Advertisement

- United States

- /

- Electronic Equipment and Components

- /

- NasdaqGS:RELL

Richardson Electronics' (NASDAQ:RELL) Dividend Will Be $0.06

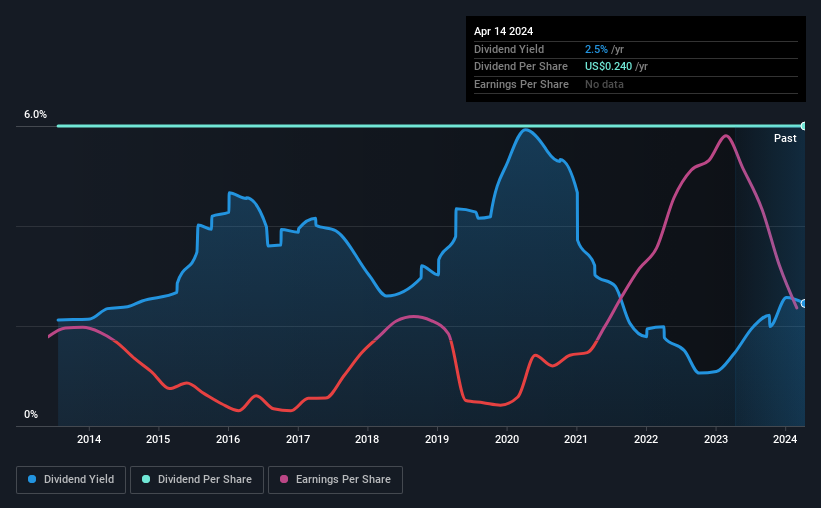

The board of Richardson Electronics, Ltd. (NASDAQ:RELL) has announced that it will pay a dividend on the 29th of May, with investors receiving $0.06 per share. This means the annual payment is 2.5% of the current stock price, which is above the average for the industry.

See our latest analysis for Richardson Electronics

Richardson Electronics' Payment Has Solid Earnings Coverage

A big dividend yield for a few years doesn't mean much if it can't be sustained. Prior to this announcement, Richardson Electronics' dividend was making up a very large proportion of earnings, and the company was also not generating any cash flow to offset this. Generally, we think that this would be a risky long term practice.

Looking forward, earnings per share is forecast to rise by 97.1% over the next year. If the dividend continues along recent trends, we estimate the payout ratio will be 40%, which would make us comfortable with the sustainability of the dividend, despite the levels currently being quite high.

Richardson Electronics Has A Solid Track Record

The company has an extended history of paying stable dividends. There hasn't been much of a change in the dividend over the last 10 years. Dividends have grown relatively slowly, which is not great, but some investors may value the relative consistency of the dividend.

Dividend Growth Could Be Constrained

The company's investors will be pleased to have been receiving dividend income for some time. We are encouraged to see that Richardson Electronics has grown earnings per share at 38% per year over the past five years. Earnings per share is growing nicely, but the company is paying out most of its earnings as dividends. This might be sustainable, but we wonder why Richardson Electronics is not retaining those earnings to reinvest in growth.

In Summary

In summary, while it's good to see that the dividend hasn't been cut, we are a bit cautious about Richardson Electronics' payments, as there could be some issues with sustaining them into the future. We can't deny that the payments have been very stable, but we are a little bit worried about the very high payout ratio. Overall, we don't think this company has the makings of a good income stock.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. For instance, we've picked out 2 warning signs for Richardson Electronics that investors should take into consideration. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:RELL

Richardson Electronics

Provides engineered solutions, power grid and microwave tube, and related consumables in North America, the Asia Pacific, Europe, and Latin America.

Flawless balance sheet with moderate growth potential.

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7065.0% undervalued

43 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9636.2% undervalued

46 followersusers have followed this narrative

8 commentsusers have commented on this narrative

16 likesusers have liked this narrative

NI

niteco on Broadcom ·

A Capital Allocation Favorite with Structural Importance

Fair Value:US$651.0541.3% undervalued

45 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

TO

Tokyo on Okta ·

Good foundation, but now it's all about the next steps

Fair Value:US$15123.0% undervalued

91 followersusers have followed this narrative

7 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on Investigator Silver ·

Investigator Silver, Leverage Exposed: $1/oz Move = $42M Cash for This ASX Developer

Fair Value:AU$2.3997.7% undervalued

13 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

TA

Talos on Voyager Technologies ·

The "Landlord of Orbit" – A Deep Value Play Ahead of the Starlab Era

Fair Value:US$385.289.3% undervalued

17 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Advanced Micro Devices ·

The "David vs. Goliath" AI Trade – Why Second Place is Worth Billions

Fair Value:US$907.3243.6% undervalued

36 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7446.4% undervalued

66 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9723.5% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1931.2% undervalued

51 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative