Does Verizon Offer Long Term Value After Recent 5G Investments And Mixed Share Price Performance?

Reviewed by Bailey Pemberton

- If you have ever wondered whether Verizon Communications is quietly turning into a value play rather than just a slow and steady dividend name, you are in the right place.

- Despite a soft patch in the short term, with the stock down around 2% over the last week and 3% over the last month, Verizon is still up roughly 7% over the past year and 27.4% over 3 years. This hints that sentiment has been gradually improving, even if the year to date move of about 0.6% lower looks flat.

- Behind these moves, investors have been paying close attention to Verizon's ongoing 5G network investments, debt reduction efforts, and subscriber trends, particularly in its wireless and broadband businesses. At the same time, regulatory developments and competitive shifts in the US telecom landscape have kept risk perceptions in flux. This helps explain why the stock has not moved in a straight line.

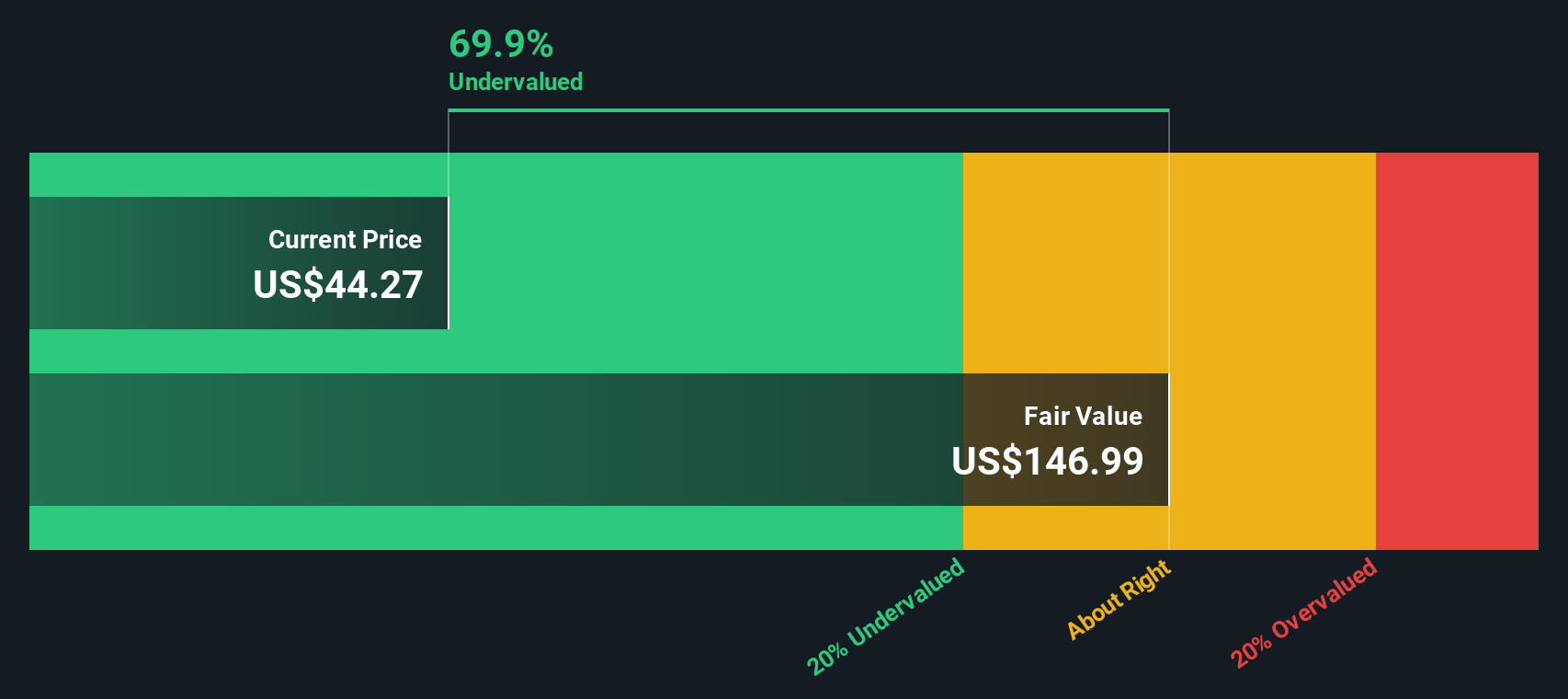

- On our framework, Verizon currently scores a 4/6 valuation check, suggesting the market may still be underpricing parts of the story. Next, we will unpack what that means across different valuation methods, before finishing with a more intuitive way to think about what Verizon is really worth.

Find out why Verizon Communications's 7.0% return over the last year is lagging behind its peers.

Approach 1: Verizon Communications Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a business is worth today by projecting its future cash flows and discounting them back to the present using a required rate of return.

For Verizon Communications, the latest twelve month Free Cash Flow is about $17.0 billion, and analysts expect this to rise to roughly $23.4 billion by 2029. Beyond the first few analyst forecast years, Simply Wall St extends the projections using more modest growth assumptions, with estimated Free Cash Flow reaching around $28.1 billion by 2035.

When all of these future cash flows are discounted back and summed, the DCF model suggests an intrinsic value of about $99.54 per share. Compared with the current market price, this implies a discount of roughly 59.8%, indicating that the stock appears significantly undervalued on cash flow grounds.

This is a cash flow story that the market may not be fully pricing in yet.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Verizon Communications is undervalued by 59.8%. Track this in your watchlist or portfolio, or discover 899 more undervalued stocks based on cash flows.

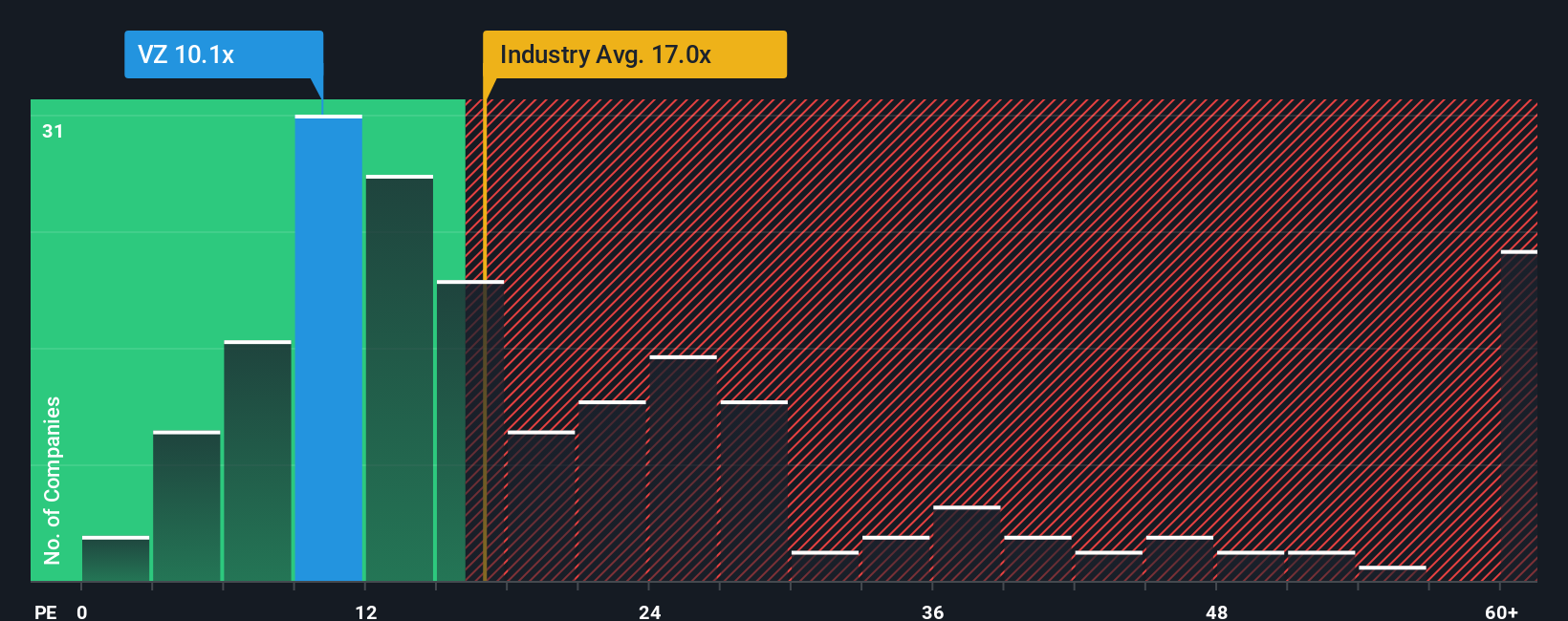

Approach 2: Verizon Communications Price vs Earnings

For a mature, consistently profitable business like Verizon Communications, the price to earnings ratio is a useful way to gauge how much investors are paying for each dollar of current earnings. It captures both what the company is earning today and how the market feels about its prospects.

In general, faster growing and lower risk companies tend to justify higher PE ratios, while slower growth or higher uncertainty usually means a lower, more conservative multiple is appropriate. Verizon currently trades on a PE of about 8.50x, which is slightly above the Telecom peer average of around 8.13x but well below the broader Telecom industry average of roughly 15.81x, suggesting the stock is priced more like a steady utility than a growth story.

Simply Wall St's Fair Ratio framework goes a step further by estimating what PE multiple Verizon should reasonably trade at, given its earnings growth outlook, profitability, industry, market cap and risk profile. On this basis, Verizon's Fair Ratio is 13.88x, materially higher than its current 8.50x. That gap indicates the market is still applying a meaningful discount relative to what these fundamentals imply.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1458 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Verizon Communications Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives, a simple way to connect your view of Verizon Communications' future (its story) with the numbers behind it. This is done by linking your assumptions about revenue, earnings and margins into a forecast that produces a Fair Value you can compare to the current share price. It is all available via an easy to use tool on Simply Wall St's Community page that updates automatically when new news or earnings arrive. One investor might build a bullish Verizon Narrative around rapid 5G and broadband expansion and arrive at a Fair Value near the top of the current range. Another might focus on debt, competition and market saturation and land closer to the low end, with each investor using the same framework to decide whether Verizon looks like a buy, a hold or a sell at today’s price.

Do you think there's more to the story for Verizon Communications? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:VZ

Verizon Communications

Through its subsidiaries, engages in the provision of communications, technology, information, and entertainment products and services to consumers, businesses, and governmental entities worldwide.

6 star dividend payer and good value.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion