Advertisement

- United States

- /

- Tech Hardware

- /

- NasdaqGS:WDC

Does Western Digital’s 17% Weekly Rally Signal More Room to Run in 2025?

Simply Wall St

Reviewed by Bailey Pemberton

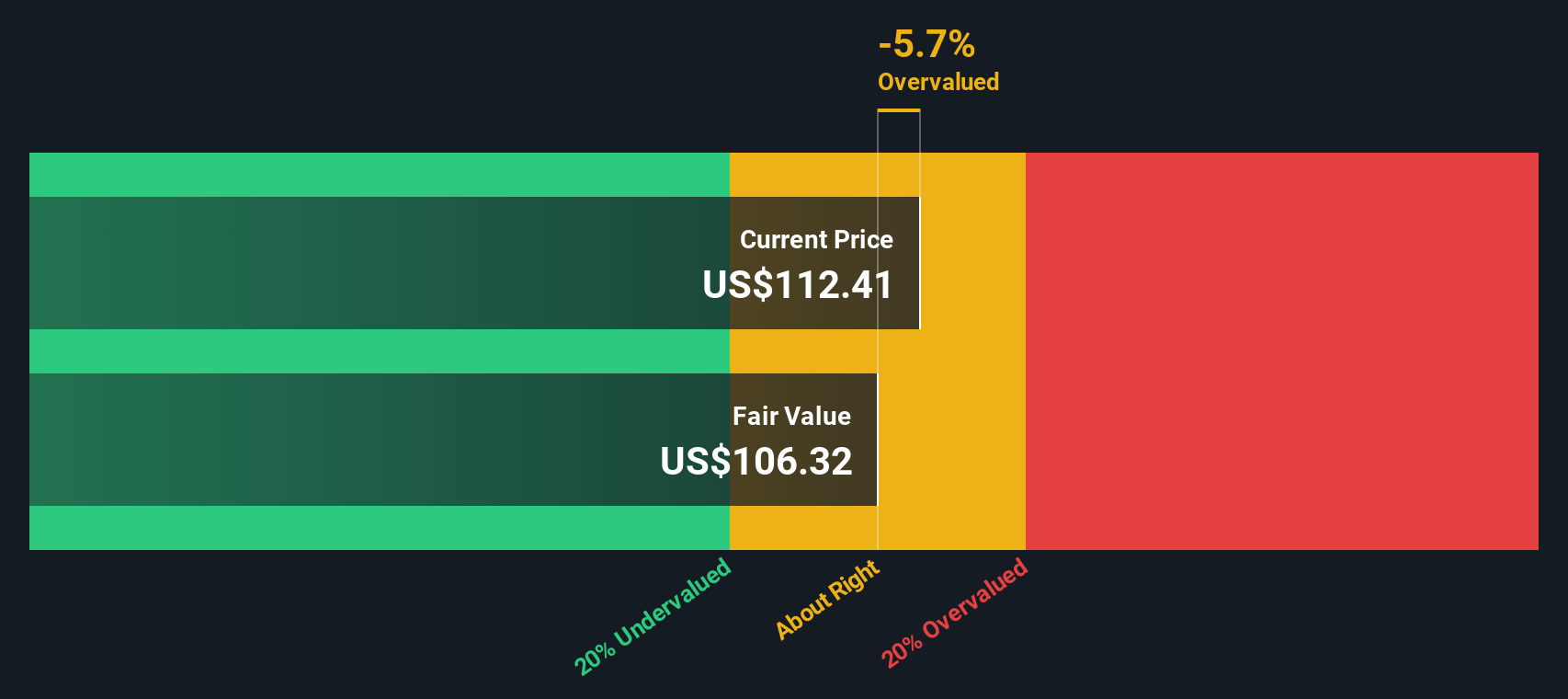

- Curious if Western Digital’s recent rally means its shares are still a good deal, or if the best opportunities have already passed you by? Let’s dig into what is really driving the value here.

- The stock has seen significant gains lately, with a 17.3% jump over the last week and a 197.0% return in the past year, suggesting either surging optimism or shifting risk perceptions.

- Western Digital has attracted attention following rumors about industry consolidation and large-scale investment in data infrastructure, both of which have set the sector buzzing. Market buzz around a potential merger and renewed demand for data storage seem to have supported these dramatic price moves.

- On our scoring system, Western Digital registers a solid 5 out of 6 on the main undervaluation checks, which is impressive. Understanding what goes into that will require a look at several different valuation approaches. Stick around, as we will reveal a deeper way to judge whether the market has this stock valued correctly before we wrap up.

Approach 1: Western Digital Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model is a widely used method for estimating a company's intrinsic value by projecting its future cash flows and discounting them back to their present value. For Western Digital, this approach provides a comprehensive look at how much the business could be worth based on the cash it is expected to generate moving forward.

Western Digital’s current Free Cash Flow (FCF) stands at $1.79 Billion. Analysts forecast steady growth, with FCF projected to reach $4.29 Billion by 2030. The first five years of these projections are based on analyst expectations, while subsequent years are extrapolated by Simply Wall St. This projected increase in FCF reflects optimism around the company’s capacity to generate higher earnings from operations over the next decade.

Applying the 2 Stage Free Cash Flow to Equity model, the intrinsic value of Western Digital is estimated at $230.49 per share. Given recent market pricing, this suggests the stock is approximately 29.1% undervalued according to this method.

In summary, the DCF analysis indicates that Western Digital may offer meaningful value despite recent gains.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Western Digital is undervalued by 29.1%. Track this in your watchlist or portfolio, or discover 921 more undervalued stocks based on cash flows.

