Advertisement

- United States

- /

- IT

- /

- NYSE:SNOW

Does Snowflake’s Expanded AI Agent “Control Plane” Strategy Reshape The Bull Case For SNOW?

Reviewed by Sasha Jovanovic

- In April 2026, Snowflake announced extensive updates to Snowflake Intelligence and Cortex Code, aiming to connect more enterprise data sources, systems, and AI models into a single environment so organizations can run AI agents directly on governed data reflecting how their businesses operate.

- By positioning these AI agents as a control plane for enterprise workflows and extending Cortex Code across third-party platforms like AWS Glue, Databricks, and Postgres, Snowflake is trying to embed itself more deeply into how both technical and business users build, automate, and share data-driven work.

- Next, we will examine how Snowflake’s push to make Intelligence a control plane for agentic workflows affects its investment narrative.

We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Snowflake Investment Narrative Recap

To own Snowflake, you need to believe it can evolve from a cloud data warehouse into a core AI and data control layer for large enterprises. The near term catalyst is whether AI driven workloads can translate into sustained product revenue growth and improved cash flow, while the biggest risk remains intense competition and high costs in a still unprofitable business. The latest Snowflake Intelligence and Cortex Code updates do not materially change those near term stakes.

The April 2026 Snowflake Intelligence and Cortex Code upgrades are most relevant here because they go directly at the AI native platform concern. By letting AI agents act on governed data across tools like AWS Glue, Databricks and Postgres, Snowflake is trying to stay central as customers experiment with more AI centric stacks, which could be important for how quickly AI usage turns into durable consumption on its platform.

But beneath that promise, investors should also be aware that rising R&D spend, compliance demands and competition could still pressure Snowflake’s profitability and valuation...

Read the full narrative on Snowflake (it's free!)

