- United States

- /

- Telecom Services and Carriers

- /

- NasdaqGS:ASTS

AST SpaceMobile (ASTS): Revisiting Valuation After Volatile Performance and Shifting Investor Sentiment

Reviewed by Kshitija Bhandaru

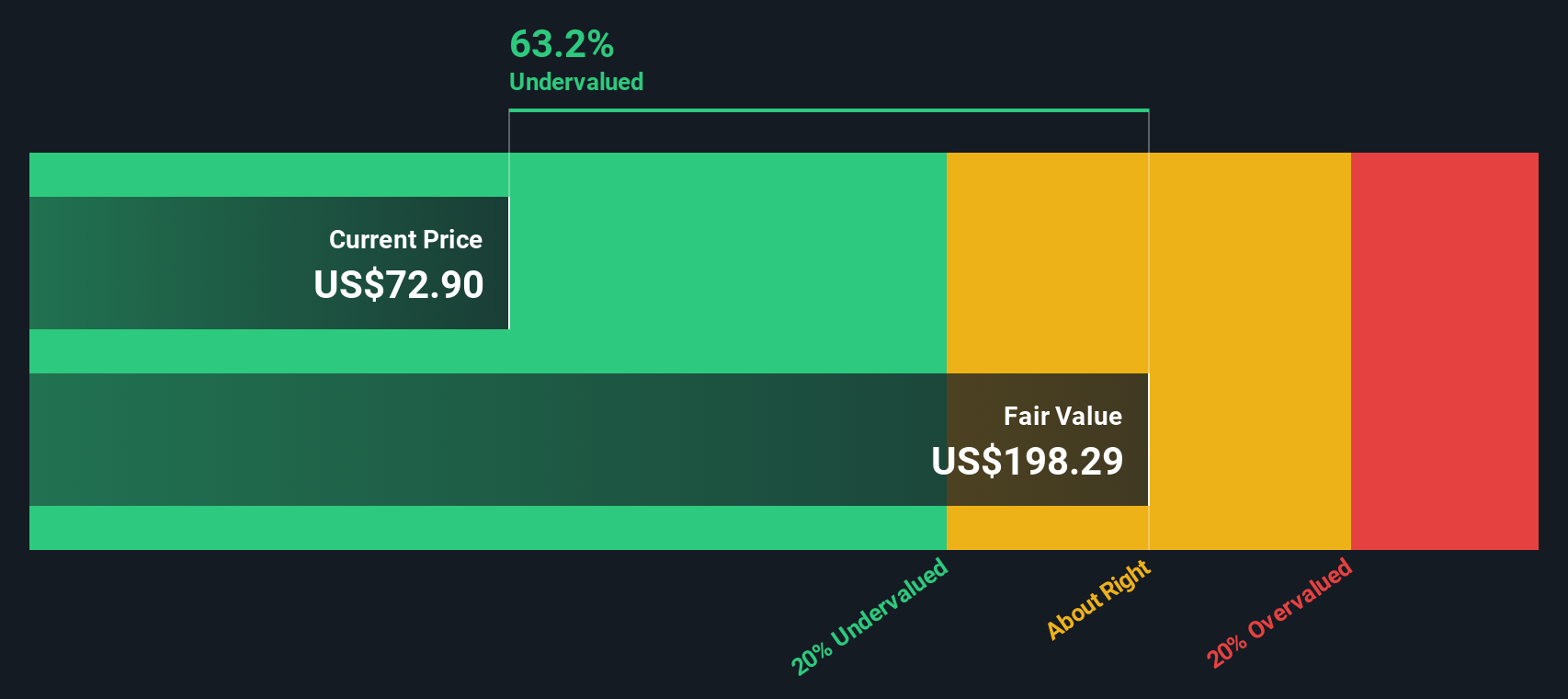

Price-to-Book of 15.2x: Is it justified?

Based on its price-to-book (P/B) ratio, AST SpaceMobile appears expensive compared to both the US telecom industry and its peers. The current P/B multiple stands at 15.2x, significantly above the industry average of 1.6x and the peer average of 3.9x. This suggests the market has assigned a high valuation relative to the company's net assets.

The price-to-book ratio focuses on how much investors are willing to pay for each dollar of a company’s net assets. In capital-intensive sectors such as telecom, this metric is often used to gauge whether a stock is trading at a premium or discount to its book value.

Such a high P/B ratio implies that investors expect substantial growth or business prospects that justify a premium. However, given AST SpaceMobile's current lack of profits and limited meaningful revenue, the valuation may reflect optimism about future potential rather than present fundamentals.

Result: Fair Value of $49.09 (OVERVALUED)

See our latest analysis for AST SpaceMobile.However, ongoing losses and premium valuation mean that any stumble in growth or execution could significantly challenge AST SpaceMobile's current momentum.

Find out about the key risks to this AST SpaceMobile narrative.Another View: SWS DCF Model Perspective

While the current valuation looks steep against industry averages, our DCF model offers a surprisingly different take. According to this method, AST SpaceMobile could actually be undervalued. Does this signal hidden opportunity or does it simply highlight uncertainty?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own AST SpaceMobile Narrative

If you see things differently or want to dig deeper into AST SpaceMobile’s story, you can quickly build your own perspective using the available data. Do it your way.

A great starting point for your AST SpaceMobile research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Smart investors never settle for just one opportunity. Catch new trends, uncover niche sectors, and tap into tomorrow’s biggest gainers using these powerful tools on Simply Wall St.

- Tap into the fast-growing world of secure digital payments and fintech innovation by checking out cryptocurrency and blockchain stocks.

- Unlock potential by finding companies leading breakthroughs in medical artificial intelligence and healthcare transformation through healthcare AI stocks.

- Spot high-yield opportunities and strengthen your portfolio income by searching for dividend stocks with yields > 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:ASTS

AST SpaceMobile

Designs and develops the constellation of BlueBird satellites in the United States.

Exceptional growth potential with excellent balance sheet.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion