Advertisement

- United States

- /

- Software

- /

- NasdaqGS:TRMB

Is Trimble (TRMB) Now Attractive After Recent Share Price Pullback?

Reviewed by Bailey Pemberton

- If you are wondering whether Trimble is starting to look attractively priced or still expensive at around recent levels, this article walks through the key valuation clues to help you frame that view.

- The share price has been mixed recently, with a 0.1% move over the last week, a 19.4% decline over 30 days, a 16.9% decline year to date, an 11.1% decline over 1 year, a 15.9% gain over 3 years, and a 10.1% decline over 5 years. This gives investors a wide range of reference points.

- These moves sit against a backdrop of ongoing interest in Trimble's role in sectors such as software enabled construction, agriculture, and geospatial solutions. These areas often attract investors who watch longer term technology adoption trends. Market sentiment around these themes, along with broader sector rotations, can help explain why the stock has seen both periods of strength and pullbacks across different time frames.

- Trimble currently has a valuation score of 3 out of 6, reflecting that it screens as undervalued on half of Simply Wall St's standard checks. Next, we will look at what different valuation methods suggest about that number and introduce an even more rounded way to judge value later in the article.

Approach 1: Trimble Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model projects a company’s future cash flows and then discounts them back to today to estimate what the business might be worth right now.

For Trimble, the model used is a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The latest twelve month free cash flow is about $353.5 million. Analysts have provided free cash flow estimates for the coming years, and Simply Wall St extends those projections further. By 2028, free cash flow is projected at $1.036b, with intermediate annual projections between 2026 and 2035 ranging from about $861.7 million to $1.409b before discounting.

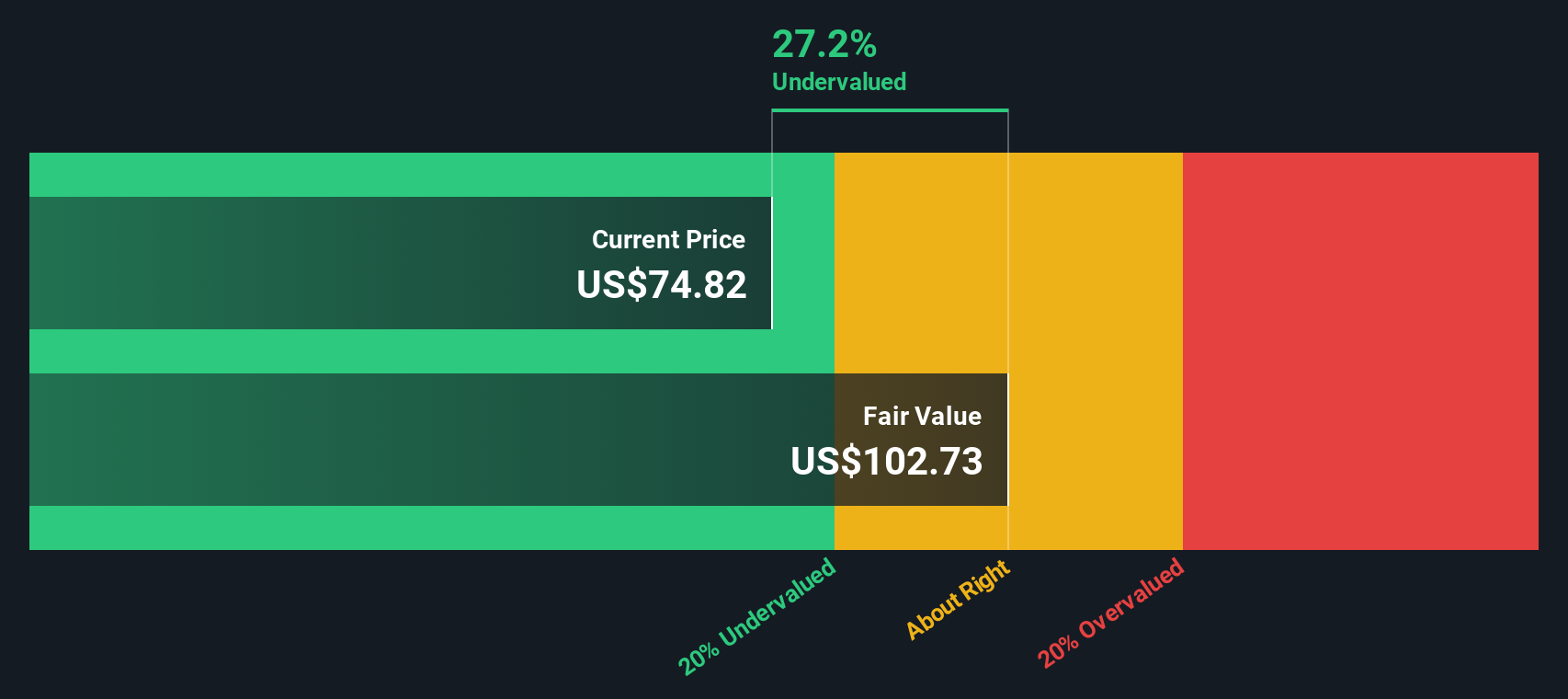

After discounting those projected cash flows back to today, the model arrives at an estimated intrinsic value of $81.90 per share. This implies the stock trades at about a 20.5% discount to that DCF estimate, which indicates that Trimble appears undervalued based on this cash flow view.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Trimble is undervalued by 20.5%. Track this in your watchlist or portfolio, or discover 51 more high quality undervalued stocks.

