Advertisement

- United States

- /

- Software

- /

- NasdaqGS:ZM

Zoom (ZM): Valuation in Focus After Strong Q2, Raised Guidance, and New AI-Powered Launches

Kshitija Bhandaru

Reviewed by Simply Wall St

If you have been eyeing Zoom Communications (ZM), this week’s earnings and product updates might feel like the moment you have been waiting for. Zoom just turned in stronger than expected profits for the second quarter, accompanied by a raised outlook for full-year 2026. This is a confident signal from management that they see more growth ahead. On top of this, the fresh rollout of AI-powered features such as Zoom Virtual Agent for Phone, the new Zoom Hub, and enhanced AI Companion tools makes it clear that Zoom is intent on staking a claim in the evolving world of unified communications.

Over the past year, the stock has posted a 17.9% gain, reversing a period of sluggishness and shaking off a nearly flat run in the past three months. Recent launches in AI and product integration seem to be reigniting investor interest, especially as profitability edges higher. While the longer five-year picture shows the share price still working its way back from earlier highs, the combination of stable revenue growth and expanding margins suggests momentum that could carry forward.

With shares rebounding and a stronger outlook, investors may wonder whether Zoom is trading at a bargain or if the market has already priced in the promise of future AI-led expansion.

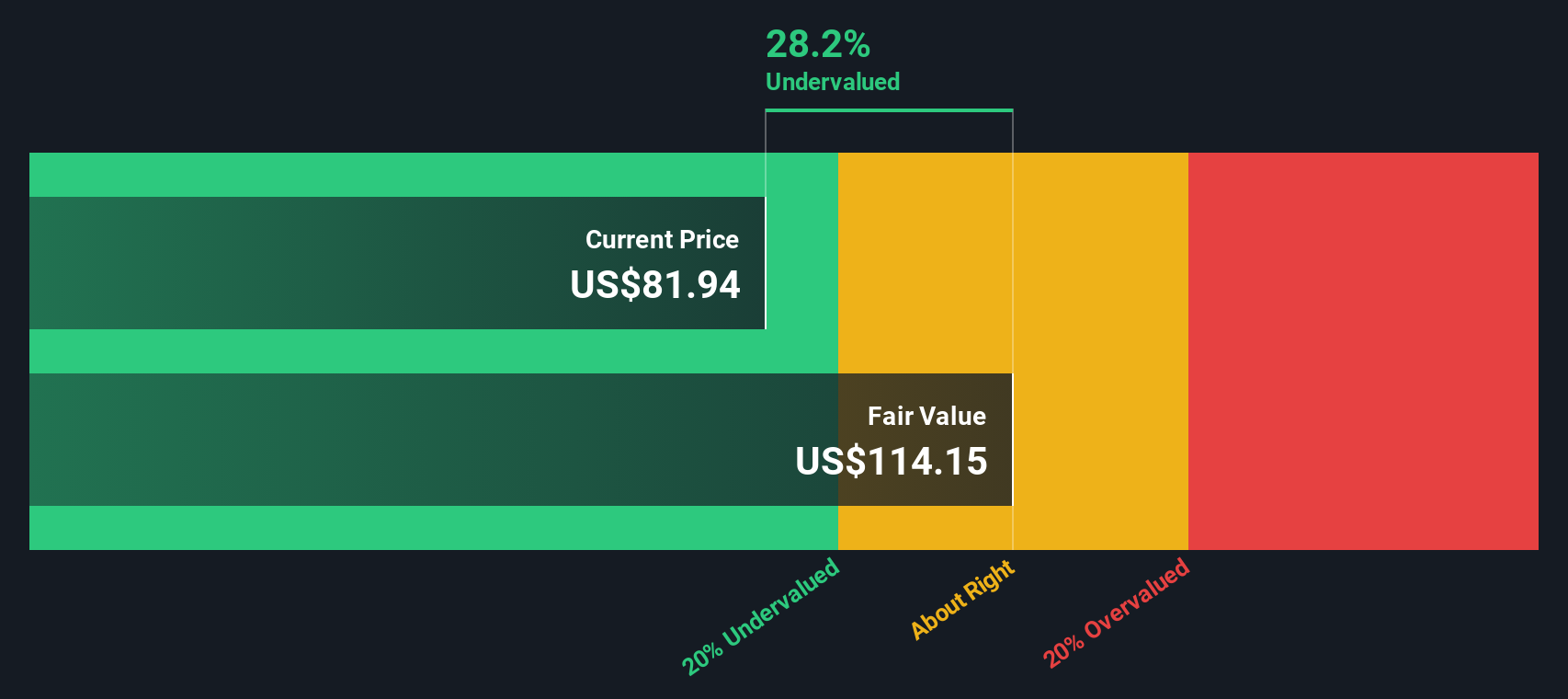

Most Popular Narrative: 11.1% Undervalued

According to community narrative, Zoom Communications is viewed as undervalued relative to its consensus fair value, based on future earnings growth and profitability projections.

Strong and accelerating adoption of AI-powered features, such as AI Companion, Virtual Agent 2.0, and Contact Center Elite, demonstrates growing customer reliance on advanced collaboration and productivity tools. This positions Zoom at the forefront of enterprise digital transformation and is likely to expand the addressable market, drive multi-year revenue growth, and increase recurring revenue stability.

What is fueling this positive outlook? The most popular narrative points to bold growth assumptions, margin trends, and a valuation path that could surprise even seasoned investors. Think you know what drives this double-digit fair value gap? The real story behind analyst confidence may prompt you to reconsider your own valuation instincts.

Result: Fair Value of $91.63 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, intensifying competition from larger, integrated platforms and potential challenges in monetizing new AI features could threaten Zoom's growth and profitability assumptions.

Find out about the key risks to this Zoom Communications narrative.Another View: SWS DCF Model

Looking at Zoom through the lens of our DCF model adds an extra layer of perspective. This method also points to undervaluation and suggests the market may not be fully factoring in future potential. Can two different approaches really agree?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Zoom Communications for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Zoom Communications Narrative

If you want a different take or prefer hands-on research, explore the numbers and piece together your own perspective in just minutes. Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Zoom Communications.

Ready for More Winning Ideas?

Serious about growing your portfolio? There’s no reason to stick to one stock when some of the market’s best investment opportunities are just waiting to be uncovered. Don’t let a great idea pass you by. Take charge and act while others hesitate.

- Spot high-potential opportunities by screening for companies matching undervalued cash flow criteria using undervalued stocks based on cash flows.

- Unlock the latest breakthroughs in artificial intelligence by tracking innovators shaping tomorrow’s technology via AI penny stocks.

- Secure steady income streams by targeting companies offering strong yields through dividend stocks with yields > 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Zoom Communications might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Kshitija Bhandaru

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.

About NasdaqGS:ZM

Zoom Communications

Provides an Artificial Intelligence-first work platform for human connection in the Americas, the Asia Pacific, Europe, the Middle East, and Africa.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Defense AI: A Robotic Response to America’s Security Gaps

Fair Value US$12.00|49.7% undervalued

MA

Community Contributor

Figma (FIG): The S&P 500’s Design Standard Turning Into an All-in-One Platform

Fair Value US$65.70|7.0% overvalued

TI

Community Contributor

Sleep Cycle's Revenue Set to Rise 10% with Strong Revenue Model

Fair Value SEK 38.04|20.3% undervalued

MA

Community Contributor

Has JB Hi-Fi Lost Its Point of Difference?

Fair Value AU$76.00|54.2% overvalued

RO

Community Contributor