Advertisement

- United States

- /

- Tech Hardware

- /

- NasdaqGS:SMCI

Super Micro Computer (SMCI) Stock Looks Below Fair Value Despite Its 7x Run

Reviewed by Bailey Pemberton

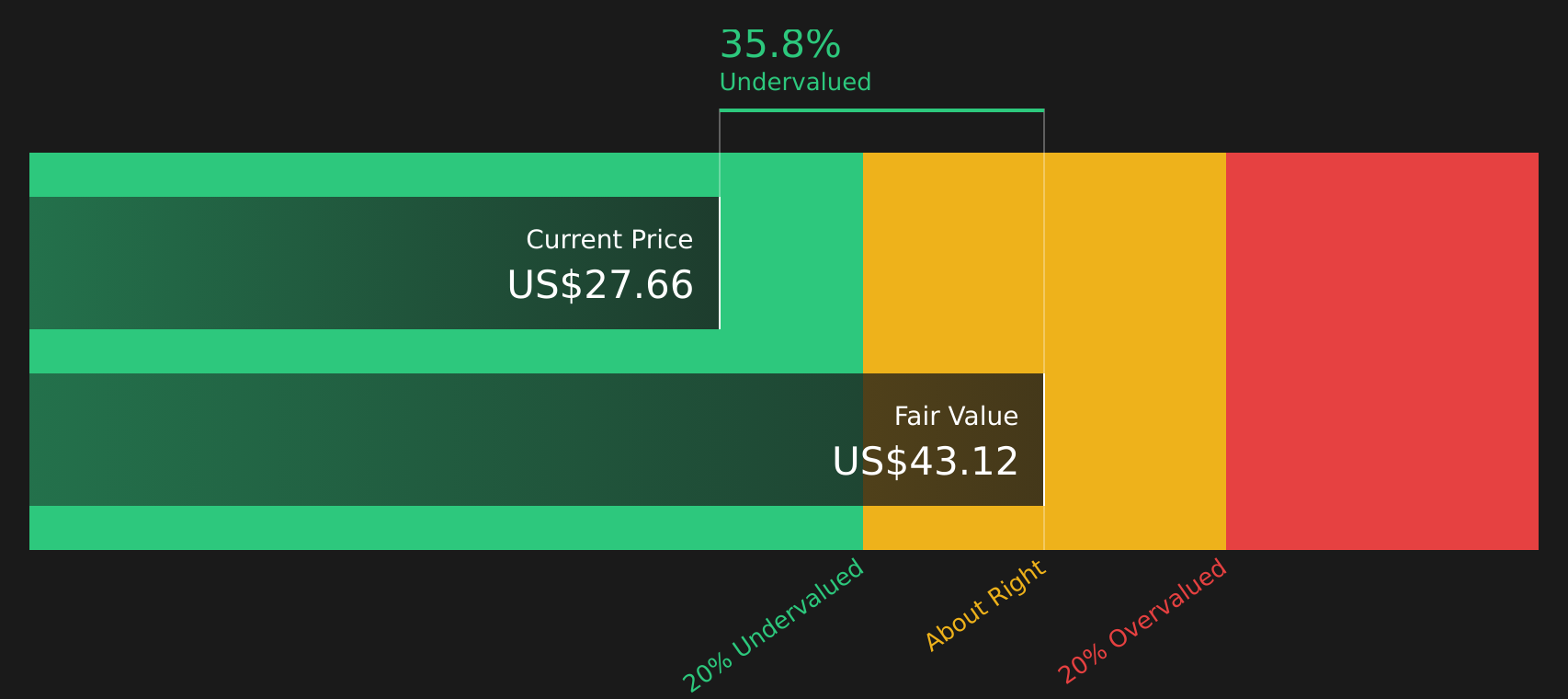

Super Micro Computer stock has given investors a very large 5 year return, yet at around US$27.66 the valuation work still points to a discount, with both the Discounted Cash Flow (DCF) intrinsic value estimate and the market multiples suggesting the shares may be trading below what the fundamentals imply.

- A roughly 7x gain over 5 years leaves long term holders with substantial gains, yet the current valuation signals still flag the stock as pricing in relatively modest expectations compared with that history.

- New edge and high performance AI infrastructure offerings can support expectations for future cash flows, while concerns around margins, competition and sentiment shifts toward other AI infrastructure providers may limit how much of that is reflected in the share price.

- On Simply Wall St's broader checks, Super Micro Computer screens as undervalued in 5 of 6 valuation tests, so the overall picture leans cheap rather than fully pricing in its AI positioning.

The issue now is whether that apparent discount is a genuine margin of safety or simply compensation for the risks that recent news flow and share price declines have brought back into focus.

Find out why Super Micro Computer's -44.4% return over the last year is lagging behind its peers.

Is Super Micro Computer Still Cheap on Cash Flow?

The Discounted Cash Flow (DCF) model here estimates what Super Micro Computer’s potential future cash generation could be worth today. The latest twelve-month free cash flow is a loss of about $6.9b, so the model assumes a recovery followed by growing cash flows rather than simply extrapolating the recent figure. Based on those cash flow projections, the intrinsic value is estimated at roughly $43.12 per share.

Compared with the current share price of about $27.66, this suggests that, on this particular DCF view, Super Micro Computer appears around 35.8% undervalued. The recent launch of turnkey Kubernetes Edge AI appliances with Red Hat and Everpure is one factor used to support constructive cash flow expectations, while the share price still appears to reflect concerns related to margins and competition.

On this DCF assessment, Super Micro Computer stock appears undervalued relative to the cash flows reflected in the model.

Our Discounted Cash Flow (DCF) analysis suggests Super Micro Computer is undervalued by 35.8%. Track this in your watchlist or portfolio, or discover 46 more high quality undervalued stocks.

Does Super Micro Computer Look Undervalued on Earnings?

The P/E multiple is a useful way to think about what you are paying today for each dollar of Super Micro Computer’s earnings. On this measure, Super Micro Computer trades on a P/E of about 14.3x, which is well below the broader Tech sector average of roughly 24.2x and also below the peer group average of around 48.0x.

A fair P/E ratio for Super Micro Computer, based on its sector, scale and risk profile in this model, is estimated at about 52.1x. Compared with the current 14.3x, the stock trades at a large discount to what this framework suggests might be reasonable, even after recent debates around AI hardware margins and competition.

On the P/E multiple, Super Micro Computer stock screens as undervalued relative to both peers and the model’s fair ratio.

See what the numbers say about this price — find out in our valuation breakdown.

The Super Micro Computer Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Super Micro Computer pick up where this valuation puzzle leaves off by spelling out which paths for Super Micro Computer’s growth, margins and earnings would need to occur for the stock to be worth materially more or less than today’s price. Each narrative links its figures to a clear view on how growth, profitability and key risks might evolve, giving you a reference point you can revisit as new information comes through.

Community views on Super Micro Computer sit far apart, with one camp focused on AI infrastructure upside and the other on legal and customer concentration risk.

Bull case: 26% undervalued

"The accelerating global adoption of AI and analytics continues to drive demand for high-performance, scalable server and data center solutions, positioning Super Micro for strong multi-year revenue growth as enterprises and nations build out AI infrastructure, directly supporting projected revenue outperformance…"

Read the full Bull Case to see why Super Micro Computer could be undervalued

Bear case: 13% overvalued

"One customer represented roughly 63% of Q2 FY2026 revenue…"

Read the full Bear Case to see why Super Micro Computer could be overvalued

Do you think there's more to the story for Super Micro Computer? Head over to our Community to see what others are saying!

The Bottom Line

For Super Micro Computer, both the Discounted Cash Flow (DCF) intrinsic value estimate and the earnings multiple work suggest an undervalued stock, even after the recent share price swings. The core question is whether the current discount compensates you for concentration, legal and competitive risks, or whether it reflects an overly cautious read on the company’s AI infrastructure opportunity. From here, everything hinges on whether Super Micro Computer can sustain attractive margins and diversify its revenue base enough for that valuation gap to close rather than widen into a value trap.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:SMCI

Super Micro Computer

Develops and sells server and storage solutions based on modular and open-standard architecture in the United States, Asia, Europe, and internationally.

Undervalued with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Giftify ·

Giftify ($GIFT): A Small-Cap Incentives Platform with More ScaleThan Its Valuation Suggests

Fair Value:US$2.564.5% undervalued

61 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

HA

HarishPK on lululemon athletica ·

Quantifying the Transition: Why Lululemon’s Moat Remains Intact

Fair Value:US$161.825.6% undervalued

24 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$23053.3% overvalued

65 followersusers have followed this narrative

1 commentusers have commented on this narrative

17 likesusers have liked this narrative

JO

John_Eric on Veeva Systems ·

AI-Powered Veeva Systems Poised for Solid Growth Amid Regulatory Stability

Fair Value:US$32038.5% undervalued

33 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

Recently Updated Narratives

BR

browser on Bentley Systems ·

Bentley Systems’ Strategic Positioning in the Digital Infrastructure Cycle

Fair Value:US$15.72102.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6526.7% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AR

ariz_scribe on Marti Technologies ·

$MRT at Roth - Pick of the Panel

Fair Value:US$1.9628.6% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75028.3% undervalued

89 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5450.8% undervalued

61 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$23053.3% overvalued

65 followersusers have followed this narrative

1 commentusers have commented on this narrative

17 likesusers have liked this narrative