Advertisement

- United States

- /

- Electronic Equipment and Components

- /

- NasdaqGS:FLEX

A Note On Flex Ltd.'s (NASDAQ:FLEX) ROE and Debt To Equity

Many investors are still learning about the various metrics that can be useful when analysing a stock. This article is for those who would like to learn about Return On Equity (ROE). By way of learning-by-doing, we'll look at ROE to gain a better understanding of Flex Ltd. (NASDAQ:FLEX).

Return on equity or ROE is a key measure used to assess how efficiently a company's management is utilizing the company's capital. Put another way, it reveals the company's success at turning shareholder investments into profits.

Check out our latest analysis for Flex

How Is ROE Calculated?

ROE can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Flex is:

12% = US$422m ÷ US$3.4b (Based on the trailing twelve months to December 2020).

The 'return' refers to a company's earnings over the last year. So, this means that for every $1 of its shareholder's investments, the company generates a profit of $0.12.

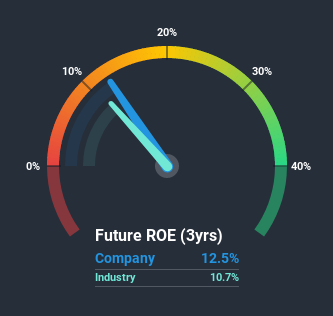

Does Flex Have A Good ROE?

By comparing a company's ROE with its industry average, we can get a quick measure of how good it is. However, this method is only useful as a rough check, because companies do differ quite a bit within the same industry classification. You can see in the graphic below that Flex has an ROE that is fairly close to the average for the Electronic industry (11%).

That's neither particularly good, nor bad. While at least the ROE is not lower than the industry, its still worth checking what role the company's debt plays as high debt levels relative to equity may also make the ROE appear high. If true, then it is more an indication of risk than the potential. Our risks dashboardshould have the 3 risks we have identified for Flex.

The Importance Of Debt To Return On Equity

Most companies need money -- from somewhere -- to grow their profits. That cash can come from retained earnings, issuing new shares (equity), or debt. In the case of the first and second options, the ROE will reflect this use of cash, for growth. In the latter case, the debt used for growth will improve returns, but won't affect the total equity. In this manner the use of debt will boost ROE, even though the core economics of the business stay the same.

Combining Flex's Debt And Its 12% Return On Equity

Flex does use a high amount of debt to increase returns. It has a debt to equity ratio of 1.13. While its ROE is pretty respectable, the amount of debt the company is carrying currently is not ideal. Investors should think carefully about how a company might perform if it was unable to borrow so easily, because credit markets do change over time.

Summary

Return on equity is useful for comparing the quality of different businesses. Companies that can achieve high returns on equity without too much debt are generally of good quality. All else being equal, a higher ROE is better.

Having said that, while ROE is a useful indicator of business quality, you'll have to look at a whole range of factors to determine the right price to buy a stock. The rate at which profits are likely to grow, relative to the expectations of profit growth reflected in the current price, must be considered, too. So you might want to check this FREE visualization of analyst forecasts for the company.

But note: Flex may not be the best stock to buy. So take a peek at this free list of interesting companies with high ROE and low debt.

When trading Flex or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NasdaqGS:FLEX

Flex

Provides technology innovation, supply chain, and manufacturing solutions to data center, communications, enterprise, consumer, automotive, industrial, healthcare, industrial, and power industries.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Ubisoft Entertainment ·

Is Ubisoft the Market’s Biggest Pricing Error? Why Forensic Value Points to €33 Per Share

Fair Value:€33.888.1% undervalued

47 followersusers have followed this narrative

3 commentsusers have commented on this narrative

21 likesusers have liked this narrative

TO

Tokyo on LVMH Moët Hennessy - Louis Vuitton Société Européenne ·

EU#4 - Turning Heritage into the World’s Strongest Luxury Empire

Fair Value:€750.0428.5% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

WE

WealthAP on Alphabet ·

The "Easy Money" Is Gone: Why Alphabet Is Now a "Show Me" Story

Fair Value:US$386.4316.5% undervalued

63 followersusers have followed this narrative

1 commentusers have commented on this narrative

19 likesusers have liked this narrative

Recently Updated Narratives

SE

SelectiveCapital on FactSet Research Systems ·

Future PE of 12.8x Shines Bright for FactSet Growth

Fair Value:US$313.9934.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on Brookfield Infrastructure ·

BIPC: A strategic player in the energy crisis, a hybrid of Utility and Digital REIT.

Fair Value:US$57.1412.5% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AL

alex30free on Indutrade ·

Quintessential serial acquirer

Fair Value:SEK 256.868.9% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OO

OOO97 on Neo Performance Materials ·

Undervalued Key Player in Magnets/Rare Earth

Fair Value:CA$25.3322.3% undervalued

75 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

DA

davidlsander on Ubisoft Entertainment ·

Is Ubisoft the Market’s Biggest Pricing Error? Why Forensic Value Points to €33 Per Share

Fair Value:€33.888.1% undervalued

47 followersusers have followed this narrative

3 commentsusers have commented on this narrative

21 likesusers have liked this narrative

WE

WealthAP on PayPal Holdings ·

The "Sleeping Giant" Stumbles, Then Wakes Up

Fair Value:US$8250.7% undervalued

88 followersusers have followed this narrative

6 commentsusers have commented on this narrative

35 likesusers have liked this narrative

Trending Discussion

KA

Kalibrator on Ubisoft Entertainment ·

As a gamer, I would not touch this company now. They are hated by the community and have been releasing major flops on their AAA games during the last 5 years (for good reasons). It is true that the valuation is ridiculously low compared to what the licenses are worth, but if the trend continues the value of those will also decline. Management needs to almost make a 180° turnaround to get things right. I agree that a take-private deal before it is too late might be the best option for an investor entering today. We might also see a split sales of the different studios. It is a very risky play, but potentially with high reward.

1

|0

CG

CGHHDEEU2026 on LANXESS ·

It is very interesting to overlook the how strongly the fair values assessed by various analysists divergent (based on HANDELSBLATT today): Barclays 14€, GoldmanIt Sachs 10€, UBS 14€, Jeffries 17€, Berenberg 18€, Warburg € 21, Deutsche Bank 27€. So, Anglo-Saxon analysts are much less optimistic than their continental European colleagues. Yesterday the Lanxess share price jumped by 11 percent. Hopefully it won't be a one-off event...

0

|0