Advertisement

- United States

- /

- Diversified Financial

- /

- NYSE:XYZ

Square, Inc.'s (NYSE:SQ) P/E is Sky High But Doesn't Mean The Stock Is Overvalued

Yesterday fintech giant Square, Inc. ( NYSE:SQ ) announced that it is adding banking and checking accounts to the range of services it offers small businesses. These services will further expand the very large portfolio of services Square is able to offer businesses. This makes the platform more valuable to potential customers and creates opportunities to earn more revenue from each of its business customers. It also underscores the fact that Square is still very much in growth mode which goes some way to explaining the incredibly high PE ratio of 308x. But is such a high PE realistic given the growth outlook for Square?

The average PE ratio of US equities is around 18x, which means Square is trading on a PE ratio 17 times higher. Even the IT industry in which Square operates only has a PE of 34.9x.

View our latest analysis for Square

Want the full picture on analyst estimates for the company? Then our free report on Square will help you uncover what's on the horizon.

Clearly the market is very optimistic about Square's outlook, so it's worth taking a closer look at historical and forecast growth.

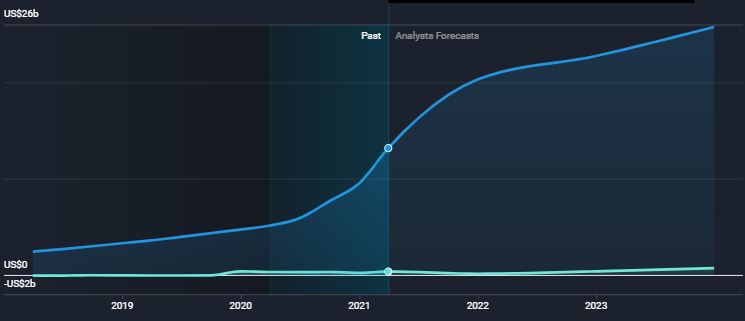

How Is Square's Growth Trending?

Square's P/E ratio would be typical for a company that's expected to deliver very strong growth, and importantly, perform much better than the market.

Retrospectively, the last year delivered a decent 11% gain to the company's bottom line.Still, EPS has barely risen at all in aggregate from three years ago, which is not ideal.Accordingly, shareholders probably wouldn't have been overly satisfied with the unstable medium-term growth rates.

Shifting to the future, estimates from the analysts covering the company suggest earnings should grow by 25% each year over the next three years. This is a lot better than the 14% per year forecast for the broader market, but probably not enough to justify such a high multiple.

If we take a look at analyst forecasts for revenue and earnings, we can see that while revenue is growing rapidly, the company is barely profitable. In fact, earnings are expected to remain flat while revenue continues to rise. This is typical of companies that prioritize growth over profitability.

The Bottom Line on Square's P/E

When a company prioritizes growth to the extent that Square does, the PE ratio merely indicates that investors are optimistic. It doesn't mean the stock is wildly overvalued compared to the rest of the market. But it does mean investors should look for other ways to assess the risk of investing in Square.

Ultimately, investors will want to see the company generate profits. Square can increase its profits by improving its profit margin or growing revenue. Eventually revenue growth will begin to slow and by then investors will want to see the profit margin improve. It would be concerning if revenue growth slowed without a corresponding improvement in profit margins.

Square is still burning cash to fund growth, although the burn rate appears manageable. This is funded both by borrowing and by selling new stock. Over the last five years the number of shares has increased by 31%, which means shareholders have been diluted. However, the rate at which new shares are being issued has fallen each year, which is good news. If share issues were to pick up, that may also indicate that the company is struggling to stay on a path to profitability.

In addition, Square is showing a few other warning signs that you may want to be aware of.

Square continues to launch new services, allowing it to grow its market share and the revenue it earns from each customer. The PE ratio is very high, but this needs to be viewed in the context of its goal of growing market share and revenue rather than prioritizing profitability.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with a strong growth track record, trading on a P/E below 20x.

Valuation is complex, but we're here to simplify it.

Discover if Block might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Richard Bowman and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Richard Bowman

Richard is an analyst, writer and investor based in Cape Town, South Africa. He has written for several online investment publications and continues to do so. Richard is fascinated by economics, financial markets and behavioral finance. He is also passionate about tools and content that make investing accessible to everyone.

About NYSE:XYZ

Block

Block, Inc., together with its subsidiaries, builds ecosystems focused on commerce and financial products and services in the United States and internationally.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6928.0% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8149.5% undervalued

7 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

AU

AuCA on Nova Ljubljanska Banka d.d ·

Nova Ljubljanska Banka d.d will expect a 11.2% revenue boost driving future growth

Fair Value:€20916.5% undervalued

23 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3404.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

87 followersusers have followed this narrative

11 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7923.6% undervalued

925 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative