Advertisement

- United States

- /

- IT

- /

- NYSE:CINT

CI&T (NYSE:CINT) Might Be Having Difficulty Using Its Capital Effectively

What trends should we look for it we want to identify stocks that can multiply in value over the long term? Firstly, we'd want to identify a growing return on capital employed (ROCE) and then alongside that, an ever-increasing base of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. Although, when we looked at CI&T (NYSE:CINT), it didn't seem to tick all of these boxes.

What Is Return On Capital Employed (ROCE)?

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. The formula for this calculation on CI&T is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

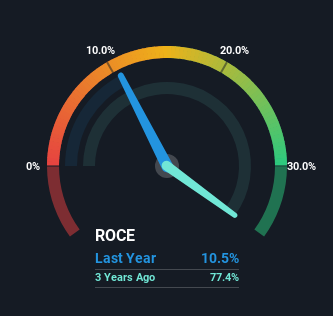

0.10 = R$252m ÷ (R$3.0b - R$600m) (Based on the trailing twelve months to June 2024).

So, CI&T has an ROCE of 10%. That's a pretty standard return and it's in line with the industry average of 10%.

See our latest analysis for CI&T

Above you can see how the current ROCE for CI&T compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like to see what analysts are forecasting going forward, you should check out our free analyst report for CI&T .

The Trend Of ROCE

In terms of CI&T's historical ROCE movements, the trend isn't fantastic. Around five years ago the returns on capital were 55%, but since then they've fallen to 10%. On the other hand, the company has been employing more capital without a corresponding improvement in sales in the last year, which could suggest these investments are longer term plays. It may take some time before the company starts to see any change in earnings from these investments.

On a side note, CI&T has done well to pay down its current liabilities to 20% of total assets. That could partly explain why the ROCE has dropped. Effectively this means their suppliers or short-term creditors are funding less of the business, which reduces some elements of risk. Some would claim this reduces the business' efficiency at generating ROCE since it is now funding more of the operations with its own money.

The Bottom Line

Bringing it all together, while we're somewhat encouraged by CI&T's reinvestment in its own business, we're aware that returns are shrinking. Since the stock has declined 65% over the last three years, investors may not be too optimistic on this trend improving either. All in all, the inherent trends aren't typical of multi-baggers, so if that's what you're after, we think you might have more luck elsewhere.

While CI&T doesn't shine too bright in this respect, it's still worth seeing if the company is trading at attractive prices. You can find that out with our FREE intrinsic value estimation for CINT on our platform.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:CINT

CI&T

Provides strategy, design, and software engineering services in North America, Europe, Latin America, Asia Pacific, and worldwide.

Very undervalued with flawless balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7058.5% undervalued

21 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

HE

HedgeY on AST SpaceMobile ·

AST SpaceMobile: The Boldest Direct-to-Cell Bet in Public Markets

Fair Value:US$17045.8% undervalued

43 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative

FU

FundamentalFlow on Onto Innovation ·

Onto Innovation: The Advanced Packaging Chokepoint 51.3% undervalued intrinsic discount

Fair Value:US$38029.2% undervalued

26 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7449.0% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

Recently Updated Narratives

RE

REElax on Volta Metals ·

Springer REE deposit valuation

Fair Value:CA$3.595.0% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

davidlsander on Atlas Salt ·

Once In A Life Time Deeply Discounted Recession Proof Utility

Fair Value:CA$2.9656.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PI

PittTheYounger on SSAB ·

SSAB in pole position when it comes to the combination of steel tariffs and the EU's investment drive

Fair Value:SEK 79.1721.8% overvalued

63 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7449.0% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9723.3% undervalued

57 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1933.9% undervalued

48 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

Trending Discussion

KA

Karndog on Berkshire Hathaway ·

Abel is also an Energy expert. He's already on the AI train even without "buying tech".

0

|0

SI

Simply Wall St User on Automatic Data Processing ·

This stock with dividend Aristocrat status and real annual increases may require more time to ascert...

0

|0

SI

Simply Wall St User on Access Holdings ·

It's wonderful. It has greatly helped me take informed decisions.

0

|0