Advertisement

- United States

- /

- Wireless Telecom

- /

- NYSE:AD

A Look At Array Digital Infrastructure (AD) Valuation After US$1.018b Spectrum Sale And Special Dividend

Array Digital Infrastructure (AD) is back in focus after closing a US$1.018b sale of spectrum licenses to AT&T and declaring a US$10.25 per share special cash dividend tied to that transaction.

See our latest analysis for Array Digital Infrastructure.

The AT&T spectrum deal and special dividend have arrived alongside a 17.38% 90 day share price return and a 29.40% 1 year total shareholder return, while the 3 year total shareholder return above 250% suggests recent momentum rather than fading performance.

If this kind of corporate action has you thinking more broadly about telecom and infrastructure opportunities, it could be a good moment to scan fast growing stocks with high insider ownership for other ideas gaining attention.

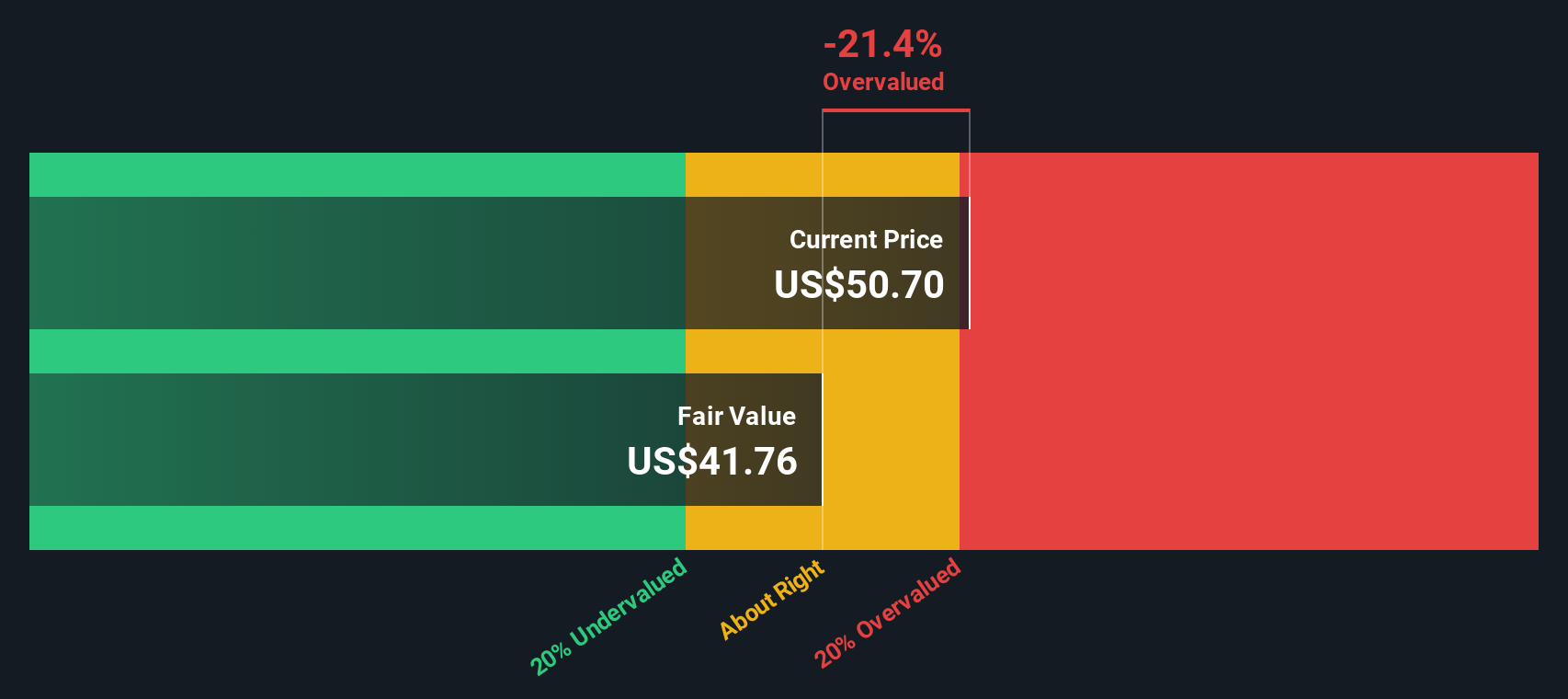

With the special dividend, a US$1.018b cash inflow and an intrinsic value estimate implying a 26% discount, the key question is simple: is Array still mispriced or is the market already baking in future growth?

Most Popular Narrative: 6.1% Overvalued

At a last close of US$57.80 versus a narrative fair value of US$54.50, the current price sits modestly above that fair value anchor, which hinges on very specific long term assumptions about revenue, margins and the earnings multiple.

The analysts have a consensus price target of $80.75 for United States Cellular based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $85.0, and the most bearish reporting a price target of just $72.0.

Curious what has to happen to revenue, profit margins and the future P/E to justify that higher fair value? The narrative leans heavily on a sharp earnings swing and a premium multiple that is usually reserved for faster growing sectors. If you want to see exactly how those assumptions stack up over the next few years, the full narrative lays the numbers out in black and white.

Result: Fair Value of $54.50 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the whole story could change if regulatory approvals for pending transactions stall or if competitive pressure from larger carriers continues to weigh on service revenues.

Find out about the key risks to this Array Digital Infrastructure narrative.

Another Take: DCF Points the Other Way

While the narrative model points to a 6.1% premium to its US$54.50 fair value, our DCF model tells a different story. In this view, Array Digital Infrastructure at US$57.80 trades about 25.6% below a US$77.66 fair value, raising the question of which set of assumptions you trust more.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Array Digital Infrastructure for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 876 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Array Digital Infrastructure Narrative

If you look at these numbers and reach a different conclusion, or prefer to test your own assumptions directly, you can build a tailored thesis in a few minutes using Do it your way.

A great starting point for your Array Digital Infrastructure research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Ready for more investment ideas?

If Array has sharpened your thinking, do not stop here, let the Simply Wall St Screener surface fresh opportunities that match the way you like to invest.

- Target potential mispricings by scanning these 876 undervalued stocks based on cash flows that line up with your own expectations on cash flow strength and pricing.

- Ride the growth of AI by reviewing these 24 AI penny stocks that could benefit from rising demand for data, automation and computing power.

- Tap into long term income themes by checking these 12 dividend stocks with yields > 3% that might suit a portfolio focused on regular cash returns.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:AD

Array Digital Infrastructure

Owns and operates shared wireless communications infrastructure in the United States.

Excellent balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0775.1% undervalued

121 followersusers have followed this narrative

1 commentusers have commented on this narrative

21 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9822.7% undervalued

39 followersusers have followed this narrative

0 commentsusers have commented on this narrative

32 likesusers have liked this narrative

KO

Kouj on CSL ·

CSL: The Dip Is the Opportunity

Fair Value:AU$1559.0% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative

GA

GavrielH on DHT Holdings ·

DHT Holdings, inc: Strait of Hormuz Risk Amidst US-Israel vs Iran Tensions Spikes VLCC Rates.

Fair Value:US$3653.2% undervalued

12 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

Recently Updated Narratives

VE

Vestra on VEON ·

VEON Ltd. (VEON): The Frontier "Digital Operator" and the 84% Hypergrowth Inflection

Fair Value:US$67.825.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on Salesforce ·

Salesforce (CRM): The "Agentic Work Unit" Revolution and the $50 Billion Capital Pivot

Fair Value:US$34143.5% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on NVIDIA ·

NVIDIA (NVDA): The "Agentic AI" Pivot and the $2 Billion Sovereign Cloud Alliance

Fair Value:US$237.524.1% undervalued

24 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.378.4% undervalued

53 followersusers have followed this narrative

3 commentsusers have commented on this narrative

27 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9822.7% undervalued

39 followersusers have followed this narrative

0 commentsusers have commented on this narrative

32 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59633.6% undervalued

1308 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

Trending Discussion

DA

daqui_luis on Corticeira Amorim S.G.P.S ·

Great analysis on a great and solid company with a dominant position in the Cork Market.

1

|0