- United States

- /

- Software

- /

- NYSE:NOW

ServiceNow (NYSE:NOW) Partners With Saifr To Enhance Financial Services Operations

Reviewed by Simply Wall St

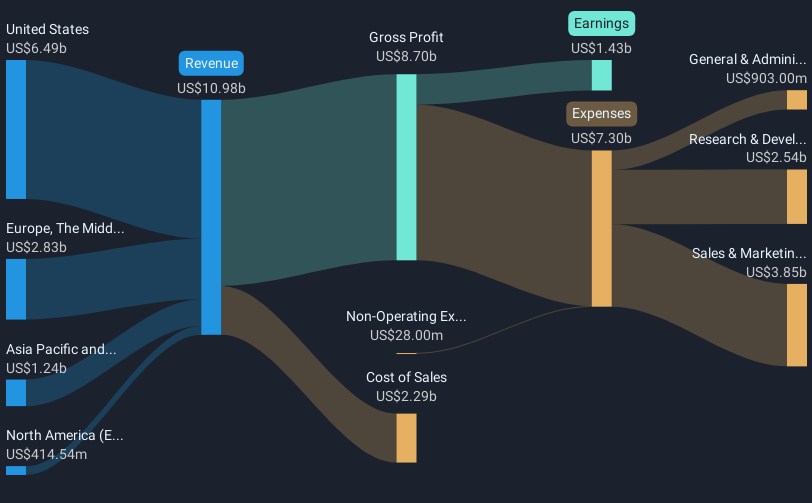

ServiceNow (NYSE:NOW) experienced a significant price move of 24% over the last quarter, possibly influenced by recent key developments. A notable event was its collaboration with Saifr to enhance adverse media and sanctions monitoring, promising advancements in compliance and regulatory frameworks. This development, together with expanded partnerships involving AI integrations announced during the period, such as with Black Kite, could have bolstered investor confidence. The S&P 500's broader upward trend coincided with ServiceNow's own growth, suggesting these developments added weight to the market's upward momentum rather than countering it.

We've spotted 2 possible red flags for ServiceNow you should be aware of.

The recent collaboration between ServiceNow and Saifr, along with expanded AI partnerships, could influence the company's revenue and earnings forecasts. These developments may attract increased attention in AI-driven markets, potentially boosting long-term growth prospects but also presenting near-term challenges. Such strategic moves might lead to fluctuations in short-term earnings visibility as the company transitions to hybrid consumption and subscription models for AI products. Specifically, the initial impact on revenue could be subdued as consumption-based monetization affects revenue recognition timing.

Over the past five years, ServiceNow's shares have delivered a total return of very large at 150.68%, highlighting robust growth, though recent shifts in industry dynamics and competitive pressures may introduce headwinds. In the shorter term, ServiceNow outperformed the US Software industry, which posted a return of 18.5% over the past year, underscoring its capable navigation of market challenges relative to peers. The current share price of US$812.70 reflects a slight discount to the consensus price target of approximately US$1,084.14, indicating potential for future appreciation as analysts weigh the implications of strategic initiatives.

Click to explore a detailed breakdown of our findings in ServiceNow's financial health report.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:NOW

ServiceNow

Provides cloud-based solution for digital workflows in the North America, Europe, the Middle East and Africa, Asia Pacific, and internationally.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion