Advertisement

- United States

- /

- Software

- /

- NYSE:U

Unity Software (U) Valuation: Is Growth Already Priced In After Recent 14% Share Price Rise?

Unity Software (U.S.) shares have quietly drifted higher over the past month, up nearly 14% as investors sift through developments in the interactive software space. The rise comes in response to healthy revenue growth and improved net income figures over the past year.

See our latest analysis for Unity Software.

The latest 1-month share price return of nearly 14% builds on a strong year for Unity Software, with a 76% total shareholder return over the past twelve months. This signals renewed optimism in its growth outlook. Momentum has picked up recently as investors respond to healthier fundamentals and ongoing excitement about interactive software platforms.

If today’s momentum in Unity caught your attention, now’s a great opportunity to explore See the full list for free.

But with shares hovering just shy of analyst targets and recent gains fueled by stronger fundamentals, the big question remains: Is Unity Software trading at a discount, or has the market already factored in its future growth?

Most Popular Narrative: 12.1% Overvalued

Unity Software last closed at $43.14, which is above the fair value of $38.48 according to the most widely followed narrative by andreas_eliades. This creates a debate over whether the market is overestimating the company's immediate prospects while overlooking potentially significant catalysts on the horizon.

Unity's increasingly diversified revenue streams in non-gaming sectors decrease its riskiness and bolster its long-term growth potential. Significant restructuring progress with the new management addressing past missteps is evident by the rollback of the controversial runtime fee.

Why do some believe Unity’s turnaround could reshape its future and justify a premium price? The key assumptions driving this fair value calculation involve dramatic changes behind the scenes and future revenue bets beyond gaming. But which strategic pivots and financial forecasts carry the most weight in this narrative? Only a deep dive unveils what really powers this valuation.

Result: Fair Value of $38.48 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, concerns about intensifying competition in advertising and uncertainty around sustained non-gaming growth could challenge the optimism behind Unity’s bullish narrative.

Find out about the key risks to this Unity Software narrative.

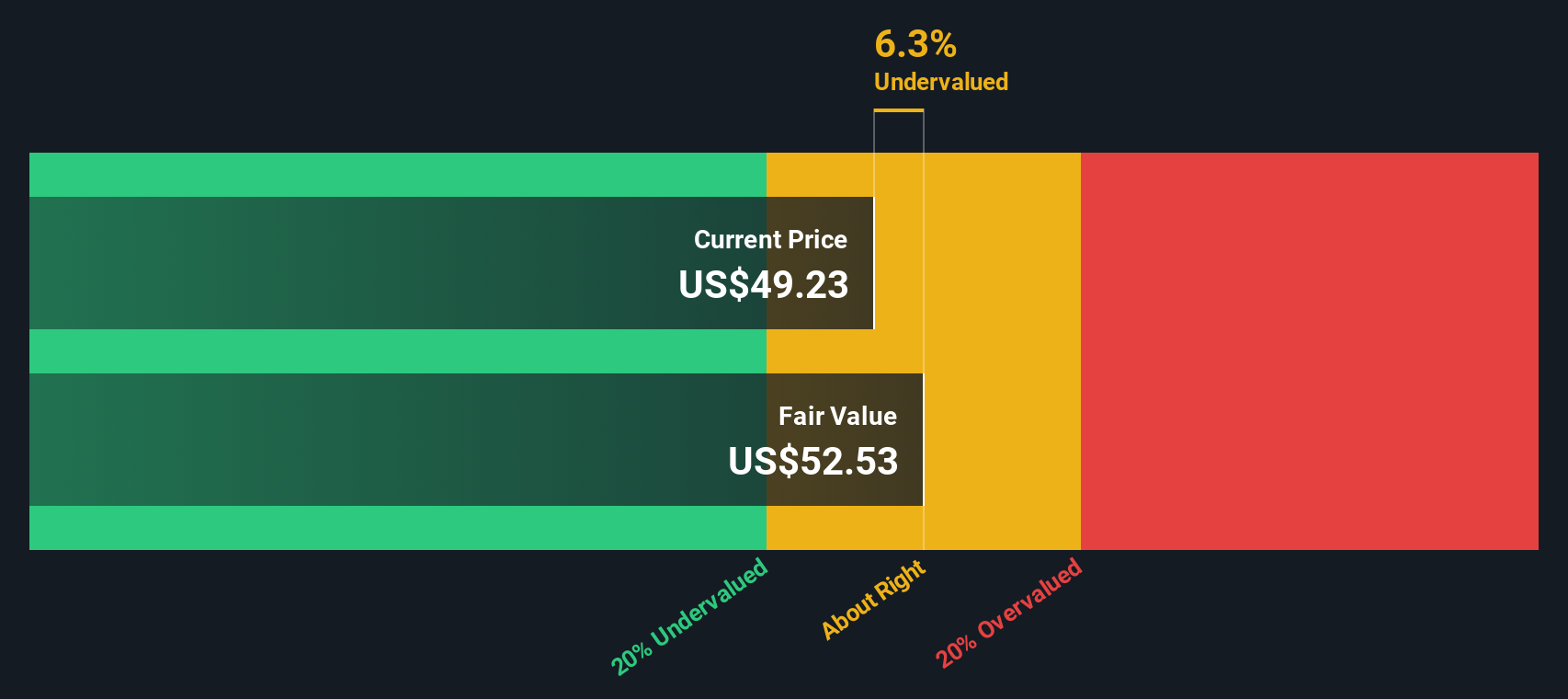

Another View: SWS DCF Model Suggests Undervaluation

While the most popular narrative sees Unity as overvalued, our SWS DCF model presents a different picture. According to this approach, Unity’s shares are trading below fair value, with the DCF estimate coming in at $55.91 compared to the current price of $43.14. This method views Unity as undervalued by a significant margin. This raises the question: which valuation is closer to reality, and what does this divergence mean for investors?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Unity Software for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 928 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Unity Software Narrative

If you have a different perspective or want to dive into the numbers yourself, it takes just a few minutes to shape your own narrative. Do it your way

A great starting point for your Unity Software research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Smart Investment Opportunities?

Why stop here when there are powerful stocks making headlines every day? Get a step ahead of the crowd and target trends before they hit the mainstream. Let Simply Wall Street’s screener help you zero in on companies set to disrupt their industries and reward forward-thinking investors.

- Capture long-term returns by locking in these 14 dividend stocks with yields > 3% that reward shareholders with yields over 3%, building reliable income into your portfolio.

- Ride the wave of innovation by backing these 25 AI penny stocks transforming business with artificial intelligence breakthroughs and real-world applications.

- Anticipate the next market surge by targeting these 928 undervalued stocks based on cash flows that the crowd has not recognized yet for their strong cash flow potential.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:U

Unity Software

Operates a platform to develop, deploy, and grow games and interactive experiences for mobile phones, PCs, consoles, and extended reality devices in the United States, China, Hong Kong, Taiwan, Europe, the Middle East, Africa, the Asia Pacific, Canada, and Latin America.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7065.0% undervalued

40 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9636.2% undervalued

45 followersusers have followed this narrative

8 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Broadcom ·

A Capital Allocation Favorite with Structural Importance

Fair Value:US$651.0541.3% undervalued

42 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

TO

Tokyo on Okta ·

Good foundation, but now it's all about the next steps

Fair Value:US$15123.0% undervalued

90 followersusers have followed this narrative

7 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Recently Updated Narratives

DC

Dc12 on Doximity ·

High physician usership and impressive AI tools

Fair Value:US$33.740.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Rog on CTT - Correios De Portugal ·

Why CTT benefits right now in multiple ways

Fair Value:€6.6710.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

ES

Esteban on Hershey ·

Hershey - fortress brand-and-scale position in U.S. confectionery: protects the downside far better than it compounds the upside

Fair Value:US$85.86111.6% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7446.4% undervalued

65 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9723.5% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1931.2% undervalued

49 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative