Advertisement

- United States

- /

- Software

- /

- NasdaqGS:VRNS

A Look At Varonis Systems (VRNS) Valuation After SaaS Progress And Atlas AI Launch

Why Varonis Systems (VRNS) is back on investors’ radar

Varonis Systems (VRNS) has drawn fresh attention after reporting 9.4% year on year revenue growth and 32% SaaS ARR growth, while issuing full year EPS guidance that came in below market expectations.

The company also launched its new Varonis Atlas AI Security Platform and is presenting at RSA Conference 2026. These developments are prompting investors to reassess the stock after its post earnings share price decline.

See our latest analysis for Varonis Systems.

At a share price of $23.72, Varonis has recorded a 90 day share price return of 28.62% and a 1 year total shareholder return of 42.68%. This performance comes amid interest around Atlas and the company’s appearances at the RSA Conference.

If this AI security story has your attention, it can be worth widening your watchlist to see how other AI exposed names compare by using our screener for 33 AI small caps

With Varonis trading at US$23.72, carrying an intrinsic discount estimate of roughly 49% and a mixed track record of recent returns, you need to ask: is this a reset entry point, or is the market already baking in future growth?

Most Popular Narrative: 30% Undervalued

The most followed narrative on Varonis puts fair value at $33.90, well above the last close at $23.72, and frames that gap around long term AI driven data security demand and the SaaS transition.

Rapid proliferation of enterprise data and increased AI adoption are materially boosting demand for automated, comprehensive data protection, positioning Varonis to capture higher revenue growth and expand its total addressable market as organizations prioritize data security for both compliance and risk mitigation.

Want to see what underpins that valuation gap? The narrative focuses on firm revenue expansion, a sharp margin shift, and a rich future earnings multiple that assumes those targets hold.

Result: Fair Value of $33.90 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that upside case depends on a smooth SaaS transition and resilient margins, and both competitive pressure and ongoing losses could easily challenge those assumptions.

Find out about the key risks to this Varonis Systems narrative.

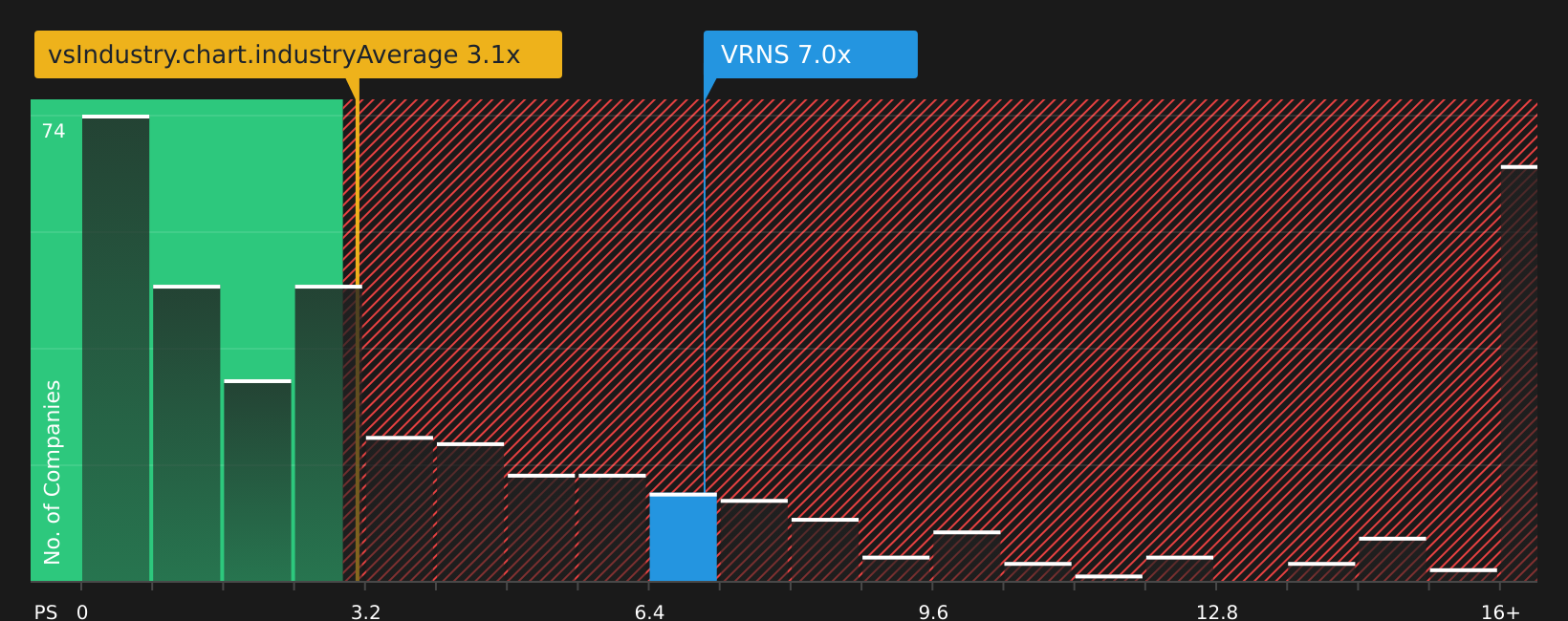

Another way to look at the valuation

While the Simply Wall St DCF model suggests Varonis is trading about 49% below an estimated future cash flow value of $46.59, the market is also pricing in a relatively rich 4.5x P/S ratio versus 3.3x for the US Software industry and 4x for peers. That mix of apparent discount and premium raises a simple question for you: are cash flow assumptions too cautious or are revenue multiples too optimistic?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

The mix of potential upside and ongoing questions around Varonis might feel finely balanced. It makes sense to review the numbers yourself, weigh the AI story against the current valuation, and then check how that aligns with the company’s 2 key rewards and 1 important warning sign

Looking for more investment ideas?

If you have come this far with Varonis, do not stop here. Broaden your opportunity set with a few targeted screens that keep you ahead of the crowd.

- Target potential mispricings by scanning for quality names trading below what their fundamentals suggest using our 54 high quality undervalued stocks.

- Prioritise resilience by focusing on companies with strong finances through the solid balance sheet and fundamentals stocks screener (39 results).

- Hunt for lesser known opportunities that still have solid fundamentals with the screener containing 26 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:VRNS

Varonis Systems

Provides software products and services that continuously discover and classify critical data, remediate exposures, and detect advanced threats with AI-powered technology in North America, Europe, APAC, and rest of worlds.

Flawless balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Unicycive Therapeutics ·

Looking to be second time lucky with a game-changing new product

Fair Value:US$21.5368.7% undervalued

92 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

CL

Clive_Thompson on Hermès International Société en commandite par actions ·

Hermès - Expensive bags, and expensive stock. And the story of €14 billion of bearer shares gone missing.

Fair Value:€1.51k10.0% overvalued

22 followersusers have followed this narrative

1 commentusers have commented on this narrative

23 likesusers have liked this narrative

SU

superbullll on Cheniere Energy ·

Cheniere Energy (LNG) — The Toll Road That Geopolitics Just Made More Valuable

Fair Value:US$320.9412.5% undervalued

22 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

SA

Salman2415 on GNG Electronics ·

Strong execution in a growing category, but long‑term value hinges on cash‑flow discipline

Fair Value:₹135.87179.9% overvalued

10 followersusers have followed this narrative

1 commentusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$27.5240.8% undervalued

52 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on TotalEnergies ·

Is This strategic transformation of TTE? Significant re-rating potential

Fair Value:€88.2912.8% undervalued

9 followersusers have followed this narrative

2 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on Silver X Mining ·

A Case for Silver X reaching CAD$18 by 2031 (a possible 30 bagger)

Fair Value:CA$1896.4% undervalued

1 followerusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.378.3% undervalued

55 followersusers have followed this narrative

3 commentsusers have commented on this narrative

29 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9826.5% undervalued

47 followersusers have followed this narrative

0 commentsusers have commented on this narrative

35 likesusers have liked this narrative

PD

pdixit1 on Vertiv Holdings Co ·

The Infrastructure AI Cannot Be Built Without

Fair Value:US$408.6437.4% undervalued

39 followersusers have followed this narrative

3 commentsusers have commented on this narrative

18 likesusers have liked this narrative

Trending Discussion

OD

Oddlott on lululemon athletica ·

Thankyou for the interesting comments. So what is the world wide including USA growth rate?

0

|0