Advertisement

- United States

- /

- Electronic Equipment and Components

- /

- NasdaqGS:IPGP

Analysts Have Lowered Expectations For IPG Photonics Corporation (NASDAQ:IPGP) After Its Latest Results

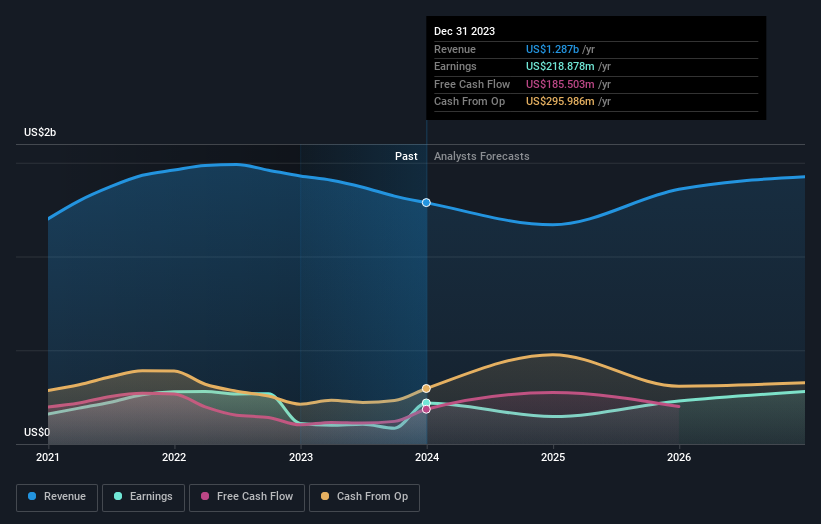

There's been a notable change in appetite for IPG Photonics Corporation (NASDAQ:IPGP) shares in the week since its annual report, with the stock down 12% to US$88.99. Results were roughly in line with estimates, with revenues of US$1.3b and statutory earnings per share of US$4.63. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. With this in mind, we've gathered the latest statutory forecasts to see what the analysts are expecting for next year.

See our latest analysis for IPG Photonics

Following the recent earnings report, the consensus from ten analysts covering IPG Photonics is for revenues of US$1.17b in 2024. This implies an uncomfortable 9.2% decline in revenue compared to the last 12 months. Statutory earnings per share are forecast to plunge 33% to US$3.17 in the same period. Yet prior to the latest earnings, the analysts had been anticipated revenues of US$1.34b and earnings per share (EPS) of US$4.98 in 2024. Indeed, we can see that the analysts are a lot more bearish about IPG Photonics' prospects following the latest results, administering a substantial drop in revenue estimates and slashing their EPS estimates to boot.

The consensus price target fell 11% to US$111, with the weaker earnings outlook clearly leading valuation estimates. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. There are some variant perceptions on IPG Photonics, with the most bullish analyst valuing it at US$131 and the most bearish at US$74.00 per share. Analysts definitely have varying views on the business, but the spread of estimates is not wide enough in our view to suggest that extreme outcomes could await IPG Photonics shareholders.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the IPG Photonics' past performance and to peers in the same industry. These estimates imply that revenue is expected to slow, with a forecast annualised decline of 9.2% by the end of 2024. This indicates a significant reduction from annual growth of 1.0% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 5.2% per year. It's pretty clear that IPG Photonics' revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The most important thing to take away is that the analysts downgraded their earnings per share estimates, showing that there has been a clear decline in sentiment following these results. Unfortunately, they also downgraded their revenue estimates, and our data indicates underperformance compared to the wider industry. Even so, earnings per share are more important to the intrinsic value of the business. Furthermore, the analysts also cut their price targets, suggesting that the latest news has led to greater pessimism about the intrinsic value of the business.

With that in mind, we wouldn't be too quick to come to a conclusion on IPG Photonics. Long-term earnings power is much more important than next year's profits. At Simply Wall St, we have a full range of analyst estimates for IPG Photonics going out to 2026, and you can see them free on our platform here..

You can also see our analysis of IPG Photonics' Board and CEO remuneration and experience, and whether company insiders have been buying stock.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:IPGP

IPG Photonics

Develops, manufactures, and sells fiber lasers, fiber amplifiers, diode lasers, and laser-based systems used in materials processing, medical, and advanced applications.

Flawless balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Conexeu Sciences ·

This small biotech is developing technology that could potentially change how tissue is rebuilt

Fair Value:US$25.3450.6% undervalued

17 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

HE

HedgeY on Quanta Services ·

The Picks-and-Shovels Leader of the Grid Supercycle

Fair Value:US$7101.3% overvalued

33 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

FU

FundamentalFlow on Karman Holdings ·

KRMN — Karman Space & Defense: Down 58% from Peak, Is the Market Mispricing a Hypergrowth Defense Compounder?

Fair Value:US$105.651.0% undervalued

17 followersusers have followed this narrative

1 commentusers have commented on this narrative

10 likesusers have liked this narrative

DO

Double_Bubbler on Invinity Energy Systems ·

Invinity Energy Systems: All About That BESS

Fair Value:UK£162.0% undervalued

24 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

Recently Updated Narratives

PU

Pure_Research on Micron Technology ·

Strategic and Financial Blueprint of Micron Technology: Resolving the Memory Wall in the Gen-AI Era

Fair Value:US$2.02k49.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

Connor_Y on Palantir Technologies ·

Palantir: Operating System for Government and Regulated Industry AI

Fair Value:US$361.5863.1% undervalued

10 followersusers have followed this narrative

2 commentsusers have commented on this narrative

0 likesusers have liked this narrative

LE

lenny67 on Renforth Resources ·

The Strategic Arbitrage at Parbec: Why Renforth Holds the Cards

Fair Value:CA$0.1586.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7444.1% undervalued

66 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9635.2% undervalued

56 followersusers have followed this narrative

8 commentsusers have commented on this narrative

17 likesusers have liked this narrative

CO

Connor_Y on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1928.3% undervalued

51 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

Trending Discussion

AC

ACV on Alignment Healthcare ·

high medical loss ratios, and negative free cash flow signal that scaling profitably remains elusive...

0

|0