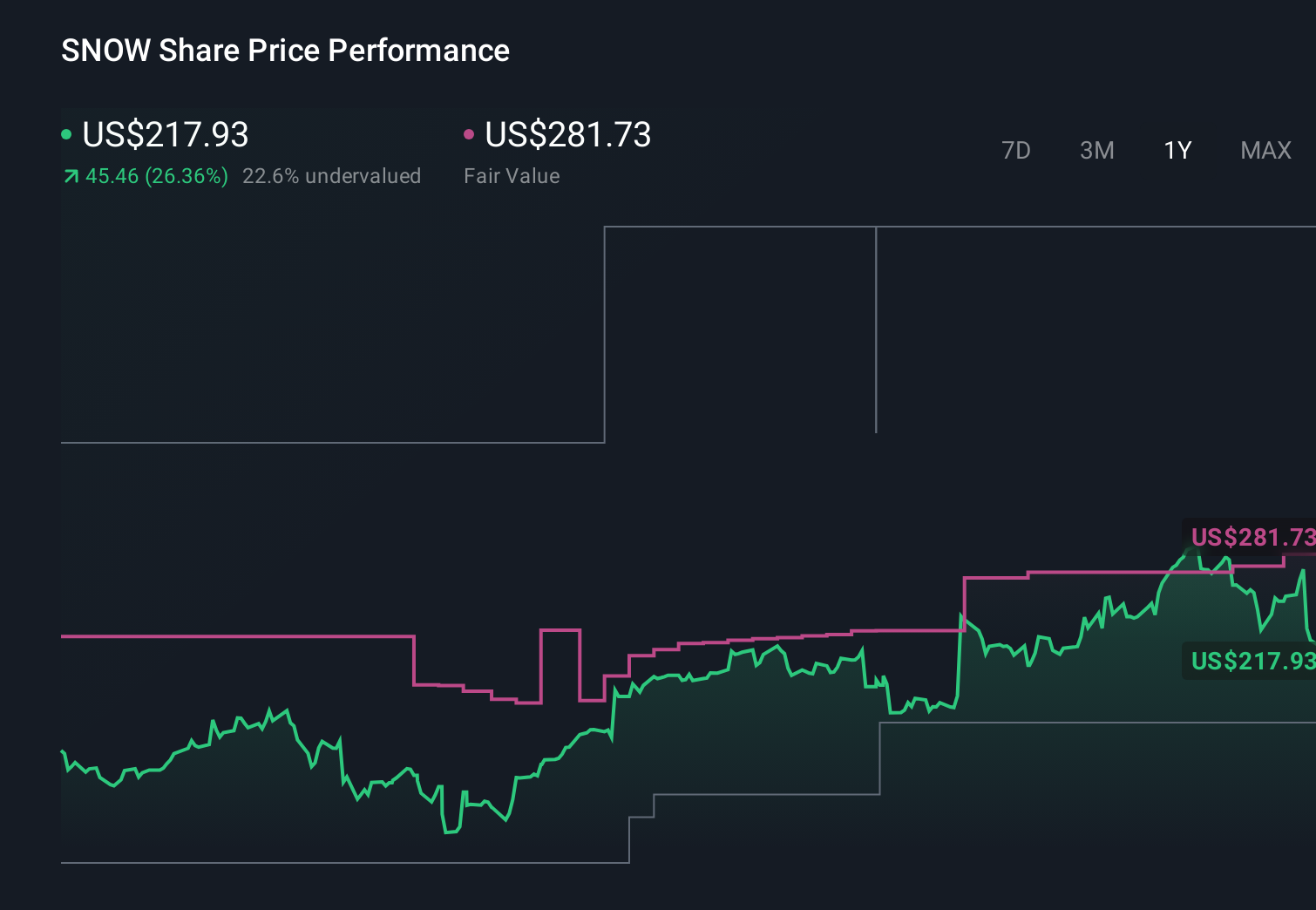

Snowflake’s narrative projects $9.0 billion revenue and $689.7 million earnings by 2029. This requires 24.5% yearly revenue growth and about a $2.0 billion earnings increase from -$1.3 billion today.

Uncover how Snowflake's forecasts yield a $232.74 fair value, a 61% upside to its current price.

Exploring Other Perspectives

Some of the lowest analysts were already cautious, assuming roughly 22.6% annual revenue growth and no profits within three years, so you should expect their views on AI updates and competitive risks to evolve as the impact of Snowflake Intelligence and Cortex Code on real world customer spend becomes clearer.

Explore 14 other fair value estimates on Snowflake - why the stock might be worth 45% less than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Snowflake research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Snowflake research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Snowflake's overall financial health at a glance.

Ready For A Different Approach?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Capitalize on the AI infrastructure supercycle with our selection of the 38 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Rare earth metals are the new gold rush. Find out which 32 stocks are leading the charge.

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:SNOW

Snowflake

Provides a cloud-based data platform for various organizations in the United States and internationally.

Excellent balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Unicycive Therapeutics ·

Looking to be second time lucky with a game-changing new product

Fair Value:US$21.5361.6% undervalued

139 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

DE

Degen_GCR on Everpure ·

Second order memory play likely to double in a year

Fair Value:US$18054.9% undervalued

23 followersusers have followed this narrative

1 commentusers have commented on this narrative

15 likesusers have liked this narrative

DO

Double_Bubbler on Intuitive Machines ·

Intuitive Machines: To The Moon and Beyond!

Fair Value:US$42.319.9% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

YI

yiannisz on AppLovin ·

AppLovin’s AI Engine Is Printing Profit

Fair Value:US$989.2449.4% undervalued

33 followersusers have followed this narrative

2 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

KA

kapirey on STIF Société anonyme ·

STIF Société anonyme will achieve 14% revenue growth with a focus on future gains

Fair Value:€43.6317.4% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KA

kapirey on Palantir Technologies ·

Palantir is strategic geopolitical asset at the intersection of AI, defense, and Western alliances.

Fair Value:US$120.1411.5% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KA

kapirey on Village Farms International ·

VFF is a vertically integrated, low-cost cannabis producer

Fair Value:US$4.7244.7% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8590.6% undervalued

111 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

TR

tripledub on Meta Platforms ·

The $135 Billion Bet That Should Make Every Shareholder Nervous

Fair Value:US$74017.0% undervalued

38 followersusers have followed this narrative

3 commentsusers have commented on this narrative

33 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$268.6116.1% undervalued

1182 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative