Advertisement

- United States

- /

- Professional Services

- /

- NYSE:DAY

Earnings Miss: Ceridian HCM Holding Inc. Missed EPS By 5.4% And Analysts Are Revising Their Forecasts

Last week, you might have seen that Ceridian HCM Holding Inc. (NYSE:CDAY) released its full-year result to the market. The early response was not positive, with shares down 8.7% to US$66.91 in the past week. It looks like the results were a bit of a negative overall. While revenues of US$824m were in line with analyst predictions, statutory earnings were less than expected, missing estimates by 5.4% to hit US$0.53 per share. Following the result, analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. So we collected the latest post-earnings statutory consensus estimates to see what could be in store for next year.

View our latest analysis for Ceridian HCM Holding

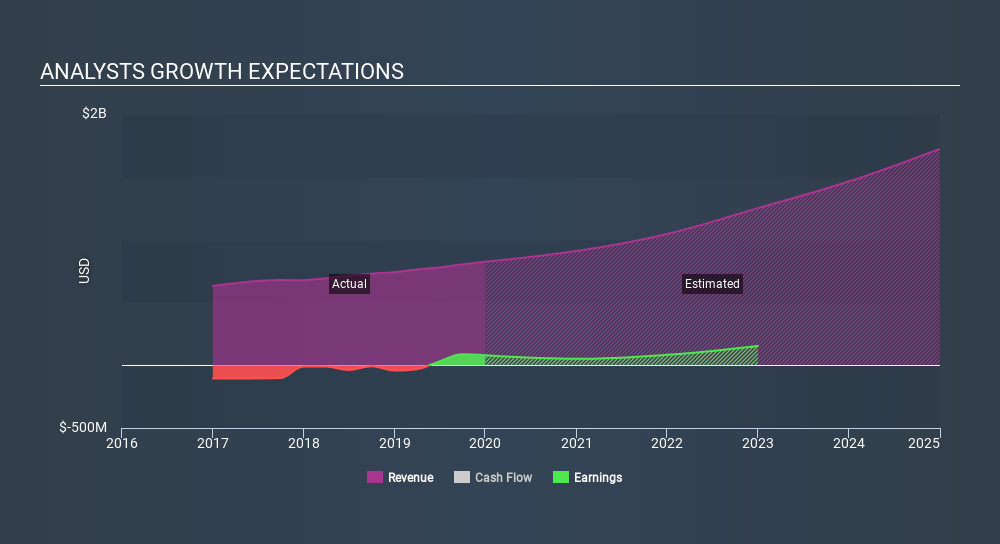

Taking into account the latest results, the latest consensus from Ceridian HCM Holding's 15 analysts is for revenues of US$908.4m in 2020, which would reflect a solid 10% improvement in sales compared to the last 12 months. Statutory earnings per share are expected to crater 53% to US$0.26 in the same period. Yet prior to the latest earnings, analysts had been forecasting revenues of US$928.8m and earnings per share (EPS) of US$0.43 in 2020. Analysts seem less optimistic after the recent results, reducing their sales forecasts and making a large cut to earnings per share forecasts.

Despite the cuts to forecast earnings, there was no real change to the US$72.31 price target, showing that analysts don't think the changes have a meaningful impact on the stock's intrinsic value. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. Currently, the most bullish analyst values Ceridian HCM Holding at US$87.00 per share, while the most bearish prices it at US$43.00. Note the wide gap in analyst price targets? This implies to us that there is a fairly broad range of possible scenarios for the underlying business.

In addition, we can look to Ceridian HCM Holding's past performance and see whether business is expected to improve, and if the company is expected to perform better than wider market. We can infer from the latest estimates that analysts are expecting a continuation of Ceridian HCM Holding's historical trends, as next year's forecast 10% revenue growth is roughly in line with 8.8% annual revenue growth over the past three years. Compare this with the wider market, which analyst estimates (in aggregate) suggest will see revenues grow 12% next year. It's clear that while Ceridian HCM Holding's revenue growth is expected to continue on its current trajectory, it's only expected to grow in line with the market itself.

The Bottom Line

The most important thing to take away is that analysts downgraded their earnings per share estimates, showing that there has been a clear decline in sentiment following these results. Lamentably, they also downgraded their sales forecasts, but the business is still expected to grow at roughly the same rate as the market itself. The consensus price target held steady at US$72.31, with the latest estimates not enough to have an impact on analysts' estimated valuations.

With that in mind, we wouldn't be too quick to come to a conclusion on Ceridian HCM Holding. Long-term earnings power is much more important than next year's profits. We have forecasts for Ceridian HCM Holding going out to 2024, and you can see them free on our platform here.

It might also be worth considering whether Ceridian HCM Holding's debt load is appropriate, using our debt analysis tools on the Simply Wall St platform, here.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NYSE:DAY

Dayforce

Operates as a human capital management (HCM) software company in the United States, Canada, Australia, and internationally.

Reasonable growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|33.3% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|23.4% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|8.5% overvalued

DA

Community Contributor