Advertisement

- United States

- /

- Electronic Equipment and Components

- /

- NasdaqGS:HOLI

What Is Hollysys Automation Technologies Ltd.'s (NASDAQ:HOLI) Share Price Doing?

Hollysys Automation Technologies Ltd. (NASDAQ:HOLI), which is in the electronic business, and is based in China, received a lot of attention from a substantial price increase on the NASDAQGS over the last few months. With many analysts covering the stock, we may expect any price-sensitive announcements have already been factored into the stock’s share price. However, what if the stock is still a bargain? Let’s examine Hollysys Automation Technologies’s valuation and outlook in more detail to determine if there’s still a bargain opportunity.

Check out our latest analysis for Hollysys Automation Technologies

What's the opportunity in Hollysys Automation Technologies?

Good news, investors! Hollysys Automation Technologies is still a bargain right now. I’ve used the price-to-earnings ratio in this instance because there’s not enough visibility to forecast its cash flows. The stock’s ratio of 8.08x is currently well-below the industry average of 20.79x, meaning that it is trading at a cheaper price relative to its peers. However, given that Hollysys Automation Technologies’s share is fairly volatile (i.e. its price movements are magnified relative to the rest of the market) this could mean the price can sink lower, giving us another chance to buy in the future. This is based on its high beta, which is a good indicator for share price volatility.

What kind of growth will Hollysys Automation Technologies generate?

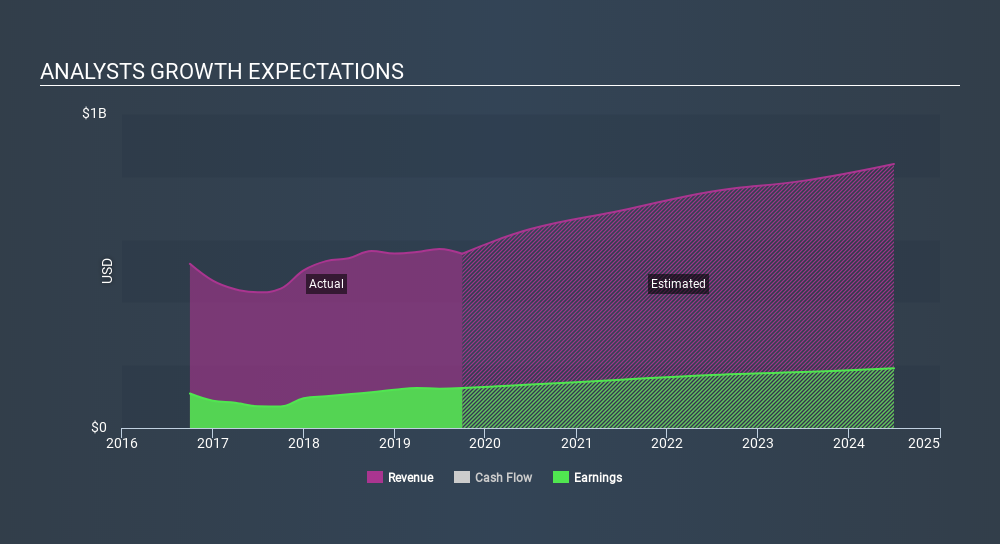

Investors looking for growth in their portfolio may want to consider the prospects of a company before buying its shares. Although value investors would argue that it’s the intrinsic value relative to the price that matter the most, a more compelling investment thesis would be high growth potential at a cheap price. With profit expected to grow by 35% over the next couple of years, the future seems bright for Hollysys Automation Technologies. It looks like higher cash flow is on the cards for the stock, which should feed into a higher share valuation.

What this means for you:

Are you a shareholder? Since HOLI is currently undervalued, it may be a great time to accumulate more of your holdings in the stock. With an optimistic outlook on the horizon, it seems like this growth has not yet been fully factored into the share price. However, there are also other factors such as capital structure to consider, which could explain the current undervaluation.

Are you a potential investor? If you’ve been keeping an eye on HOLI for a while, now might be the time to make a leap. Its prosperous future outlook isn’t fully reflected in the current share price yet, which means it’s not too late to buy HOLI. But before you make any investment decisions, consider other factors such as the track record of its management team, in order to make a well-informed investment decision.

Price is just the tip of the iceberg. Dig deeper into what truly matters – the fundamentals – before you make a decision on Hollysys Automation Technologies. You can find everything you need to know about Hollysys Automation Technologies in the latest infographic research report. If you are no longer interested in Hollysys Automation Technologies, you can use our free platform to see my list of over 50 other stocks with a high growth potential.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NasdaqGS:HOLI

Hollysys Automation Technologies

Provides automation control system solutions in the People’s Republic of China, Southeast Asia, India, and the Middle East.

Excellent balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|8.8% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.3% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$384.84|18.1% undervalued

BL

Community Contributor