- United States

- /

- Communications

- /

- NasdaqGS:CSCO

How Investors May Respond To Cisco Systems (CSCO) AI Enhancements for Webex and Global Ecosystem Expansion

Reviewed by Sasha Jovanovic

- In late September 2025, Cisco announced new AI-powered enhancements to its Webex Customer Experience portfolio, including unified quality management tools for supervisors, expanded AI agent capabilities, and deeper integrations with Salesforce, Amazon Web Services, and Epic Systems, alongside planned Webex ecosystem expansions in India and Saudi Arabia.

- By enabling supervisors to manage both AI and human agents through a single platform and broadening language support, Cisco is aiming to transform customer interactions and streamline service operations for global clients.

- We'll examine how Cisco's rollout of unified AI-powered tools for Webex supervisors could shape its long-term investment narrative and market position.

These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

Cisco Systems Investment Narrative Recap

For investors considering Cisco Systems, the core thesis revolves around its ability to lead in AI-driven networking and security while shifting toward higher-margin, recurring software revenues. The recent Webex enhancements position Cisco to strengthen its AI and collaboration offerings, but do not materially change the most critical short-term catalyst: accelerating AI infrastructure demand from hyperscale and cloud customers. The principal risk remains Cisco’s dependency on large, cyclical infrastructure orders from a concentrated customer base.

Among recent announcements, the launch of AI-powered enhancements in the Webex Customer Experience portfolio stands out as particularly relevant. These innovations unify supervision of human and AI agents across the contact center, directly aligning with Cisco’s push for continued recurring revenue growth and expansion in enterprise AI applications.

However, investors should also consider that, in contrast, the concentration of cloud and AI infrastructure orders could ...

Read the full narrative on Cisco Systems (it's free!)

Cisco Systems' outlook forecasts $65.2 billion in revenue and $14.0 billion in earnings by 2028. This is based on an assumed 4.8% annual revenue growth rate and a $3.8 billion increase in earnings from the current $10.2 billion.

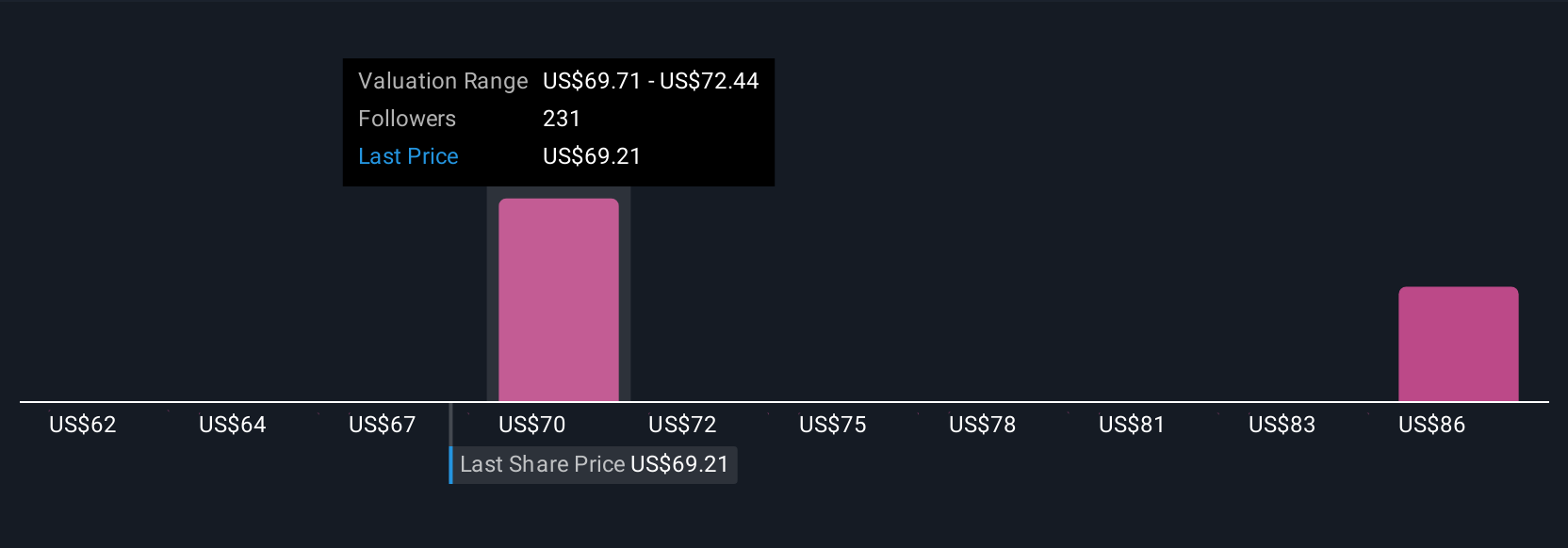

Uncover how Cisco Systems' forecasts yield a $75.81 fair value, a 11% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members' fair value estimates for Cisco Systems span from US$58.24 to US$75.81, with 11 distinct perspectives. Despite this spread, Cisco’s reliance on a handful of hyperscale clients for AI infrastructure orders could weigh heavily on future results, so it's worth seeing what others think.

Explore 11 other fair value estimates on Cisco Systems - why the stock might be worth 15% less than the current price!

Build Your Own Cisco Systems Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Cisco Systems research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Cisco Systems research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Cisco Systems' overall financial health at a glance.

No Opportunity In Cisco Systems?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Find companies with promising cash flow potential yet trading below their fair value.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:CSCO

Cisco Systems

Designs, develops, and sells technologies that help to power, secure, and draw insights from the internet in the Americas, Europe, the Middle East, Africa, the Asia Pacific, Japan, and China.

Established dividend payer and good value.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion