- United States

- /

- Software

- /

- NasdaqGS:VRNS

How Investors May Respond To Varonis Systems (VRNS) Earnings Miss and New Securities Investigation

Reviewed by Sasha Jovanovic

- Earlier in 2025, Varonis Systems reported third-quarter results that fell short of revenue forecasts, highlighting a sharp drop in term license subscription revenues and specific weakness in its on-premises subscription business.

- Soon after these disclosures, law firm Kaplan Fox & Kilsheimer LLP launched a securities law investigation into Varonis, underscoring investor concern about how the company communicated its performance and business transition challenges.

- We’ll now explore how the revenue shortfall and pressure on the on-premises subscription segment may influence Varonis Systems’ broader investment narrative.

Explore 28 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Varonis Systems Investment Narrative Recap

To own Varonis Systems, you need to believe its data security platform and SaaS shift can outweigh current execution issues and ongoing losses. The latest revenue miss and sharp drop in term license subscriptions directly pressure that thesis in the near term, since the most important short term catalyst is proof that its business transition can support stable, predictable growth. At the same time, the biggest risk now is that prolonged weakness in on premises subscriptions undermines confidence in that transition altogether.

Against this backdrop, Varonis’ December 2025 announcement of an integration with AWS Security Hub stands out, because it reinforces the core catalyst of deeper cloud adoption and broader platform coverage. While this integration helps extend Varonis’ reach across cloud environments and supports its SaaS centric story, investors may still weigh it against the immediate concerns raised by the third quarter revenue shortfall and the resulting securities law investigation.

Yet behind these growth ambitions, the pressure on on premises revenue and associated legal scrutiny is something investors should be aware of...

Read the full narrative on Varonis Systems (it's free!)

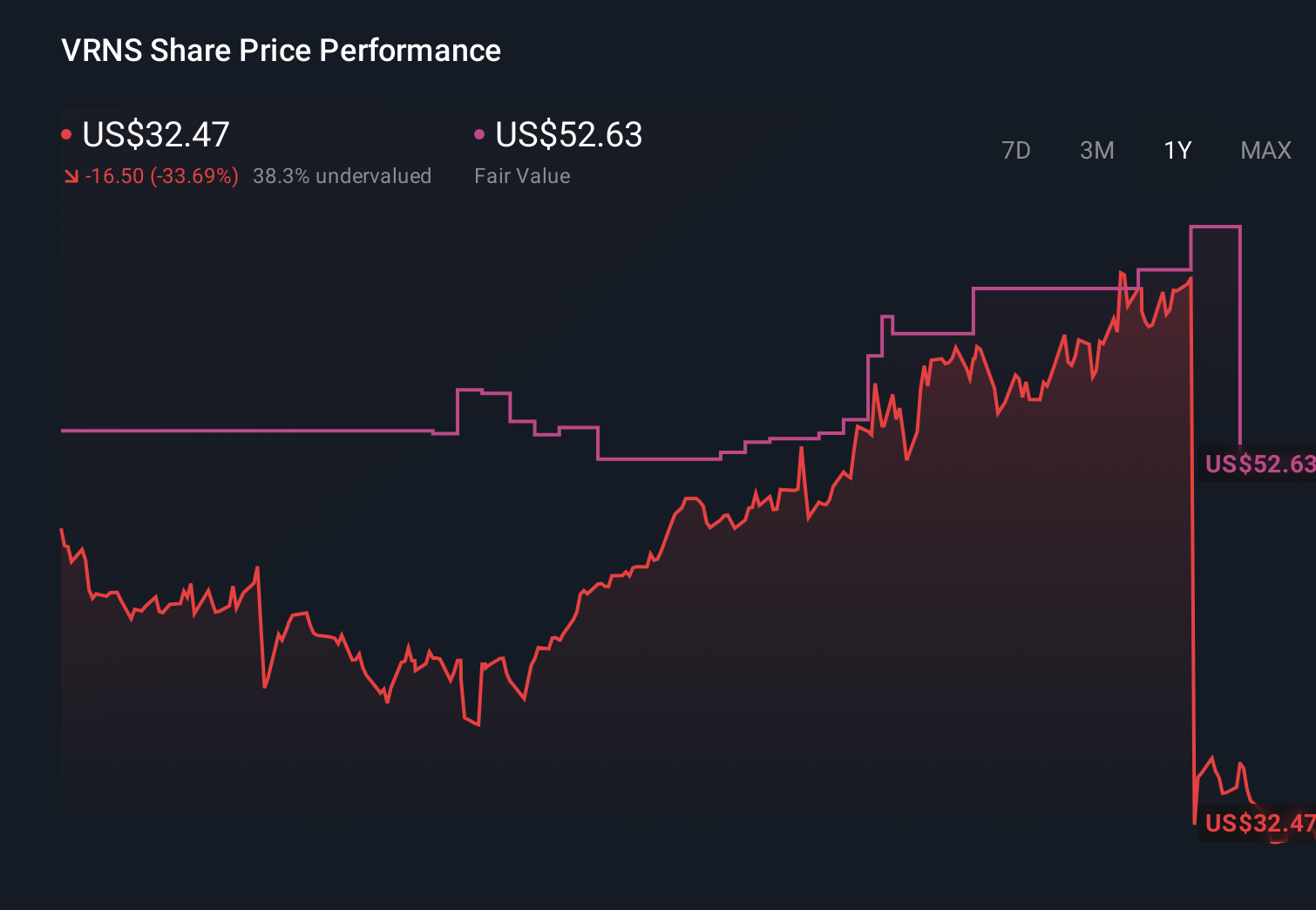

Varonis Systems’ narrative projects $911.4 million revenue and $119.3 million earnings by 2028. This requires 15.3% yearly revenue growth and an earnings increase of about $222 million from -$102.9 million today.

Uncover how Varonis Systems' forecasts yield a $52.63 fair value, a 58% upside to its current price.

Exploring Other Perspectives

Three fair value estimates from the Simply Wall St Community cluster between US$52.63 and US$70, highlighting how far opinions can stretch above the current share price. You should weigh those views against the risk that Varonis’ SaaS transition and recent revenue miss keep GAAP growth and profitability under pressure for longer, which could meaningfully affect how the story plays out.

Explore 3 other fair value estimates on Varonis Systems - why the stock might be worth just $52.63!

Build Your Own Varonis Systems Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Varonis Systems research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Varonis Systems research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Varonis Systems' overall financial health at a glance.

Curious About Other Options?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- These 16 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- We've found 13 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:VRNS

Varonis Systems

Provides software products and services that continuously discover and classify critical data, remediate exposures, and detect advanced threats with AI-powered technology in North America, Europe, APAC, and rest of world.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion