Advertisement

- United States

- /

- Airlines

- /

- NasdaqGS:JBLU

What JetBlue Airways (JBLU)'s Route Expansion and A320 Groundings Reveal About Its Risk-Reward Tradeoff

Simply Wall St

Reviewed by Sasha Jovanovic

- In recent days, JetBlue Airways has outlined a wave of network expansions, from new spring break routes out of Fort Lauderdale to added Northeast–Florida and Puerto Rico services, while also cutting its fourth-quarter outlook after hurricane disruptions, FAA-mandated Airbus A320 groundings, and government shutdown-related cancellations pushed it toward an adjusted loss.

- The combination of growth-focused route additions and weather- and regulator-driven operational headwinds underscores how JetBlue is simultaneously investing in key leisure markets and absorbing higher near-term costs and capacity constraints.

- We’ll now examine how the FAA-driven A320 groundings and resulting cost pressures influence JetBlue’s existing investment narrative.

AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

JetBlue Airways Investment Narrative Recap

To own JetBlue today, you need to believe the airline can turn improving leisure demand and network optimization into sustainable profits despite recent losses and a relatively new management team. The A320 groundings and Q4 outlook cut primarily reinforce the existing near term risks around cost pressure, capacity limits and already thin visibility into demand, rather than creating a new, separate issue for the story.

Among the latest announcements, JetBlue’s expanded Florida network from New York and Boston to Daytona Beach stands out as closely tied to the current investment case, as it leans into resilient Northeast to Florida leisure demand while its A220 deployment highlights ongoing fleet simplification efforts that could matter for future unit costs and margins.

But while growth in Florida and Puerto Rico looks appealing, investors should be aware that rising labor and fuel costs, combined with...

Read the full narrative on JetBlue Airways (it's free!)

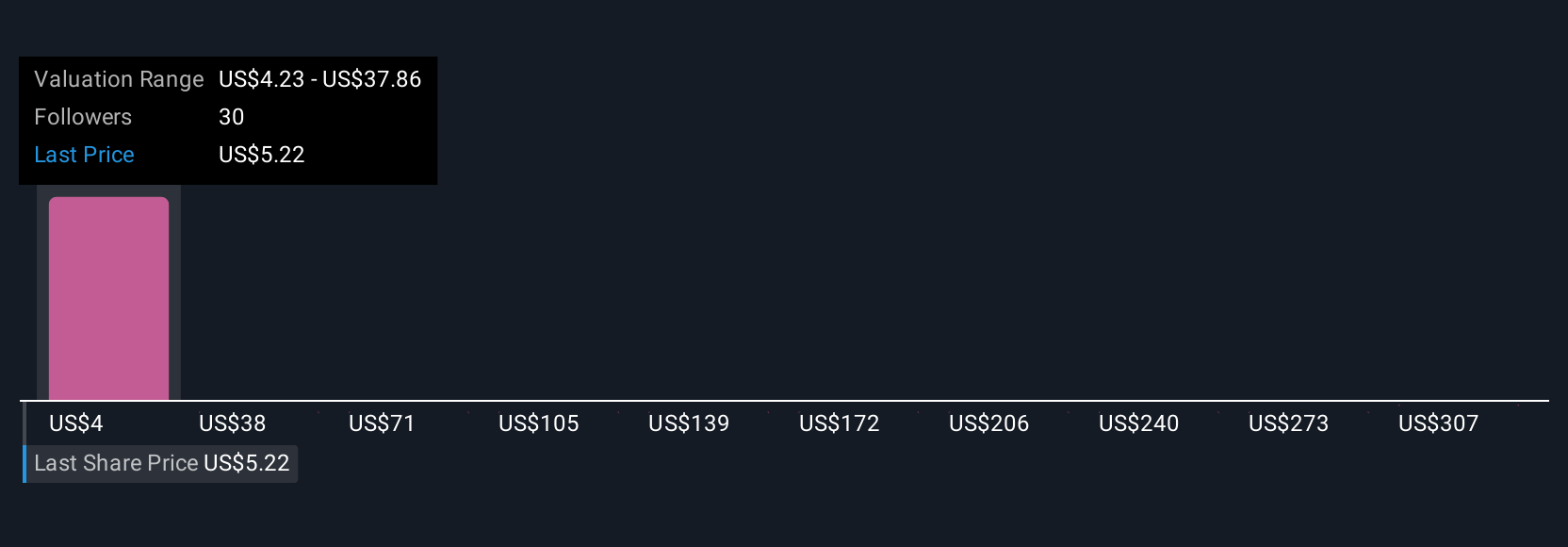

JetBlue Airways’ narrative projects $10.6 billion revenue and $728.0 million earnings by 2028. This requires 5.1% yearly revenue growth and an earnings increase of about $1.1 billion from $-386.0 million today.

Uncover how JetBlue Airways' forecasts yield a $4.65 fair value, in line with its current price.

Exploring Other Perspectives

Eight members of the Simply Wall St Community currently place JetBlue’s fair value anywhere between US$3 and US$340.49, underlining how far apart individual expectations can be. When you weigh those views against JetBlue’s ongoing exposure to higher non fuel unit costs and limited capacity growth, it becomes even more important to compare several independent perspectives before forming your own view.

Explore 8 other fair value estimates on JetBlue Airways - why the stock might be a potential multi-bagger!

Build Your Own JetBlue Airways Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your JetBlue Airways research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free JetBlue Airways research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate JetBlue Airways' overall financial health at a glance.

Seeking Other Investments?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- This technology could replace computers: discover 27 stocks that are working to make quantum computing a reality.

- Find companies with promising cash flow potential yet trading below their fair value.

- We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:JBLU

Fair value with minimal risk.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

50 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$247.5% overvalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

IN

IncomeAssets on Pulse Seismic ·

Watch Pulse Seismic Outperform with 13.6% Revenue Growth in the Coming Years

Fair Value:CA$4.4729.5% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$482.8% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6410.8% overvalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3926.8% undervalued

957 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

AN

AnalystConsensusTarget on Alphabet ·

GOOGL: AI Platform Expansion And Cloud Demand Will Support Durable Performance Amid Competitive Pressures

Fair Value:US$323.71.9% undervalued

1341 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative