- United States

- /

- Tech Hardware

- /

- NasdaqGS:STX

Seagate Technology Holdings plc Just Recorded A 16% EPS Beat: Here's What Analysts Are Forecasting Next

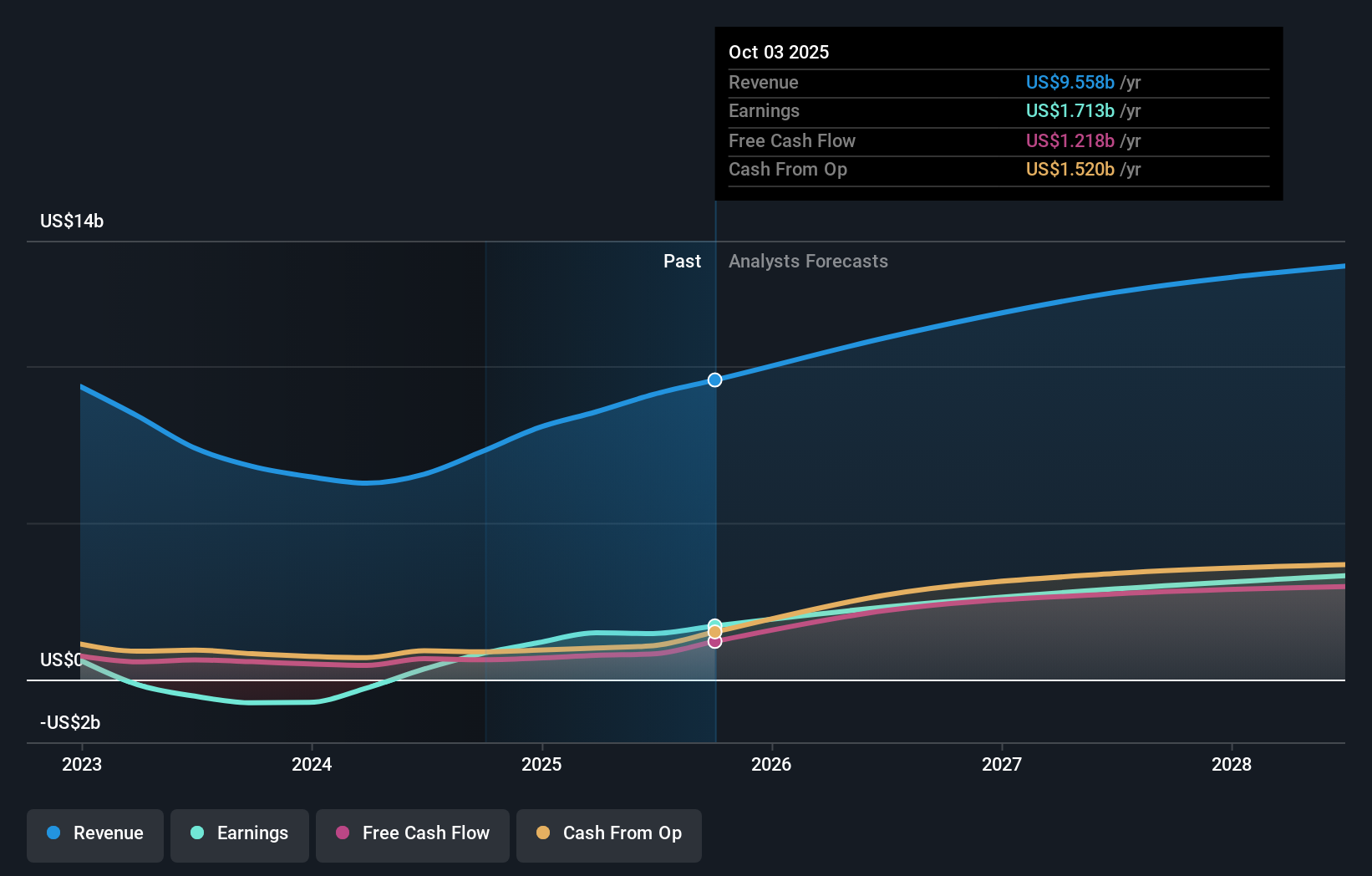

As you might know, Seagate Technology Holdings plc (NASDAQ:STX) just kicked off its latest quarterly results with some very strong numbers. It was overall a positive result, with revenues beating expectations by 3.1% to hit US$2.6b. Seagate Technology Holdings reported statutory earnings per share (EPS) US$2.43, which was a notable 16% above what the analysts had forecast. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. With this in mind, we've gathered the latest statutory forecasts to see what the analysts are expecting for next year.

Following the latest results, Seagate Technology Holdings' 19 analysts are now forecasting revenues of US$10.9b in 2026. This would be a decent 14% improvement in revenue compared to the last 12 months. Per-share earnings are expected to bounce 29% to US$10.33. In the lead-up to this report, the analysts had been modelling revenues of US$10.6b and earnings per share (EPS) of US$9.24 in 2026. There's been a pretty noticeable increase in sentiment, with the analysts upgrading revenues and making a nice gain to earnings per share in particular.

View our latest analysis for Seagate Technology Holdings

It will come as no surprise to learn that the analysts have increased their price target for Seagate Technology Holdings 11% to US$267on the back of these upgrades. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. Currently, the most bullish analyst values Seagate Technology Holdings at US$350 per share, while the most bearish prices it at US$150. This is a fairly broad spread of estimates, suggesting that analysts are forecasting a wide range of possible outcomes for the business.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. One thing stands out from these estimates, which is that Seagate Technology Holdings is forecast to grow faster in the future than it has in the past, with revenues expected to display 19% annualised growth until the end of 2026. If achieved, this would be a much better result than the 8.4% annual decline over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in the industry are forecast to see their revenue grow 6.1% per year. So it looks like Seagate Technology Holdings is expected to grow faster than its competitors, at least for a while.

The Bottom Line

The biggest takeaway for us is the consensus earnings per share upgrade, which suggests a clear improvement in sentiment around Seagate Technology Holdings' earnings potential next year. Happily, they also upgraded their revenue estimates, and are forecasting them to grow faster than the wider industry. There was also a nice increase in the price target, with the analysts clearly feeling that the intrinsic value of the business is improving.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have forecasts for Seagate Technology Holdings going out to 2028, and you can see them free on our platform here.

And what about risks? Every company has them, and we've spotted 3 warning signs for Seagate Technology Holdings (of which 1 makes us a bit uncomfortable!) you should know about.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:STX

Seagate Technology Holdings

Engages in the provision of data storage technology and infrastructure solutions in Singapore, the United States, the Netherlands, and internationally.

Reasonable growth potential with proven track record and pays a dividend.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Automotive Electronics Manufacturer Consistent and Stable

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion