Advertisement

- United States

- /

- Software

- /

- NYSE:BOX

Box (NYSE:BOX) Is Doing The Right Things To Multiply Its Share Price

What are the early trends we should look for to identify a stock that could multiply in value over the long term? Firstly, we'll want to see a proven return on capital employed (ROCE) that is increasing, and secondly, an expanding base of capital employed. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. So when we looked at Box (NYSE:BOX) and its trend of ROCE, we really liked what we saw.

What Is Return On Capital Employed (ROCE)?

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. To calculate this metric for Box, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.10 = US$60m ÷ (US$1.2b - US$591m) (Based on the trailing twelve months to April 2024).

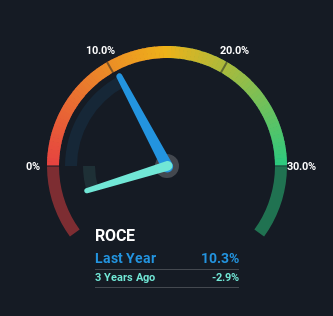

So, Box has an ROCE of 10%. In absolute terms, that's a satisfactory return, but compared to the Software industry average of 7.2% it's much better.

Check out our latest analysis for Box

Above you can see how the current ROCE for Box compares to its prior returns on capital, but there's only so much you can tell from the past. If you're interested, you can view the analysts predictions in our free analyst report for Box .

What Does the ROCE Trend For Box Tell Us?

Box has recently broken into profitability so their prior investments seem to be paying off. The company was generating losses five years ago, but now it's earning 10% which is a sight for sore eyes. In addition to that, Box is employing 53% more capital than previously which is expected of a company that's trying to break into profitability. This can tell us that the company has plenty of reinvestment opportunities that are able to generate higher returns.

Another thing to note, Box has a high ratio of current liabilities to total assets of 50%. This can bring about some risks because the company is basically operating with a rather large reliance on its suppliers or other sorts of short-term creditors. Ideally we'd like to see this reduce as that would mean fewer obligations bearing risks.

The Key Takeaway

In summary, it's great to see that Box has managed to break into profitability and is continuing to reinvest in its business. And with a respectable 46% awarded to those who held the stock over the last five years, you could argue that these developments are starting to get the attention they deserve. With that being said, we still think the promising fundamentals mean the company deserves some further due diligence.

If you'd like to know about the risks facing Box, we've discovered 1 warning sign that you should be aware of.

While Box may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

Valuation is complex, but we're here to simplify it.

Discover if Box might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:BOX

Box

Provides a cloud content management platform that enables organizations of various sizes to manage cloud content from anywhere and on any device in Poland, Australia, Canada, the European Union, France, Israel, Japan, Singapore, Switzerland, the United Kingdom, and the United States.

Flawless balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Giftify ·

Giftify ($GIFT): A Small-Cap Incentives Platform with More ScaleThan Its Valuation Suggests

Fair Value:US$2.562.2% undervalued

33 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

HA

HarishPK on lululemon athletica ·

Quantifying the Transition: Why Lululemon’s Moat Remains Intact

Fair Value:US$161.828.9% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$23059.6% overvalued

39 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

JO

John_Eric on Veeva Systems ·

AI-Powered Veeva Systems Poised for Solid Growth Amid Regulatory Stability

Fair Value:US$32039.9% undervalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Recently Updated Narratives

BL

Blagget on BP Silver ·

“valer un Potosí” GOOGLE IT. Now you’re should be kinda locked in. Educate yourself, Read the rest.

Fair Value:CA$685.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TimLee on Master Tec Group Berhad ·

Master Tec’s TNB Extension Reinforces Its Utility-Scale Growth Story

Fair Value:RM 1.6841.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

danmad on Judo Capital Holdings ·

A Fast-Growing SME Lender Trading Like a Problem Bank

Fair Value:AU$0.954.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75029.1% undervalued

84 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9630.8% undervalued

64 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5457.5% undervalued

59 followersusers have followed this narrative

3 commentsusers have commented on this narrative

10 likesusers have liked this narrative