Advertisement

Should AT&T's (T) Strong Subscriber Gains and Share Buyback Spur Investor Reassessment?

Simply Wall St

Reviewed by Sasha Jovanovic

- AT&T recently reported third quarter results, highlighting robust growth in postpaid phone and broadband subscribers along with renewed fiber and 5G investments, and completed a significant share buyback of over 52.79 million shares for US$1.5 billion between July and September 2025.

- The company also debuted Connectopia, an interactive AI-powered experience at a major sports venue, underscoring its commitment to next-generation connectivity and technology consumer engagement.

- We'll now look at how AT&T's strong subscriber growth and recent technology investments influence its long-term investment narrative.

These 15 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

AT&T Investment Narrative Recap

To be a shareholder in AT&T, you need to believe in the long-term value of expanding 5G and fiber networks, maintaining competitive subscriber growth, and disciplined capital returns amid an evolving market. While the company’s latest quarterly results underline gains in net income and subscriber additions, these do not appear to meaningfully alter the most important short-term catalyst (subscriber growth and retention) or address the prevailing risk of heightened competition pressuring margins.

Of the recent announcements, the multi-billion dollar share buyback stands out in relation to current events. While buybacks reflect management's confidence in future cash flows and can help support the stock, their material impact will ultimately depend on AT&T’s ability to deliver sustained operating improvements alongside subscriber and revenue growth.

In contrast, investors should be aware that expanded share repurchase plans may be helpful in the near-term, but if margin pressure accelerates, the longer-term impact on...

Read the full narrative on AT&T (it's free!)

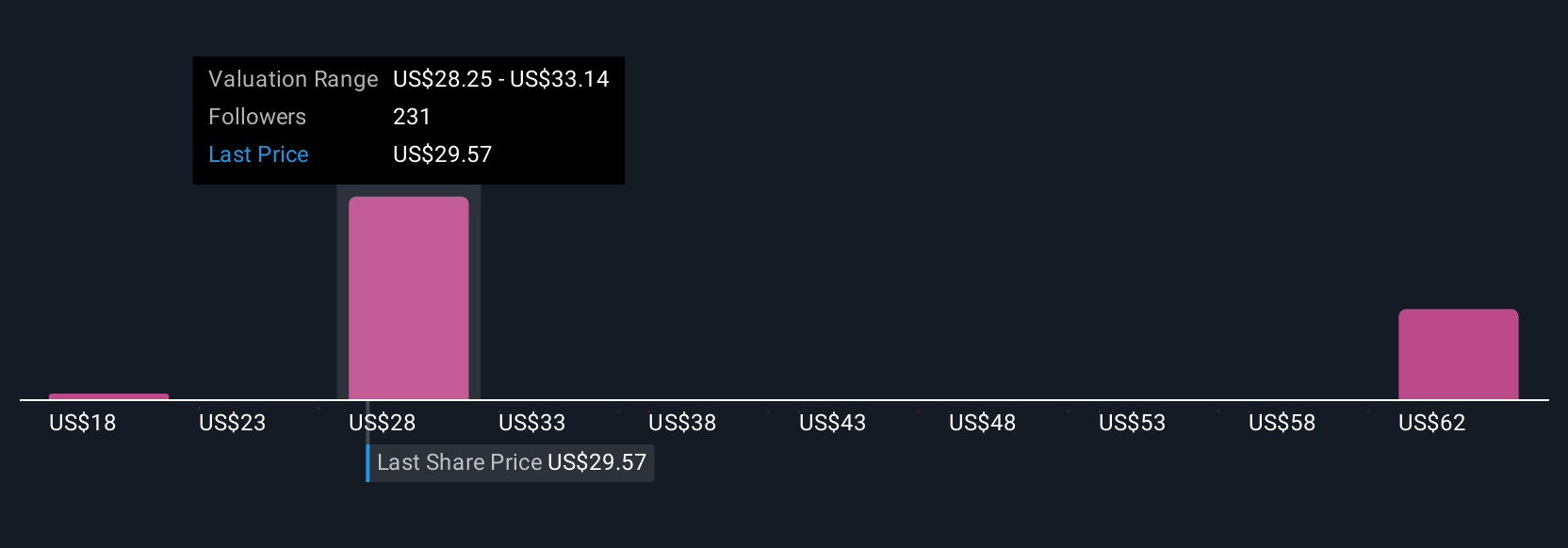

AT&T's narrative projects $130.6 billion in revenue and $17.0 billion in earnings by 2028. This requires 1.7% yearly revenue growth and a $4.3 billion earnings increase from current earnings of $12.7 billion.

Uncover how AT&T's forecasts yield a $30.99 fair value, a 23% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were forecasting AT&T earnings to reach US$17.6 billion and annual revenues of US$130.2 billion by 2028, driven by aggressive expansion in 5G and fiber while expecting significant cost savings from the transition away from legacy networks. This much more bullish view highlights how differently opinions can range, especially as recent news on subscriber growth and capital allocation could shift both risks and catalysts for the company. Comparing these perspectives can help you see where your own expectations might fit.

Explore 14 other fair value estimates on AT&T - why the stock might be worth 26% less than the current price!

Build Your Own AT&T Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your AT&T research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

- Our free AT&T research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate AT&T's overall financial health at a glance.

Seeking Other Investments?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Explore 27 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- We've found 17 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:T

Very undervalued with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|92.1% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor