Advertisement

- United States

- /

- Telecom Services and Carriers

- /

- NasdaqCM:SIFY

A Look At Sify Technologies (NasdaqCM:SIFY) Valuation After Recent Share Price Volatility

Sify Technologies (SIFY) has drawn attention after recent trading moves left the stock with a 1 day return of around an 8% decline and a 7 day return near a 10% decline, despite strong longer term figures.

See our latest analysis for Sify Technologies.

Despite the recent 1 day and 7 day share price declines, Sify Technologies still sits at a share price of US$13.34, with a 30 day share price return of 6.29% and a very large 1 year total shareholder return, hinting that short term volatility contrasts with stronger longer term sentiment.

If this kind of sharp move has your attention, it could be a good moment to see what else is moving in related areas. You can start with our screen of 33 AI infrastructure stocks.

With Sify Technologies trading at US$13.34 and sitting at a large discount to the US$22.00 analyst price target, the key question is whether the recent pullback signals a buying opportunity or if the market is already pricing in future growth.

Most Popular Narrative: 39.4% Undervalued

With Sify Technologies last closing at $13.34 against a most widely followed fair value estimate of $22, the current price sits well below that narrative anchor and puts the growth story under the spotlight.

Sify Technologies is investing in AI capabilities, likely leading to increased demand from enterprises seeking mature network, data center, and digital services. This is expected to impact revenue and earnings positively as AI workloads grow in India.

Curious what justifies nearly two thirds upside from here? The narrative leans heavily on rapid revenue expansion, margin improvement, and a premium future earnings multiple. The real surprise is how optimistic those earnings and profitability assumptions need to be to line up with that $22 fair value.

Result: Fair Value of $22 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the story could change if high SG&A and expansion costs keep margins under pressure, or if new data centers and AI driven demand ramp more slowly than expected.

Find out about the key risks to this Sify Technologies narrative.

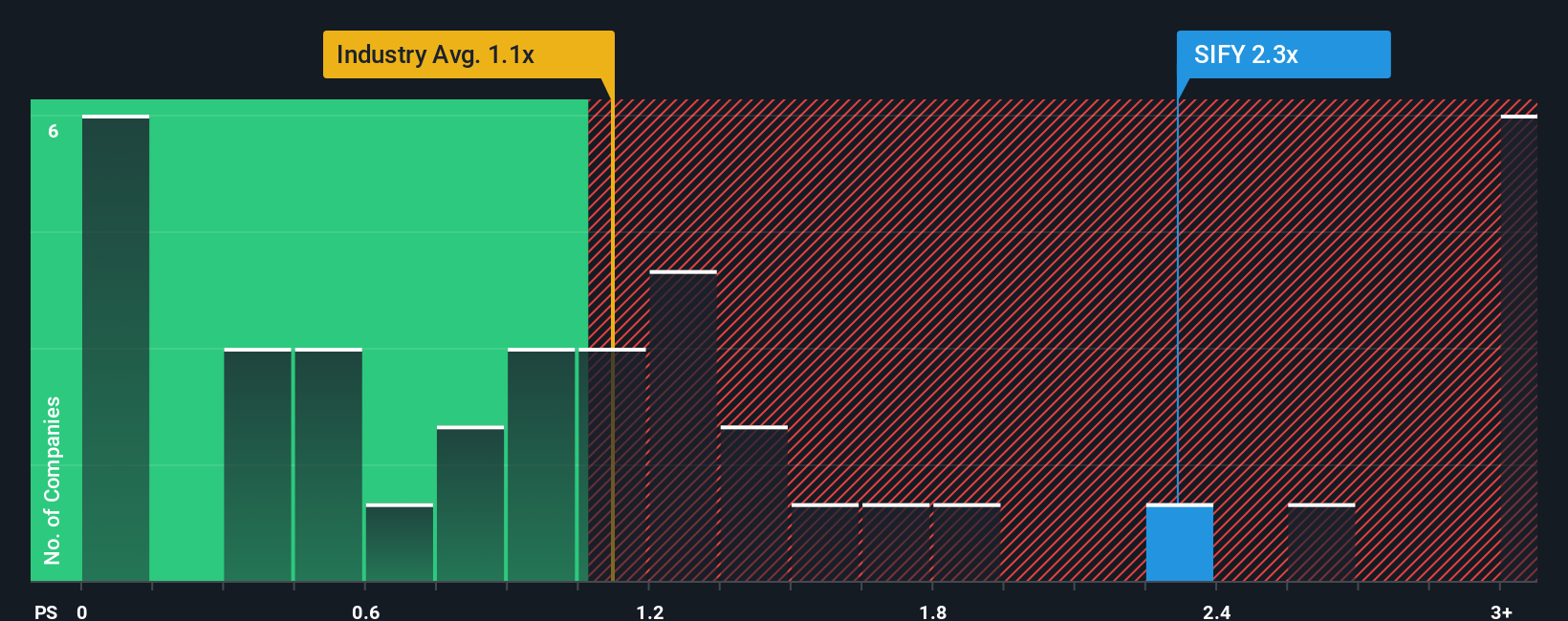

Another Angle: Price To Sales Tells A Different Story

Those fair value narratives point to Sify Technologies looking undervalued at $13.34, but the simple P/S check is far less generous. At about 2x sales, SIFY trades noticeably richer than the US Telecom industry at 1.1x, its peers at 1.2x, and even its own 1.8x fair ratio. This suggests limited margin for disappointment if growth or profitability assumptions fall short. So is the market already paying up for the AI and data center story before the profits arrive?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Sify Technologies Narrative

If you see the story differently or prefer to rely on your own analysis, you can assemble the numbers and build a complete view yourself in just a few minutes, then Do it your way.

A great starting point for your Sify Technologies research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If you are weighing up what to do next after looking at Sify Technologies, this is the moment to broaden your watchlist and compare fresh opportunities.

- Spot potential value plays early by scanning our list of screener containing 25 high quality undiscovered gems before they land on everyone else’s radar.

- Balance return potential with peace of mind by reviewing companies in the 81 resilient stocks with low risk scores that score well on our risk checks.

- Focus on quality at a sensible price by checking companies in the solid balance sheet and fundamentals stocks screener (46 results) that pair financial strength with consistent fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqCM:SIFY

Sify Technologies

Offers information and communication technology solutions and services in India and internationally.

High growth potential and overvalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

VA

valuebull on Eva Live ·

Is this the AI replacing marketing professionals?

Fair Value:US$7.4347.2% undervalued

55 followersusers have followed this narrative

0 commentsusers have commented on this narrative

12 likesusers have liked this narrative

SI

SimpleMan887 on GameStop ·

GameStop will ace the financial crisis wave with its strategic Bitcoin investment and cash reserves

Fair Value:US$22089.4% undervalued

41 followersusers have followed this narrative

2 commentsusers have commented on this narrative

19 likesusers have liked this narrative

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0778.3% undervalued

199 followersusers have followed this narrative

1 commentusers have commented on this narrative

28 likesusers have liked this narrative

YI

yiannisz on Hesai Group ·

The First Real Lidar Winner

Fair Value:US$27.0725.2% undervalued

3 followersusers have followed this narrative

1 commentusers have commented on this narrative

3 likesusers have liked this narrative

Recently Updated Narratives

FA

FA_Trader on Northern Solar Holdings Berhad ·

Northern Solar: Explosive earnings growth makes this solar story harder to ignore

Fair Value:RM 1.968.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TR

tripledub on SHAPE Australia ·

50% ROE in a Burning Building

Fair Value:AU$7.159.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.2541.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9829.9% undervalued

53 followersusers have followed this narrative

0 commentsusers have commented on this narrative

38 likesusers have liked this narrative

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3955.7% undervalued

40 followersusers have followed this narrative

3 commentsusers have commented on this narrative

41 likesusers have liked this narrative

RO

Robbo on Tesla ·

The academically fascinating Tesla

Fair Value:US$301.1k% overvalued

36 followersusers have followed this narrative

10 commentsusers have commented on this narrative

30 likesusers have liked this narrative