Advertisement

- United States

- /

- Tech Hardware

- /

- NasdaqGS:SMCI

Should Super Micro’s AI Expansion And Margin Concerns Require Action From Super Micro Computer (SMCI) Investors?

Reviewed by Sasha Jovanovic

- In late November 2025, Super Micro Computer, Inc. presented its AI-focused server and data centre solutions at the UBS Global Technology and AI Conference in Scottsdale, highlighting its Data Centre Building Block Solutions and partnerships with NVIDIA and AMD.

- At the same time, the company’s push toward a US$36.00 billion fiscal 2026 revenue target, ongoing international capacity expansion, and shifting short interest underscored the tension between ambitious growth plans and market concerns over margins and AI hardware competition.

- We’ll now examine how Super Micro’s aggressive expansion amid sector-wide AI sentiment cooling could influence its existing investment narrative.

Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

Super Micro Computer Investment Narrative Recap

To own Super Micro Computer today, you need to believe its AI focused server platforms and Data Centre Building Block Solutions can translate booming GPU demand into durable, profitable growth despite recent margin pressure. November’s 36.8% share price drop, tied to competition and rising costs, directly affects the key near term catalyst of executing on its US$36.00 billion fiscal 2026 revenue goal, while reinforcing the central risk that AI hardware “price wars” could keep profitability under strain.

The company’s raised fiscal 2026 sales guidance to at least US$36.00 billion is the announcement that most directly intersects with this backdrop, because it increases the execution bar just as sector wide AI enthusiasm has cooled and AI server competition has intensified. How effectively Super Micro ramps its Blackwell era systems and DCBBS offerings with NVIDIA and AMD will likely shape whether the recent pullback looks like a bump in the road or a warning sign for investors focused on...

Read the full narrative on Super Micro Computer (it's free!)

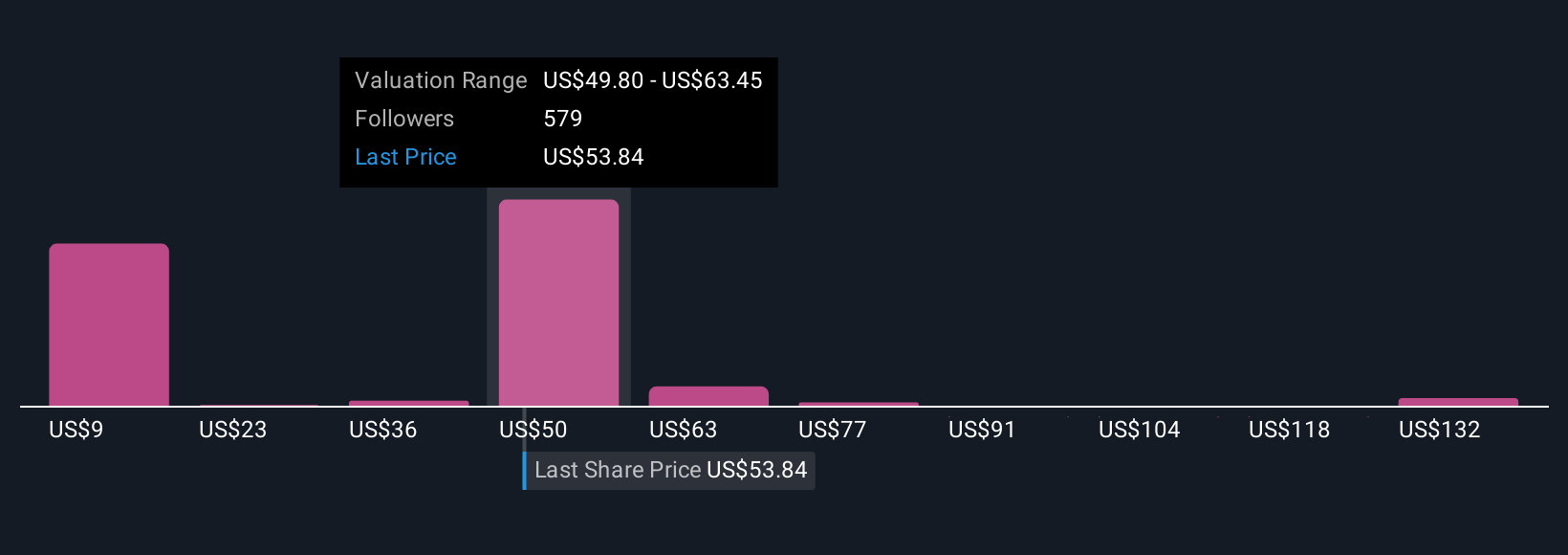

Super Micro Computer's narrative projects $48.2 billion revenue and $2.4 billion earnings by 2028.

Uncover how Super Micro Computer's forecasts yield a $48.53 fair value, a 47% upside to its current price.

Exploring Other Perspectives

Thirty seven members of the Simply Wall St Community currently place Super Micro’s fair value between US$48.53 and US$82.39, highlighting wide dispersion in expectations. Against this range, the recent share price slide and ongoing concerns about AI server margin pressure show why it can be useful to compare several independent views on what might drive the company’s performance next.

Explore 37 other fair value estimates on Super Micro Computer - why the stock might be worth over 2x more than the current price!

Build Your Own Super Micro Computer Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Super Micro Computer research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Super Micro Computer research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Super Micro Computer's overall financial health at a glance.

Ready For A Different Approach?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 24 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:SMCI

Super Micro Computer

Develops and sells server and storage solutions based on modular and open-standard architecture in the United States, Asia, Europe, and internationally.

Undervalued with high growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0777.3% undervalued

156 followersusers have followed this narrative

1 commentusers have commented on this narrative

26 likesusers have liked this narrative

CL

Clive_Thompson on Hermès International Société en commandite par actions ·

Hermès - Expensive bags, and expensive stock. And the story of €14 billion of bearer shares gone missing.

Fair Value:€1.51k10.0% overvalued

16 followersusers have followed this narrative

1 commentusers have commented on this narrative

22 likesusers have liked this narrative

SU

superbullll on Cheniere Energy ·

Cheniere Energy (LNG) — The Toll Road That Geopolitics Just Made More Valuable

Fair Value:US$320.9412.5% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

SA

Salman2415 on GNG Electronics ·

Strong execution in a growing category, but long‑term value hinges on cash‑flow discipline

Fair Value:₹135.87179.9% overvalued

7 followersusers have followed this narrative

1 commentusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

JC

JCAPITAL on Filinvest REIT ·

Filinvest REIT (PSE:FILRT) recorded an average annual revenue decline of about –5.3% over the past 5 years

Fair Value:₱5.8650.9% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JC

JCAPITAL on Shang Properties ·

I bought for undervalue and dividend yield

Fair Value:₱1065.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TR

tripledub on Sprouts Farmers Market ·

The Grocery Store That Shrank Its Way to Prosperity

Fair Value:US$9614.8% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.378.3% undervalued

55 followersusers have followed this narrative

3 commentsusers have commented on this narrative

29 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9826.5% undervalued

47 followersusers have followed this narrative

0 commentsusers have commented on this narrative

35 likesusers have liked this narrative

PD

pdixit1 on Vertiv Holdings Co ·

The Infrastructure AI Cannot Be Built Without

Fair Value:US$408.6437.4% undervalued

38 followersusers have followed this narrative

3 commentsusers have commented on this narrative

18 likesusers have liked this narrative

Trending Discussion

OD

Oddlott on lululemon athletica ·

Thankyou for the interesting comments. So what is the world wide including USA growth rate?

0

|0