Advertisement

- United States

- /

- Software

- /

- NasdaqGS:WDAY

Workday (NASDAQ:WDAY) Is Doing The Right Things To Multiply Its Share Price

If you're not sure where to start when looking for the next multi-bagger, there are a few key trends you should keep an eye out for. Firstly, we'd want to identify a growing return on capital employed (ROCE) and then alongside that, an ever-increasing base of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. With that in mind, we've noticed some promising trends at Workday (NASDAQ:WDAY) so let's look a bit deeper.

What Is Return On Capital Employed (ROCE)?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. The formula for this calculation on Workday is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

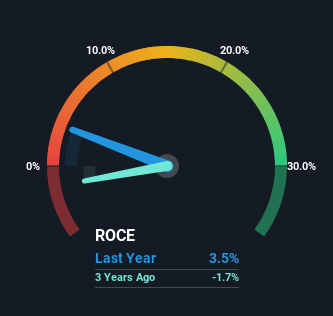

0.035 = US$419m ÷ (US$16b - US$4.4b) (Based on the trailing twelve months to October 2024).

Therefore, Workday has an ROCE of 3.5%. In absolute terms, that's a low return and it also under-performs the Software industry average of 8.3%.

Check out our latest analysis for Workday

Above you can see how the current ROCE for Workday compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like to see what analysts are forecasting going forward, you should check out our free analyst report for Workday .

What Does the ROCE Trend For Workday Tell Us?

Workday has recently broken into profitability so their prior investments seem to be paying off. The company was generating losses five years ago, but now it's earning 3.5% which is a sight for sore eyes. Not only that, but the company is utilizing 228% more capital than before, but that's to be expected from a company trying to break into profitability. This can tell us that the company has plenty of reinvestment opportunities that are able to generate higher returns.

In another part of our analysis, we noticed that the company's ratio of current liabilities to total assets decreased to 27%, which broadly means the business is relying less on its suppliers or short-term creditors to fund its operations. Therefore we can rest assured that the growth in ROCE is a result of the business' fundamental improvements, rather than a cooking class featuring this company's books.

Our Take On Workday's ROCE

To the delight of most shareholders, Workday has now broken into profitability. And with a respectable 42% awarded to those who held the stock over the last five years, you could argue that these developments are starting to get the attention they deserve. With that being said, we still think the promising fundamentals mean the company deserves some further due diligence.

On the other side of ROCE, we have to consider valuation. That's why we have a FREE intrinsic value estimation for WDAY on our platform that is definitely worth checking out.

While Workday may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

Valuation is complex, but we're here to simplify it.

Discover if Workday might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:WDAY

Workday

Provides enterprise cloud applications in the United States and internationally.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7058.5% undervalued

21 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

HE

HedgeY on AST SpaceMobile ·

AST SpaceMobile: The Boldest Direct-to-Cell Bet in Public Markets

Fair Value:US$17045.8% undervalued

43 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative

FU

FundamentalFlow on Onto Innovation ·

Onto Innovation: The Advanced Packaging Chokepoint 51.3% undervalued intrinsic discount

Fair Value:US$38029.2% undervalued

26 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7449.0% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

Recently Updated Narratives

RE

REElax on Volta Metals ·

Springer REE deposit valuation

Fair Value:CA$3.595.0% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

davidlsander on Atlas Salt ·

Once In A Life Time Deeply Discounted Recession Proof Utility

Fair Value:CA$2.9656.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PI

PittTheYounger on SSAB ·

SSAB in pole position when it comes to the combination of steel tariffs and the EU's investment drive

Fair Value:SEK 79.1721.8% overvalued

63 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7449.0% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9723.3% undervalued

57 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1933.9% undervalued

48 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

Trending Discussion

KA

Karndog on Berkshire Hathaway ·

Abel is also an Energy expert. He's already on the AI train even without "buying tech".

0

|0

SI

Simply Wall St User on Automatic Data Processing ·

This stock with dividend Aristocrat status and real annual increases may require more time to ascert...

0

|0

SI

Simply Wall St User on Access Holdings ·

It's wonderful. It has greatly helped me take informed decisions.

0

|0