Advertisement

- United States

- /

- Electronic Equipment and Components

- /

- NasdaqGS:SCSC

Shareholders May Be More Conservative With ScanSource, Inc.'s (NASDAQ:SCSC) CEO Compensation For Now

Key Insights

- ScanSource's Annual General Meeting to take place on 25th of January

- Salary of US$875.0k is part of CEO Mike Baur's total remuneration

- The overall pay is 56% above the industry average

- ScanSource's total shareholder return over the past three years was 41% while its EPS grew by 75% over the past three years

Performance at ScanSource, Inc. (NASDAQ:SCSC) has been reasonably good and CEO Mike Baur has done a decent job of steering the company in the right direction. In light of this performance, CEO compensation will probably not be the main focus for shareholders as they go into the AGM on 25th of January. However, some shareholders may still be hesitant of being overly generous with CEO compensation.

Check out our latest analysis for ScanSource

How Does Total Compensation For Mike Baur Compare With Other Companies In The Industry?

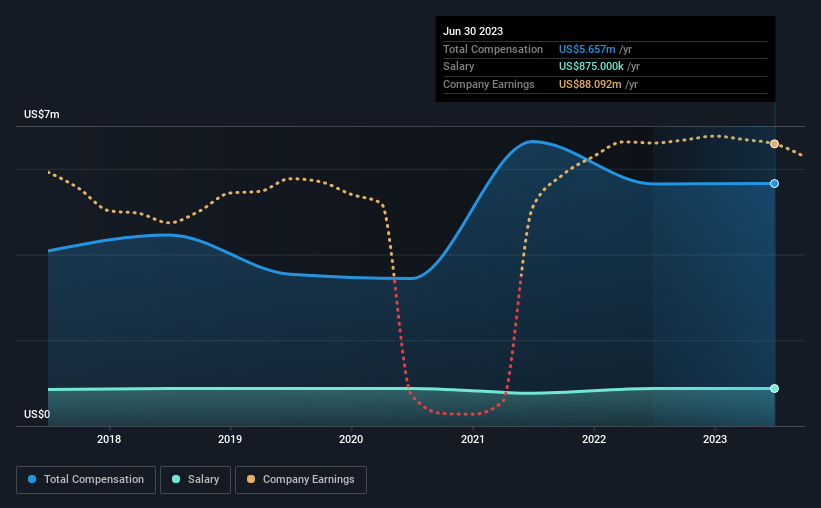

At the time of writing, our data shows that ScanSource, Inc. has a market capitalization of US$947m, and reported total annual CEO compensation of US$5.7m for the year to June 2023. That is, the compensation was roughly the same as last year. While this analysis focuses on total compensation, it's worth acknowledging that the salary portion is lower, valued at US$875k.

For comparison, other companies in the American Electronic industry with market capitalizations ranging between US$400m and US$1.6b had a median total CEO compensation of US$3.6m. Accordingly, our analysis reveals that ScanSource, Inc. pays Mike Baur north of the industry median. What's more, Mike Baur holds US$4.8m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | US$875k | US$875k | 15% |

| Other | US$4.8m | US$4.8m | 85% |

| Total Compensation | US$5.7m | US$5.6m | 100% |

Talking in terms of the industry, salary represented approximately 33% of total compensation out of all the companies we analyzed, while other remuneration made up 67% of the pie. ScanSource pays a modest slice of remuneration through salary, as compared to the broader industry. It's important to note that a slant towards non-salary compensation suggests that total pay is tied to the company's performance.

A Look at ScanSource, Inc.'s Growth Numbers

ScanSource, Inc. has seen its earnings per share (EPS) increase by 75% a year over the past three years. It achieved revenue growth of 2.9% over the last year.

Shareholders would be glad to know that the company has improved itself over the last few years. It's also good to see modest revenue growth, suggesting the underlying business is healthy. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has ScanSource, Inc. Been A Good Investment?

We think that the total shareholder return of 41%, over three years, would leave most ScanSource, Inc. shareholders smiling. So they may not be at all concerned if the CEO were to be paid more than is normal for companies around the same size.

In Summary...

Seeing that the company has put up a decent performance, only a few shareholders, if any at all, might have questions about the CEO pay in the upcoming AGM. Still, not all shareholders might be in favor of a pay raise to the CEO, seeing that they are already being paid higher than the industry.

CEO compensation can have a massive impact on performance, but it's just one element. We did our research and spotted 1 warning sign for ScanSource that investors should look into moving forward.

Switching gears from ScanSource, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:SCSC

ScanSource

Engages in the distribution of technology products and solutions in the United States and internationally.

Flawless balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

JO

Jolt_Communications on Myseum ·

The Future of Social Sharing Is Private and People Are Ready

Fair Value:US$7.9577.1% undervalued

20 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TO

Tokyo on ASML Holding ·

EU#3 - From Philips Management Buyout to Europe’s Biggest Company

Fair Value:€1.31k7.1% undervalued

27 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

YI

yiannisz on Booking Holdings ·

Booking Holdings: Why Ground-Level Travel Trends Still Favor the Platform Giants

Fair Value:US$5.47k8.5% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

CO

composite32 on Shell ·

A fully integrated LNG business seems to be ignored by the market.

Fair Value:UK£36.122.6% undervalued

35 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

CO

composite32 on Otokar Otomotiv ve Savunma Sanayi ·

Otokar is the first choice for tactical armored land vehicles to meet Europe's defense industry needs.

Fair Value:₺668.1135.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BL

BlackGoat on Palantir Technologies ·

Palantir: Redefining Enterprise Software for the AI Era

Fair Value:US$107.0237.0% overvalued

197 followersusers have followed this narrative

6 commentsusers have commented on this narrative

3 likesusers have liked this narrative

AN

andre_santos on Microsoft ·

Microsoft - A Fundamental and Historical Valuation

Fair Value:US$437.171.6% undervalued

18 followersusers have followed this narrative

4 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OO

OOO97 on Neo Performance Materials ·

Undervalued Key Player in Magnets/Rare Earth

Fair Value:CA$25.3324.4% undervalued

71 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$253.0224.5% undervalued

1047 followersusers have followed this narrative

6 commentsusers have commented on this narrative

31 likesusers have liked this narrative

AN

AnalystConsensusTarget on Amazon.com ·

AMZN: Acceleration In Cloud And AI Will Drive Margin Expansion Ahead

Fair Value:US$295.6119.1% undervalued

1343 followersusers have followed this narrative

5 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

JA

jayhcee on Motorcar Parts of America ·

MPAA often has inventory and core-related timing issues. While this quarter’s problems may ease, similar issues have recurred historically and can persist for several quarters. It's not a one-off, it's a structural part of their business. Core returns are simply estimates: How many customers will actually return the original part; how quickly they'll do so; how many are useable; what they're worth, etc. MPAA predicts X sales in a quarter and Y core returns and its reserves, inventory values, etc. are based on that. If they expect a 90% core return rate and only 80% come back it doesn't change cash but they have to write down inventory and increase cost of goods sold which impacts EPS. They've also cited inventory buildup at key customers multiple times in the past. The assumption the latest backlog will all shift into future quarters this year with no impact on pricing, etc. seems more like wishful thinking. Retailer X was slated to buy $10m in parts this quarter but finds they have a lot more inventory on hand than they anticipated so they pushed the order. Realistically there are likely to be SKU cuts, reduction in safety stock on others, etc. Assuming that all $10m will come in this year plus the regular replenishment seems pretty unrealistic. MPAA also has a shaky track record when it comes to new lines and the supposed impact on business. If you look at the EV testing solutions hype back around 2020 that was supposed to diversify them beyond traditional reman and be a higher margin business that would grow with EV adoption. But it has never turned into a material contributor. The debt reduction and stock buy backs are meaningful but IMHO this narrative takes a very optimistic view of things.

0

|0

US

User on Discovery Silver ·

The problem with your reasoning is, that 37 Moz are AgEq. If you read the FS, you'll find out that annual silver production is more around 14-15 Moz. But at the time of the FS, that 37 Moz AgEq was a number that came of a formula (which is specified in the FS), being a mix of four metals: Ag, Au, Pb and Zc. But now, beginning of 2026, the spotprices of silver and gold have risen so much in comparison to Pb and Zc prices, that you need to recalculate the AgEq number of 37 Moz according to the recent prices. This will result in the fact that silver and gold hold more value in that mix of four metals, and thus dragg the 37 Moz AgEQ number down to somewhere around 18 Moz AgEq. The more valuable silver and gold become, the lower the AgEq number will get, but it'll never get under the yearly average production of silver, which should be somewhere between 14-15 Moz Ag in the first four years. So in short, with this in mind, your fair value is rather around CA$ 50, even with silver at 300 usd an ounce. But a more prudent stockprice forecast is around CA$ 20 and hopefully going toward CA$ 30. So DSV is a top stock, because it's producing actual gold every quarter. But don't put your hopes too high.

0

|0