Advertisement

- United States

- /

- Software

- /

- NYSE:NOW

ServiceNow (NOW): Rethinking Valuation After a Sharp Pullback in Share Price

ServiceNow (NOW) shares have been under pressure lately, slipping over the past week and month. This has investors asking whether the recent pullback reflects changing fundamentals or simply sentiment catching up with earlier gains.

See our latest analysis for ServiceNow.

Zooming out, the 1 year total shareholder return of minus 29.72 percent and a 90 day share price return of minus 20.21 percent suggest momentum has clearly faded, even though the 3 year total shareholder return of 100.83 percent still points to strong long term value creation.

If this reset in sentiment has you rethinking your tech exposure, it could be a good moment to scan other high growth tech and AI stocks that might fit your strategy better.

With shares down sharply despite double digit revenue and earnings growth, and the stock trading well below consensus price targets, investors now face a key question: Is ServiceNow a contrarian buy, or is future growth already priced in?

Most Popular Narrative: 86.7% Undervalued

Compared with ServiceNow’s last close at $153.38, the most followed narrative pegs fair value far higher, implying a steep disconnect between price and expectations.

In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $20.3 billion, earnings will come to $3.3 billion, and it would be trading on a PE ratio of 93.7x, assuming you use a discount rate of 8.4%.

Want to know how revenue, margins and a sky high future earnings multiple all combine to justify that appraisal? The surprising growth runway behind this projection is anything but ordinary. Curious which assumptions turn today’s selloff into tomorrow’s upside story? Read on to see what is driving that fair value.

Result: Fair Value of $1,154.54 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that upside assumes flawless execution, and setbacks in AI integration or tightening US federal tech budgets could quickly undercut today’s bullish valuation case.

Find out about the key risks to this ServiceNow narrative.

Another View: Valuation Signals Are Split

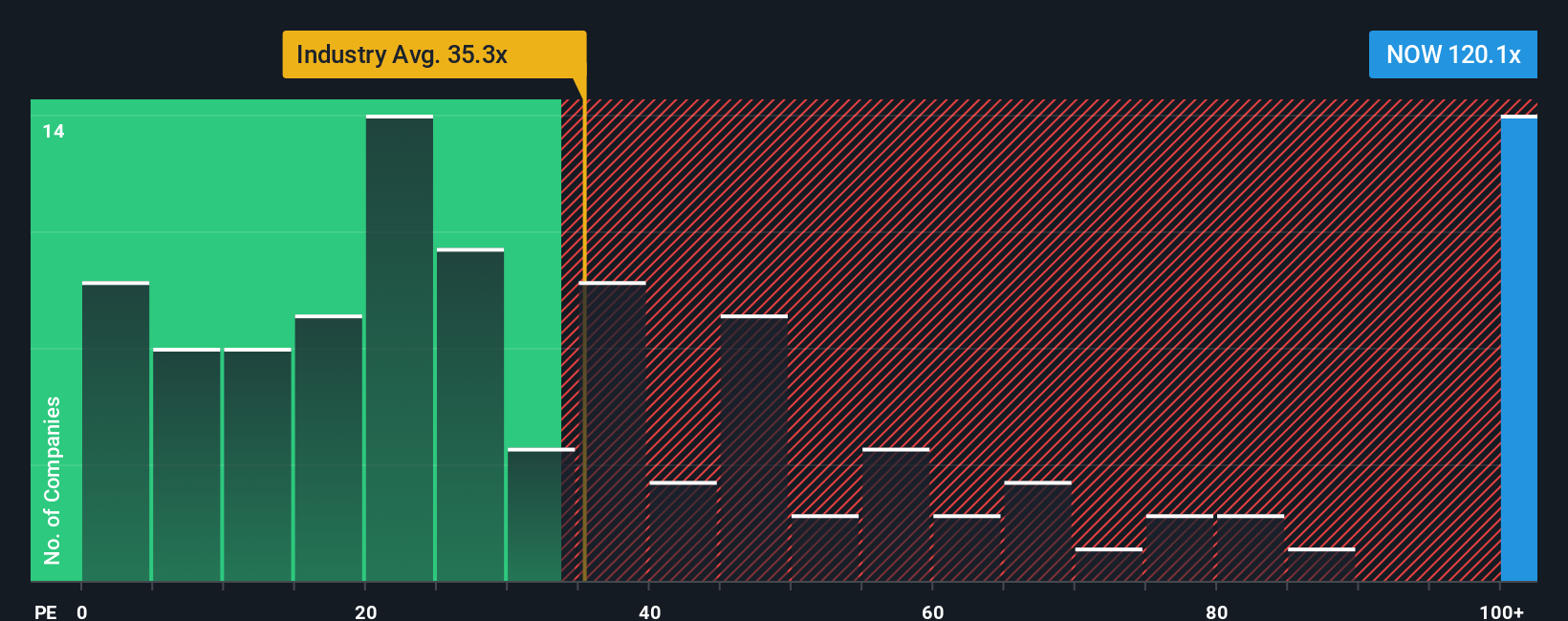

On earnings, the picture looks very different. ServiceNow trades on a P/E of 91.9 times versus about 31.2 times for the wider US software sector and a peer average of 50.3 times, while our fair ratio sits near 46.1 times. That kind of gap can close quickly, but it is unclear which way it will move first.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own ServiceNow Narrative

If you are unconvinced by this view, or prefer to examine the numbers yourself, you can build a complete narrative in minutes: Do it your way.

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding ServiceNow.

Looking for more investment ideas?

Use the Simply Wall Street Screener now to pinpoint fresh opportunities that match your strategy, before other investors crowd into the same trades.

- Capture high-upside names early by targeting these 3623 penny stocks with strong financials with fundamentals strong enough to support the next leg of your portfolio’s growth.

- Position your capital where innovation is accelerating by focusing on these 24 AI penny stocks shaping the future of intelligent software and automation.

- Identify potential mispricings today with these 915 undervalued stocks based on cash flows that cash flow models suggest the market has not fully appreciated yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:NOW

ServiceNow

Provides cloud-based solution for digital workflows in the North America, Europe, the Middle East and Africa, Asia Pacific, and internationally.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0776.3% undervalued

143 followersusers have followed this narrative

1 commentusers have commented on this narrative

24 likesusers have liked this narrative

CL

Clive_Thompson on Hermès International Société en commandite par actions ·

Hermès - Expensive bags, and expensive stock. And the story of €14 billion of bearer shares gone missing.

Fair Value:€1.51k22.4% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

SU

superbullll on Cheniere Energy ·

Cheniere Energy (LNG) — The Toll Road That Geopolitics Just Made More Valuable

Fair Value:US$320.9421.6% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

SA

Salman2415 on GNG Electronics ·

Strong execution in a growing category, but long‑term value hinges on cash‑flow discipline

Fair Value:₹135.87177.0% overvalued

5 followersusers have followed this narrative

1 commentusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

BO

BonSquid88 on Micron Technology ·

Micron Technology will experience a robust 16.5% revenue growth

Fair Value:US$55016.1% undervalued

40 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on Red Cat Holdings ·

Red Cat Holdings (RCAT): The Small-Drone Contender Bracing for Q4 Impact

Fair Value:US$18.458.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on Micron Technology ·

Micron Technology Inc. (MU): The "Silicon Gold" Rush Reaches a Fever Pitch

Fair Value:US$4956.7% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.377.8% undervalued

54 followersusers have followed this narrative

3 commentsusers have commented on this narrative

29 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9824.4% undervalued

45 followersusers have followed this narrative

0 commentsusers have commented on this narrative

34 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59633.0% undervalued

1312 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

Trending Discussion

DA

daqui_luis on Corticeira Amorim S.G.P.S ·

Great analysis on a great and solid company with a dominant position in the Cork Market.

1

|0