- United States

- /

- Electronic Equipment and Components

- /

- NasdaqGS:LFUS

Littelfuse (LFUS): Revisiting Valuation After Steady Share Gains and Undervalued Narrative Signals

Reviewed by Simply Wall St

Recent share performance and setup

Littelfuse (LFUS) has quietly outperformed many industrial tech peers this year, with the stock up about 9% year to date and roughly 10% over the past year, despite some recent pullback.

See our latest analysis for Littelfuse.

The recent pullback after a solid 1 month share price return suggests some short term profit taking, but the 1 year total shareholder return still points to steady, if unspectacular, momentum.

If you are comparing Littelfuse to what else is working in the market, this could be a good moment to explore high growth tech and AI stocks for other tech names with similar tailwinds.

With steady fundamentals, mid single digit sales growth, and the shares still trading at a discount to analyst targets, the key question now is whether Littelfuse is an undervalued compounder or if the market is already pricing in its next leg of growth.

Most Popular Narrative Narrative: 17.1% Undervalued

With Littelfuse closing at $255 versus a most popular narrative fair value of $307.50, the valuation gap sets the stage for some ambitious growth assumptions.

The rapid buildout of renewable energy infrastructure, grid storage, and sustainable grid ecosystems is resulting in double digit sales growth and a robust opportunity pipeline for Littelfuse, positioning the company to benefit from continued secular tailwinds and expanding its addressable market, which should positively impact both revenues and margins.

Curious what kind of revenue runway, margin lift, and future earnings multiple are baked into that price gap? The narrative spells out a surprisingly aggressive profitability path, calibrated to long term electrification demand, that you might want to stress test for yourself.

Result: Fair Value of $307.50 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, lingering execution risks in power semiconductors, along with heavy exposure to cyclical auto and industrial demand, could quickly challenge that upbeat profitability trajectory.

Find out about the key risks to this Littelfuse narrative.

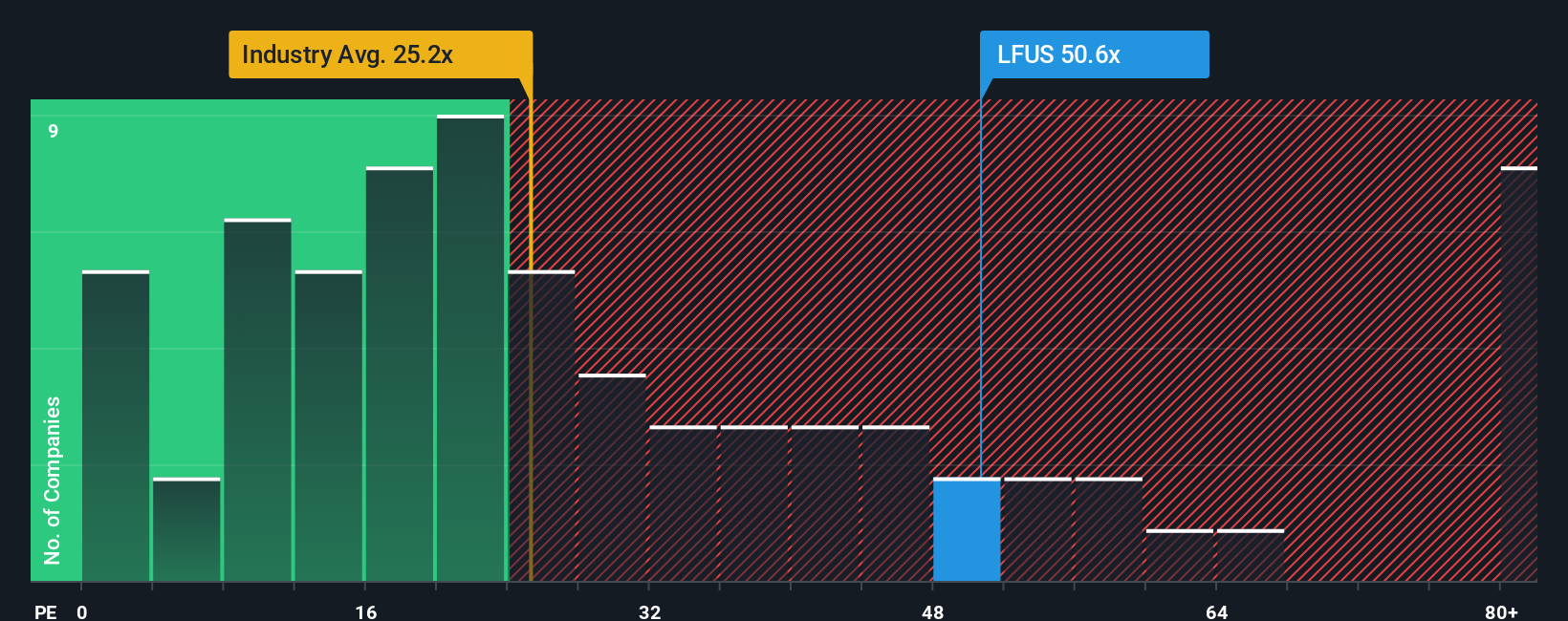

Another angle on valuation

While the narrative and fair value work point to Littelfuse as undervalued, its current price to earnings ratio of 53.5 times looks stretched versus the US Electronic industry at 24.5 times, peers at 39.4 times, and a fair ratio of 29 times. This raises the risk of multiple compression if growth disappoints.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Littelfuse Narrative

If this perspective does not quite fit your view, or you prefer a hands on approach, you can build a full narrative in minutes: Do it your way

A great starting point for your Littelfuse research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Before you move on, you may be able to gain an edge by using Simply Wall Street's powerful screener to identify fresh opportunities that match your strategy and risk profile.

- Explore potential multi baggers by focusing on these 3625 penny stocks with strong financials that combine very small market capitalizations with relatively strong fundamentals.

- Seek exposure to the AI theme by filtering for these 25 AI penny stocks where intelligent automation and data driven models are central to the business.

- Support your income objectives by focusing on these 13 dividend stocks with yields > 3% that may offer cash distributions alongside solid business quality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:LFUS

Littelfuse

Designs, manufactures, and sells electronic components, modules, and subassemblies.

Flawless balance sheet average dividend payer.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Clarivate Stock: When Data Becomes the Backbone of Innovation and Law

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

MicroVision will explode future revenue by 380.37% with a vision towards success

Trending Discussion