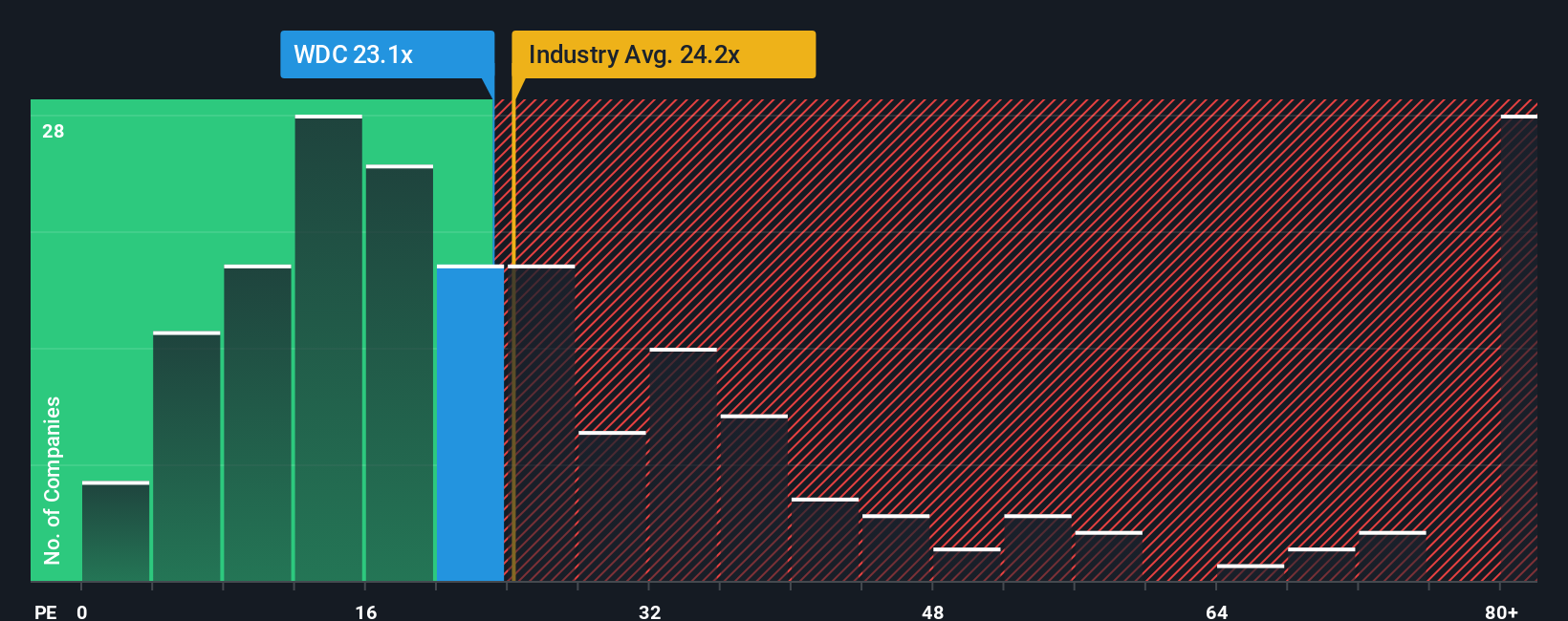

Approach 2: Western Digital Price vs Earnings

The Price-to-Earnings (PE) ratio is a widely used valuation metric when analyzing profitable companies. It compares a company’s share price to its earnings per share. For firms like Western Digital, which currently generates positive earnings, the PE ratio offers a clear gauge of how the market values each dollar of the business’s profit.

The “right” PE ratio varies based on growth expectations and perceived risk. In general, companies with higher expected earnings growth or lower risks tend to command a higher PE, while those facing challenges or uncertainties are usually valued lower.

Western Digital’s current PE ratio stands at 21.5x. This is just below the average PE for its peers at 21.7x and slightly under the technology sector average of 22.4x. At first glance, Western Digital appears to be valued similarly to the broader market and its peer group.

However, Simply Wall St’s proprietary “Fair Ratio” model factors in Western Digital’s specific characteristics such as earnings growth, industry, profit margins, market capitalization, and risk profile, and estimates a fair PE of 39.2x for the stock. This approach offers a more tailored view than generic peer or industry comparisons because it accounts for nuances unique to Western Digital and the factors most likely to affect its value.

Since the current PE of 21.5x is well below the Fair Ratio of 39.2x, Western Digital looks undervalued using this method.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1438 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Western Digital Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives, Simply Wall St’s signature tool that brings the story behind a company to life alongside the numbers.

A Narrative is simply your own investment storyline, combining your beliefs about Western Digital’s future revenue, earnings, and margins with an estimate of what the fair value should be right now. Narratives link what you think the company will achieve, how you forecast its results, and what that means for its valuation. This helps make sense of the data in a way that is personal, straightforward, and actionable.

Accessible right from the Community page on Simply Wall St and used by millions of investors, Narratives make it easy to build or explore different outlooks for Western Digital. They dynamically update as new news or earnings releases arrive, so your investment thesis always reflects the latest reality.

Narratives help you compare fair value (based on your assumptions) to the current share price. For example, you might believe Western Digital could be worth as much as $110 per share if AI demand accelerates and margins expand, while a more cautious Narrative could peg value at just $62 if competition intensifies and risks play out.

Do you think there's more to the story for Western Digital? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Western Digital might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:WDC

Western Digital

Develops, manufactures, and sells data storage devices and solutions based on hard disk drive (HDD) technology in the United States, Asia, Europe, the Middle East, and Africa.

Outstanding track record with flawless balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

139 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

931 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative