Advertisement

- United States

- /

- Tech Hardware

- /

- NasdaqGS:SMCI

We Don’t Think Super Micro Computer's (NASDAQ:SMCI) Earnings Should Make Shareholders Too Comfortable

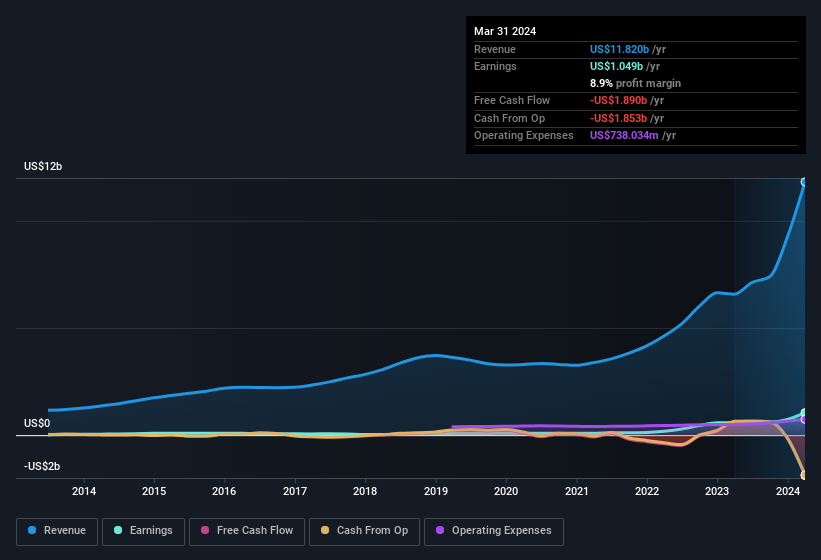

Super Micro Computer, Inc.'s (NASDAQ:SMCI) solid earnings report last week was underwhelming to investors. Our analysis has found some underlying factors which may be cause for concern.

View our latest analysis for Super Micro Computer

Examining Cashflow Against Super Micro Computer's Earnings

Many investors haven't heard of the accrual ratio from cashflow, but it is actually a useful measure of how well a company's profit is backed up by free cash flow (FCF) during a given period. In plain english, this ratio subtracts FCF from net profit, and divides that number by the company's average operating assets over that period. The ratio shows us how much a company's profit exceeds its FCF.

As a result, a negative accrual ratio is a positive for the company, and a positive accrual ratio is a negative. That is not intended to imply we should worry about a positive accrual ratio, but it's worth noting where the accrual ratio is rather high. That's because some academic studies have suggested that high accruals ratios tend to lead to lower profit or less profit growth.

For the year to March 2024, Super Micro Computer had an accrual ratio of 0.91. Statistically speaking, that's a real negative for future earnings. To wit, the company did not generate one whit of free cashflow in that time. Over the last year it actually had negative free cash flow of US$1.9b, in contrast to the aforementioned profit of US$1.05b. It's worth noting that Super Micro Computer generated positive FCF of US$608m a year ago, so at least they've done it in the past. Notably, the company has issued new shares, thus diluting existing shareholders and reducing their share of future earnings. The good news for shareholders is that Super Micro Computer's accrual ratio was much better last year, so this year's poor reading might simply be a case of a short term mismatch between profit and FCF. Shareholders should look for improved cashflow relative to profit in the current year, if that is indeed the case.

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

In order to understand the potential for per share returns, it is essential to consider how much a company is diluting shareholders. In fact, Super Micro Computer increased the number of shares on issue by 12% over the last twelve months by issuing new shares. Therefore, each share now receives a smaller portion of profit. To celebrate net income while ignoring dilution is like rejoicing because you have a single slice of a larger pizza, but ignoring the fact that the pizza is now cut into many more slices. You can see a chart of Super Micro Computer's EPS by clicking here.

How Is Dilution Impacting Super Micro Computer's Earnings Per Share (EPS)?

Super Micro Computer has improved its profit over the last three years, with an annualized gain of 1,051% in that time. In comparison, earnings per share only gained 999% over the same period. And at a glance the 79% gain in profit over the last year impresses. But in comparison, EPS only increased by 74% over the same period. So you can see that the dilution has had a bit of an impact on shareholders.

In the long term, earnings per share growth should beget share price growth. So it will certainly be a positive for shareholders if Super Micro Computer can grow EPS persistently. However, if its profit increases while its earnings per share stay flat (or even fall) then shareholders might not see much benefit. For that reason, you could say that EPS is more important that net income in the long run, assuming the goal is to assess whether a company's share price might grow.

Our Take On Super Micro Computer's Profit Performance

As it turns out, Super Micro Computer couldn't match its profit with cashflow and its dilution means that earnings per share growth is lagging net income growth. Considering all this we'd argue Super Micro Computer's profits probably give an overly generous impression of its sustainable level of profitability. If you'd like to know more about Super Micro Computer as a business, it's important to be aware of any risks it's facing. Be aware that Super Micro Computer is showing 4 warning signs in our investment analysis and 2 of those are concerning...

In this article we've looked at a number of factors that can impair the utility of profit numbers, and we've come away cautious. But there are plenty of other ways to inform your opinion of a company. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:SMCI

Super Micro Computer

Develops and sells server and storage solutions based on modular and open-standard architecture in the United States, Asia, Europe, and internationally.

Undervalued with high growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0768.0% undervalued

278 followersusers have followed this narrative

1 commentusers have commented on this narrative

40 likesusers have liked this narrative

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8591.5% undervalued

77 followersusers have followed this narrative

1 commentusers have commented on this narrative

18 likesusers have liked this narrative

TO

Tokyo on Anheuser-Busch InBev ·

EU#8 - Anheuser-Busch InBev: Courage, Capital, and the Discipline to Build an Empire

Fair Value:€89.4521.3% undervalued

4 followersusers have followed this narrative

3 commentsusers have commented on this narrative

2 likesusers have liked this narrative

OS

oscargarcia on Amazon.com ·

The capitalist colossus that makes your parcels magically appear, powers half the internet, and knows your shopping habits.

Fair Value:US$2802.3% undervalued

59 followersusers have followed this narrative

1 commentusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

CH

Chimichanga696 on Bajaj Auto ·

Bajaj Auto has seen a correction in its stock price after a strong rally, making it an attractive opportunity for investors.

Fair Value:₹15k31.2% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on Barton Gold Holdings ·

Aussie’s Barton Gold, No Debt Miner with 1 Mill That Changes Everything

Fair Value:AU$22.4495.8% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MR

MRT23 on Ategrity Specialty Insurance Company Holdings ·

ASIC is a technology-differentiated E&S insurer compounding book value with a structurally improving combined ratio

Fair Value:US$3035.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.235.6% undervalued

69 followersusers have followed this narrative

2 commentsusers have commented on this narrative

24 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$561.9326.8% undervalued

1396 followersusers have followed this narrative

2 commentsusers have commented on this narrative

12 likesusers have liked this narrative

TR

tripledub on Meta Platforms ·

The $135 Billion Bet That Should Make Every Shareholder Nervous

Fair Value:US$74018.2% undervalued

31 followersusers have followed this narrative

3 commentsusers have commented on this narrative

32 likesusers have liked this narrative