Advertisement

- United States

- /

- Wireless Telecom

- /

- NasdaqGS:TMUS

T-Mobile (TMUS): Valuation in Focus After Earnings Beat, Higher Capex, and Investor Caution

Simply Wall St

Reviewed by Simply Wall St

T-Mobile US (TMUS) reported earnings and revenue ahead of expectations. However, its disclosure of a major impairment charge and a planned increase in capital spending for 2025 has stirred investor concern. Shares have lagged behind wireless rivals as sentiment responds to mixed signals.

See our latest analysis for T-Mobile US.

After beating earnings estimates, T-Mobile’s share price has failed to bounce, down 17% over the past three months and delivering a -14% total shareholder return for the year. Momentum has clearly faded despite upbeat news about subscriber gains, new digital tools, and customer perks. Investors are weighing the impact of higher spending and an industry that is getting more competitive.

If you’re eyeing what’s next for growth stocks, now is a great time to broaden your perspective and discover fast growing stocks with high insider ownership

With shares trading at a significant discount to analyst targets and the company posting steady subscriber growth, investors are left wondering if T-Mobile is now undervalued or if the market is already factoring in all future gains.

Most Popular Narrative: 24% Undervalued

T-Mobile US closed significantly below the narrative fair value estimate. This suggests fresh upside if the scenario plays out as projected by consensus. The narrative points to robust business catalysts and a valuation gap that is not reflected in the latest price trends.

Innovations such as the rollout of 5G Advanced and T-Satellite, along with enhancements in digital platforms like T-Life, signal operational improvements that could drive margin expansion and future earnings growth.

Could these technology bets power future earnings in ways the market has not fully priced in? The narrative’s numbers are built on bold projections for revenue, margins, and future share repurchases. Curious about which key financial metrics make this valuation tick? Delve deeper to uncover the driving forces behind this compelling valuation call.

Result: Fair Value of $275 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, risks remain, including potential industry-wide churn and competitive promotions. Either of these factors could pressure T-Mobile's future revenue growth and profitability.

Find out about the key risks to this T-Mobile US narrative.

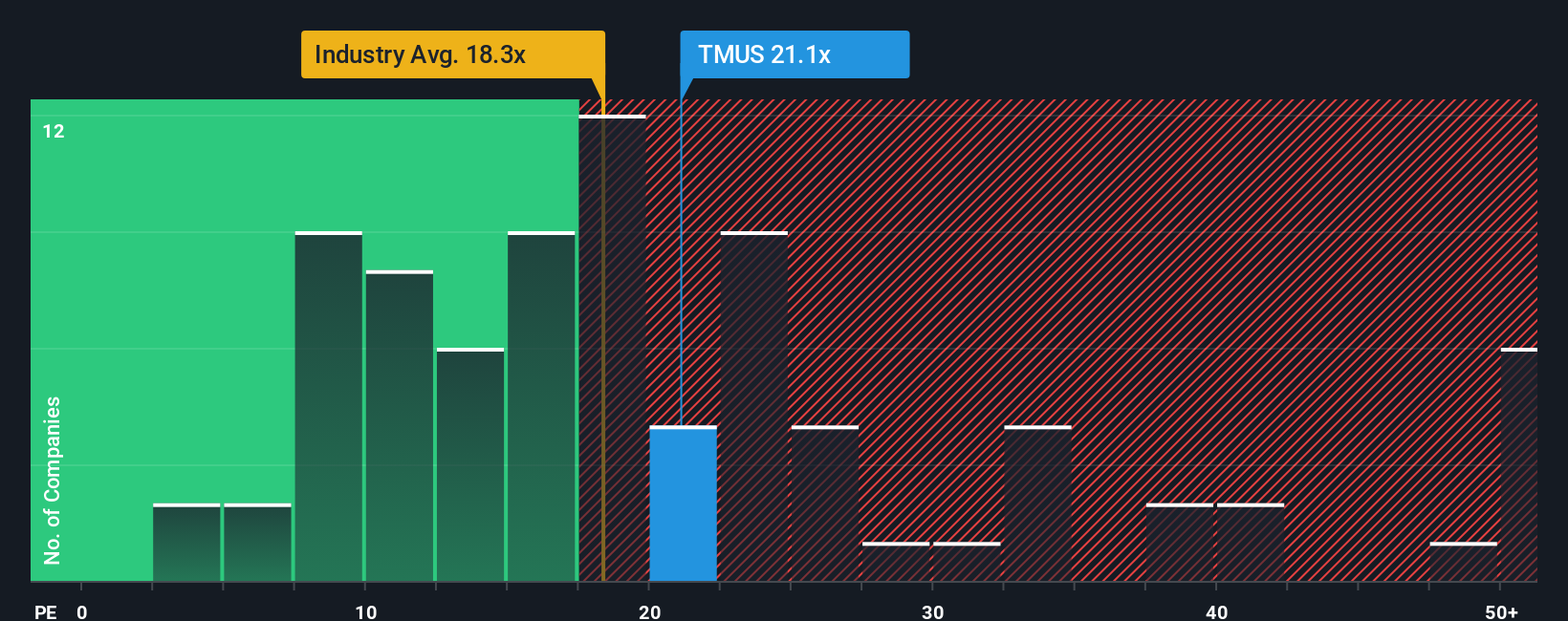

Another View: What Do Earnings Ratios Suggest?

Looking at typical earnings ratios gives a different perspective. T-Mobile is trading at 19.7 times earnings, which is higher than the industry average of 18.4 and well above the fair ratio of 16.5. This higher valuation hints at extra optimism, but does it create caution or signal opportunity if the market decides to catch up?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own T-Mobile US Narrative

If you think the numbers tell a different story or want to dig into the details yourself, you can create your own view in just a few minutes with Do it your way.

A great starting point for your T-Mobile US research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Level up your portfolio by tapping into stock trends you might be missing. The Simply Wall Street Screener spotlights new opportunities. See what could be next for you:

- Unlock potentially overlooked value by reviewing these 914 undervalued stocks based on cash flows and track equities trading below intrinsic estimates, primed for possible upside.

- Strengthen your search for steady returns by checking out these 15 dividend stocks with yields > 3% featuring companies with robust dividend yields exceeding 3%.

- Catch innovation waves on the frontier of artificial intelligence by scanning these 25 AI penny stocks with businesses positioned to benefit as AI reshapes industries.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if T-Mobile US might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:TMUS

T-Mobile US

Provides wireless communications services in the United States, Puerto Rico, and the United States Virgin Islands.

Good value with acceptable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CE

cementafriend on Constellation Energy ·

Constellation Energy Dividends and Growth

Fair Value:US$348.054.7% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KH

Khagani on CoreWeave ·

CoreWeave's Revenue Expected to Rocket 77.88% in 5-Year Forecast

Fair Value:US$11033.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PO

PortfolioPlus on Bisalloy Steel Group ·

Bisalloy Steel Group will shine with a projected profit margin increase of 12.8%

Fair Value:AU$6.7118.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

935 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

140 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative