- United States

- /

- Tech Hardware

- /

- NYSE:HPE

Does HPE's Advanced AI Networking Suite Signal a Shift in Its Automation Strategy? (HPE)

Reviewed by Simply Wall St

- Hewlett Packard Enterprise recently announced major enhancements to its HPE Juniper Networking portfolio, introducing advanced agentic AI and AIOps features for more proactive and autonomous network operations.

- A unique aspect of these innovations is the use of Marvis Minis, digital twins that simulate user experiences and enable predictive network optimization before real-time data is available.

- We'll explore how HPE's new AI-native troubleshooting and predictive capabilities could influence its ongoing investment narrative and future prospects.

Rare earth metals are the new gold rush. Find out which 29 stocks are leading the charge.

Hewlett Packard Enterprise Investment Narrative Recap

To be a Hewlett Packard Enterprise shareholder, you need confidence in the company's ability to drive growth through AI-powered innovation and its GreenLake cloud strategy, while navigating intense competition and evolving profit margins. The latest enhancements to the HPE Juniper Networking portfolio bring advanced AI-native troubleshooting and autonomous operations, but in the short term, these are unlikely to materially shift the main catalyst: approval and integration of the Juniper Networks acquisition, which is pivotal for potential synergies and future revenue progression. The most relevant recent announcement is the progress with the DOJ regarding HPE's acquisition of Juniper Networks. This remains a key development, as regulatory review continues to be the single most significant near-term hurdle for HPE’s investment case. Yet, if the deal faces further regulatory complications, investors should watch for...

Read the full narrative on Hewlett Packard Enterprise (it's free!)

Hewlett Packard Enterprise's narrative projects $42.7 billion in revenue and $3.9 billion in earnings by 2028. This requires 10.5% annual revenue growth and a $2.5 billion increase in earnings from the current $1.4 billion.

Uncover how Hewlett Packard Enterprise's forecasts yield a $23.60 fair value, a 4% upside to its current price.

Exploring Other Perspectives

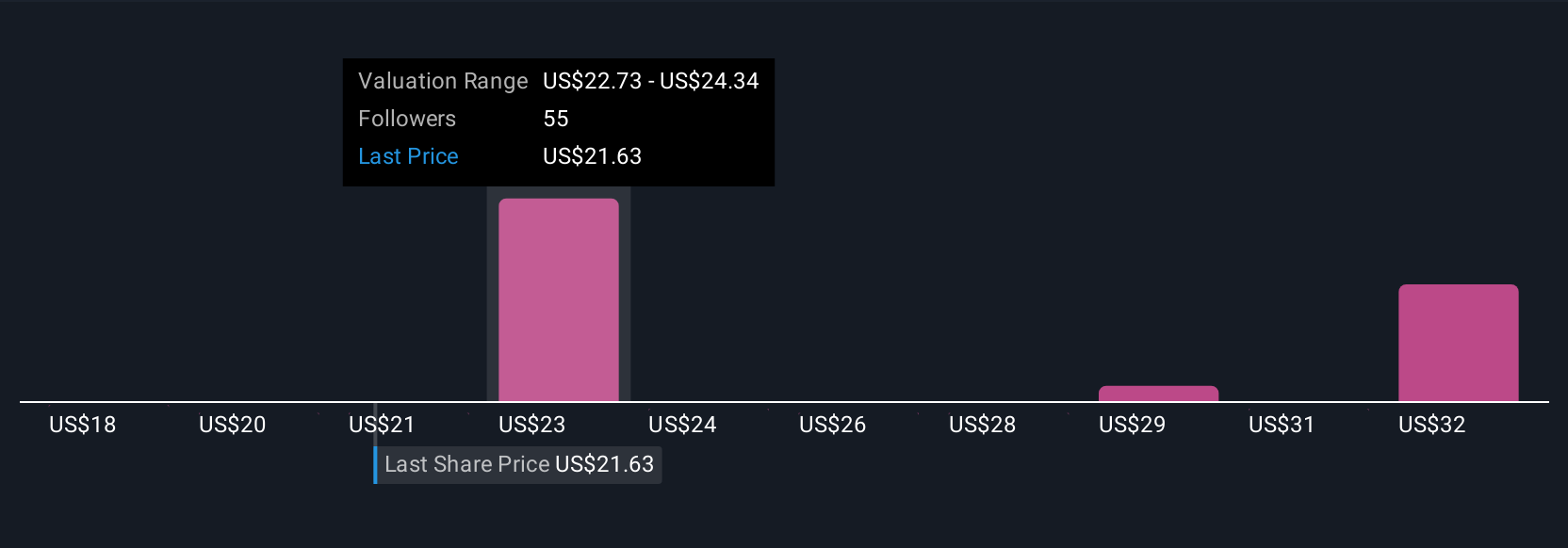

Seven independent fair value estimates from the Simply Wall St Community range from US$17.90 up to US$34.54 per share. While these perspectives differ widely, the potential for US$450 million in annual synergies from the pending Juniper acquisition remains at the heart of the company’s future opportunity and risk profile.

Explore 7 other fair value estimates on Hewlett Packard Enterprise - why the stock might be worth 21% less than the current price!

Build Your Own Hewlett Packard Enterprise Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Hewlett Packard Enterprise research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

- Our free Hewlett Packard Enterprise research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Hewlett Packard Enterprise's overall financial health at a glance.

Curious About Other Options?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Find companies with promising cash flow potential yet trading below their fair value.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if Hewlett Packard Enterprise might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:HPE

Hewlett Packard Enterprise

Provides solutions that allow customers to capture, analyze, and act upon data seamlessly.

Undervalued with moderate growth potential.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Sunrun Stock: When the Energy Transition Collides With the Cost of Capital

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion