Advertisement

- United States

- /

- Software

- /

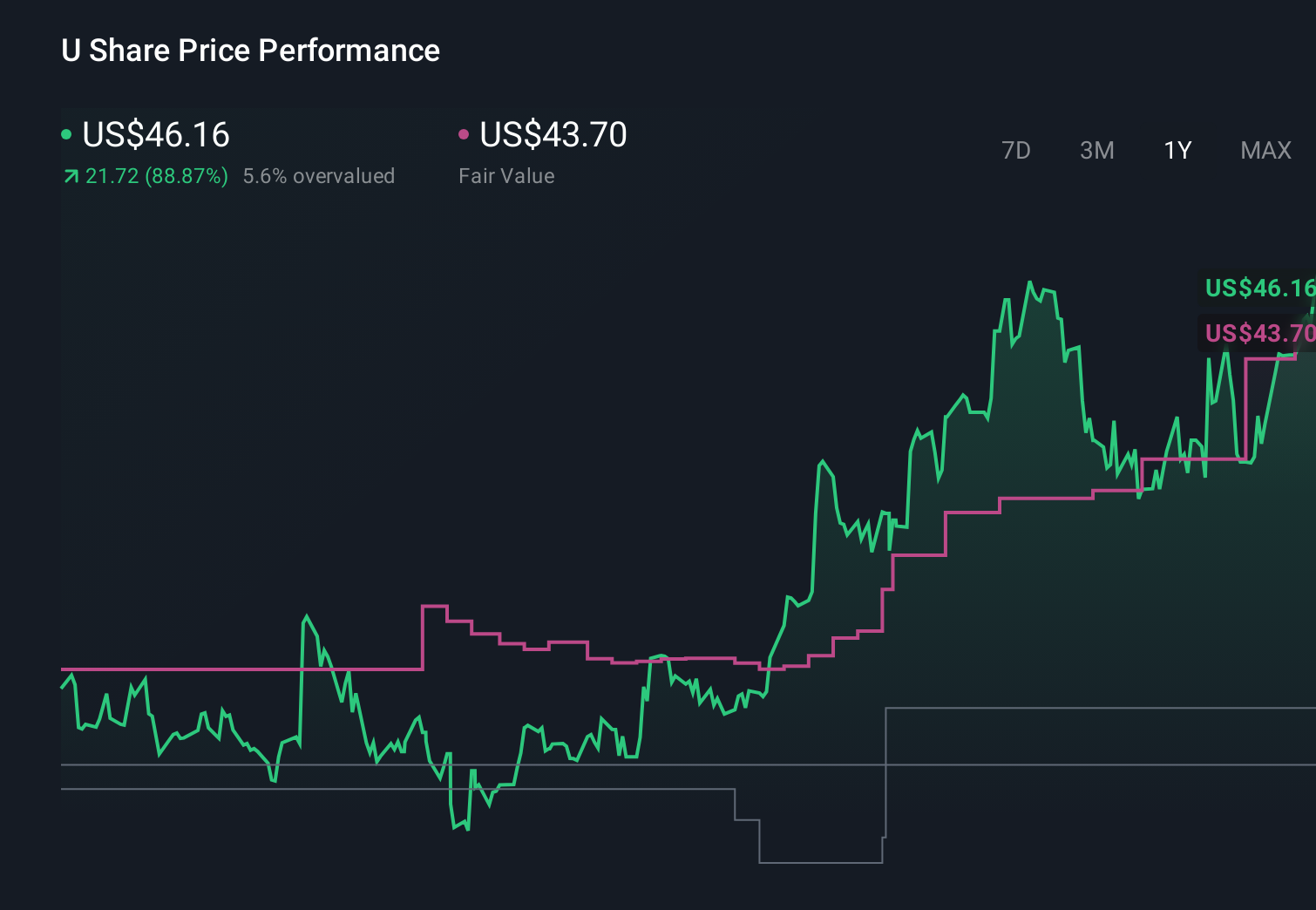

- NYSE:U

Unity Results Highlight Vector Growth AI Push And Leadership Reset

Reviewed by Bailey Pemberton

- Unity Software (NYSE:U) reported strong quarterly results, supported by its Vector advertising platform.

- Vector has now recorded three consecutive quarters of mid teen sequential revenue growth.

- Bernard Kim has been appointed to a key leadership role, while several founders and a long serving director have left the board.

- Unity is pushing ahead with AI integration and platform upgrades, alongside efforts to streamline operations.

Unity sits at the intersection of real time 3D content, gaming and advertising, so the performance of its Vector ad business matters for how you think about its broader ecosystem. The consistent mid teen sequential revenue growth in Vector over three quarters gives investors a concrete data point on how the monetization side of the story is developing.

At the same time, the leadership shake up and focus on AI tools signal that Unity Software (NYSE:U) is in a period of change that goes beyond a single quarter. For investors, the key questions now center on how governance shifts, AI efforts and operational simplification might influence Unity’s product mix and revenue drivers in the future.

Stay updated on the most important news stories for Unity Software by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Unity Software.

For Unity, the latest quarter is as much a leadership and direction story as it is a numbers update. Revenue of US$503.09 million for Q4 and a smaller net loss of US$89.96 million show a business that is still loss making but working to tighten up its model while leaning on Vector as a key growth engine. The new Q1 2026 revenue outlook of US$480 million to US$490 million sets expectations for a cooler start to the year, which helps frame how much of the recent Vector strength might be offset by softer trends elsewhere.

How This Fits Into The Unity Software Narrative

- The stronger quarter for Vector and renewed growth in Create align with the idea that AI powered tools and broader adoption of Unity’s engine can support revenue growth and gradually improve earnings stability.

- Ongoing losses of US$402.77 million for the full year and continued investment in AI tools and new markets highlight the execution and cost risks that the narrative already raises, especially as Unity pushes into non gaming verticals where adoption is less certain.

- The shake up in the board, including the arrival of Bernard Kim and founder departures, along with the planned retirement of the Chief Accounting Officer, adds a governance and execution angle that is not fully captured in the earlier focus on product rollouts and partnerships.

Knowing what a company is worth starts with understanding its story. Check out one of the top narratives in the Simply Wall St Community for Unity Software to help decide what it is worth to you.

The Risks and Rewards Investors Should Consider

- ⚠️ Unity reported a full year 2025 net loss of US$402.77 million and continues to post quarterly losses, so the path to sustained profitability is still uncertain.

- ⚠️ Leadership turnover at both board and accounting levels introduces transition risk, particularly as Unity competes with larger players like Epic Games and Roblox with their own engines and ecosystems.

- 🎁 Vector has delivered three straight quarters of mid teen sequential revenue growth, which indicates that Unity’s AI powered ad tools are gaining traction with advertisers.

- 🎁 Create posted its fastest year over year growth in more than two years, including strong momentum in China, which supports the idea of a more diversified revenue base beyond a single region or segment.

What To Watch Going Forward

From here, investors may want to see whether Unity can keep Vector’s momentum while lifting overall margins, especially as the legacy IronSource ad network becomes less material. The company’s guidance for flat revenue in Grow Solutions and double digit growth in Create provides a reference point that investors can compare against future quarters. Leadership changes, including Bernard Kim joining the board and the search for a new Chief Accounting Officer, will influence how Unity sets priorities in AI powered tools, data usage, and cost discipline in comparison with competitors like Epic Games and Roblox. How consistently Unity delivers against its Q1 2026 guidance range of US$480 million to US$490 million will likely shape confidence in the broader multi year story.

To stay up to date on how the latest news affects the investment narrative for Unity Software, head to the community page for Unity Software to follow the top community narratives.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:U

Unity Software

Operates a platform to develop, deploy, and grow games and interactive experiences for mobile phones, PCs, consoles, and extended reality devices in the United States, China, Hong Kong, Taiwan, Europe, the Middle East, Africa, the Asia Pacific, Canada, and Latin America.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0774.4% undervalued

218 followersusers have followed this narrative

1 commentusers have commented on this narrative

31 likesusers have liked this narrative

SI

SimpleMan887 on GameStop ·

GameStop will ace the financial crisis wave with its strategic Bitcoin investment and cash reserves

Fair Value:US$22089.4% undervalued

55 followersusers have followed this narrative

2 commentsusers have commented on this narrative

21 likesusers have liked this narrative

YI

yiannisz on Hesai Group ·

The First Real Lidar Winner

Fair Value:US$27.0716.3% undervalued

14 followersusers have followed this narrative

1 commentusers have commented on this narrative

4 likesusers have liked this narrative

TR

tripledub on Taiwan Semiconductor Manufacturing ·

The Most Wonderful Monopoly in the Most Dangerous Neighbourhood on Earth

Fair Value:US$3812.7% undervalued

12 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative

Recently Updated Narratives

TA

Talos on 5E Advanced Materials ·

5E Advanced Materials (FEAM): A Binary Critical Minerals Play with a $6.65 Fair Value Target

Fair Value:US$6.6577.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

53

537578 on Recursion Pharmaceuticals ·

Recursion Pharmaceuticals! WTH is going on?

Fair Value:US$1.9766.5% overvalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Visa ·

Visa and the Case for Patience in Premium Businesses

Fair Value:US$2808.7% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3956.1% undervalued

45 followersusers have followed this narrative

3 commentsusers have commented on this narrative

42 likesusers have liked this narrative

RO

Robbo on Tesla ·

The academically fascinating Tesla

Fair Value:US$301.1k% overvalued

37 followersusers have followed this narrative

11 commentsusers have commented on this narrative

31 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$587.3136.9% undervalued

1351 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

EL

Element1 on Greatland Resources ·

I can’t believe how inaccurate and out of date this site is—and people rely on it. Greatland owns tw...

0

|0

MI

Mikeymike on Auxly Cannabis Group ·

Id like to understand why they believe the profit margin is going decline so dramatically. Is it ene...

0

|0