- United States

- /

- Software

- /

- NYSE:TYL

We Discuss Why The CEO Of Tyler Technologies, Inc. (NYSE:TYL) Is Due For A Pay Rise

Key Insights

- Tyler Technologies' Annual General Meeting to take place on 6th of May

- Total pay for CEO H. Moore includes US$675.0k salary

- The overall pay is 47% below the industry average

- Over the past three years, Tyler Technologies' EPS grew by 19% and over the past three years, the total shareholder return was 38%

The solid performance at Tyler Technologies, Inc. (NYSE:TYL) has been impressive and shareholders will probably be pleased to know that CEO H. Moore has delivered. At the upcoming AGM on 6th of May, they would be interested to hear about the company strategy going forward and get a chance to cast their votes on resolutions such as executive remuneration and other company matters. Here we will show why we think CEO compensation is appropriate and discuss the case for a pay rise.

View our latest analysis for Tyler Technologies

Comparing Tyler Technologies, Inc.'s CEO Compensation With The Industry

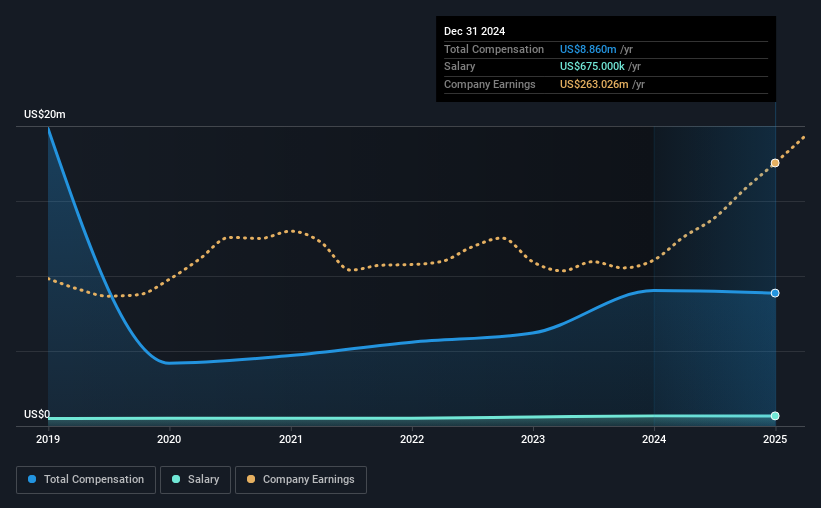

At the time of writing, our data shows that Tyler Technologies, Inc. has a market capitalization of US$22b, and reported total annual CEO compensation of US$8.9m for the year to December 2024. That is, the compensation was roughly the same as last year. While this analysis focuses on total compensation, it's worth acknowledging that the salary portion is lower, valued at US$675k.

On comparing similar companies in the American Software industry with market capitalizations above US$8.0b, we found that the median total CEO compensation was US$17m. In other words, Tyler Technologies pays its CEO lower than the industry median. What's more, H. Moore holds US$44m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | US$675k | US$675k | 8% |

| Other | US$8.2m | US$8.4m | 92% |

| Total Compensation | US$8.9m | US$9.0m | 100% |

On an industry level, roughly 11% of total compensation represents salary and 89% is other remuneration. In Tyler Technologies' case, non-salary compensation represents a greater slice of total remuneration, in comparison to the broader industry. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

Tyler Technologies, Inc.'s Growth

Over the past three years, Tyler Technologies, Inc. has seen its earnings per share (EPS) grow by 19% per year. In the last year, its revenue is up 10.0%.

This demonstrates that the company has been improving recently and is good news for the shareholders. It's also good to see modest revenue growth, suggesting the underlying business is healthy. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has Tyler Technologies, Inc. Been A Good Investment?

Boasting a total shareholder return of 38% over three years, Tyler Technologies, Inc. has done well by shareholders. As a result, some may believe the CEO should be paid more than is normal for companies of similar size.

In Summary...

Given the company's decent performance, the CEO remuneration policy might not be shareholders' central point of focus in the AGM. However, investors will get the chance to engage on key strategic initiatives and future growth opportunities for the company and set their longer-term expectations.

While CEO pay is an important factor to be aware of, there are other areas that investors should be mindful of as well. We did our research and spotted 1 warning sign for Tyler Technologies that investors should look into moving forward.

Switching gears from Tyler Technologies, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Tyler Technologies might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:TYL

Tyler Technologies

Provides integrated software and technology management solutions for the public sector.

Solid track record with excellent balance sheet.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion