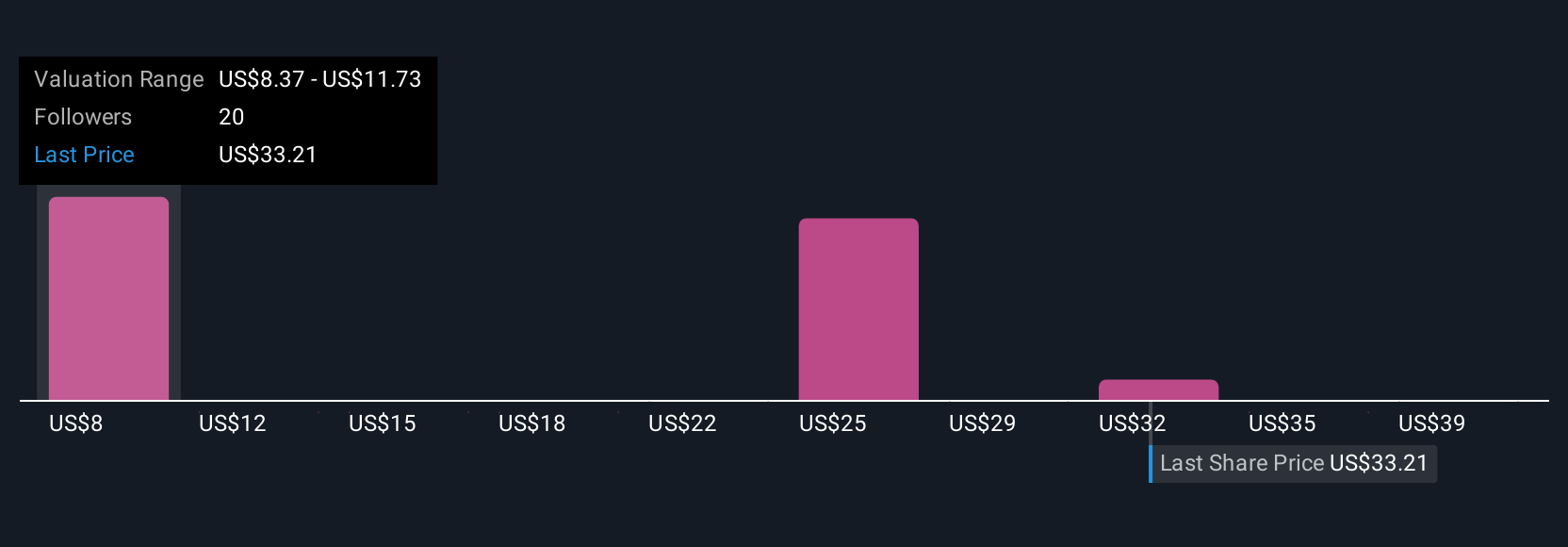

Seven Simply Wall St Community valuations for Southwest span roughly US$8 to US$46 per share, showing how far apart individual views can be. As you weigh those opinions, remember that the airline’s earnings reset to about US$500 million of 2025 EBIT and its reliance on new product initiatives put real focus on how much pricing power it can actually achieve.

Explore 7 other fair value estimates on Southwest Airlines - why the stock might be worth less than half the current price!

Build Your Own Southwest Airlines Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Southwest Airlines research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Southwest Airlines research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Southwest Airlines' overall financial health at a glance.

Searching For A Fresh Perspective?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:LUV

Southwest Airlines

Operates as a passenger airline company that provides scheduled air transportation services in the United States and near-international markets.

Reasonable growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

65 followersusers have followed this narrative

7 commentsusers have commented on this narrative

19 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

IN

IncomeAssets on Magma Silver ·

Silver's Breakout to over $50US will make Magma’s future shine with drill sampling returning 115g/t Silver and 2.3 g/t Gold at its Peru Mine

Fair Value:CA$0.3534.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on SEGRO ·

SEGRO's Revenue to Rise 14.7% Amidst Optimistic Growth Plans

Fair Value:UK£9.3924.7% undervalued

0 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PI

PicaCoder on Microsoft ·

After the AI Party: A Sobering Look at Microsoft's Future

Fair Value:US$42015.0% overvalued

62 followersusers have followed this narrative

12 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

118 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

958 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

65 followersusers have followed this narrative

7 commentsusers have commented on this narrative

19 likesusers have liked this narrative