Approach 2: Trimble Price vs Earnings

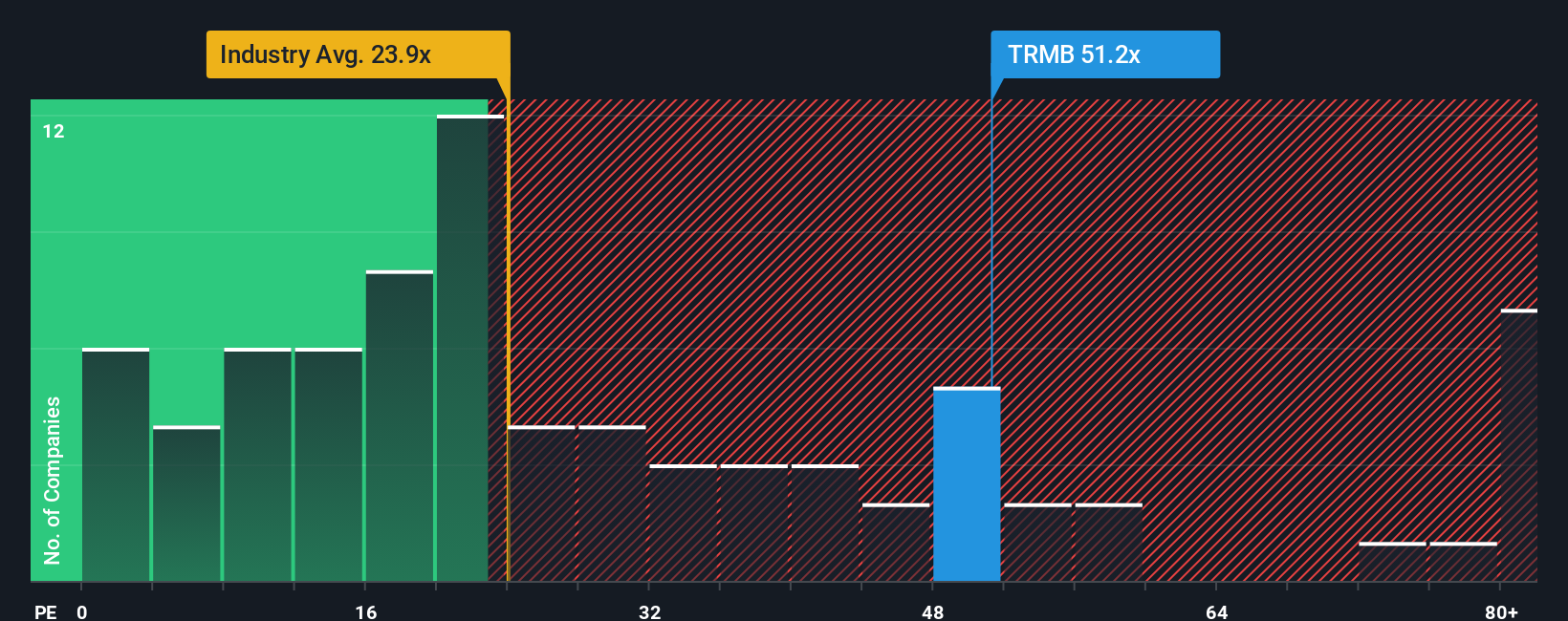

For a profitable company like Trimble, the P/E ratio is a helpful shorthand for how much investors are paying for each dollar of earnings. A higher or lower P/E often reflects what the market expects for future earnings growth and how much risk investors see in those earnings.

In simple terms, stronger expected growth and lower perceived risk can justify a higher “normal” P/E, while slower expected growth or higher risk usually point to a lower one. Trimble currently trades on a P/E of 36.55x. That sits above the Software industry average of 27.08x and also above the peer group average of 31.41x.

Simply Wall St’s Fair Ratio framework goes a step further by estimating what P/E might make sense for Trimble given its earnings growth profile, industry, profit margins, market cap and risk factors. For Trimble, this Fair Ratio is 32.58x. Because it folds in company specific fundamentals rather than just comparing with broad averages, it can be a more tailored guide to what investors might consider reasonable.

Comparing the current 36.55x P/E with the 32.58x Fair Ratio suggests Trimble screens as overvalued on this earnings based view.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 22 top founder-led companies.

Upgrade Your Decision Making: Choose your Trimble Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce Narratives, which let you connect your view of Trimble’s story to your own revenue, earnings and margin assumptions. You can then link that forecast to a Fair Value, and compare it with the current price using an easy tool on Simply Wall St’s Community page that updates when new information like earnings or news arrives. One investor might build a Trimble Narrative around the higher US$101 price target and another around the lower US$84 target, and you can decide for yourself where your Fair Value sits between those two anchors.

Do you think there's more to the story for Trimble? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Trimble might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:TRMB

Trimble

Offers technology solutions and platform that enable office professionals and field workers to connect workflows and industry lifecycles in North America, Europe, the Asia Pacific, and internationally.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0778.5% undervalued

197 followersusers have followed this narrative

1 commentusers have commented on this narrative

28 likesusers have liked this narrative

SI

SimpleMan887 on GameStop ·

GameStop will ace the financial crisis wave with its strategic Bitcoin investment and cash reserves

Fair Value:US$22089.5% undervalued

39 followersusers have followed this narrative

2 commentsusers have commented on this narrative

19 likesusers have liked this narrative

YI

yiannisz on Hesai Group ·

The First Real Lidar Winner

Fair Value:US$27.0723.5% undervalued

1 followerusers have followed this narrative

1 commentusers have commented on this narrative

3 likesusers have liked this narrative

TR

tripledub on Taiwan Semiconductor Manufacturing ·

The Most Wonderful Monopoly in the Most Dangerous Neighbourhood on Earth

Fair Value:US$38110.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

FA

FA_Trader on Northern Solar Holdings Berhad ·

Northern Solar: Explosive earnings growth makes this solar story harder to ignore

Fair Value:RM 1.968.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CG

CG86 on Bausch + Lomb ·

$BLCO & $COO The Silence BEFORE the AGM: A Retail Investor’s Timeline, Findings, and Opinion on SUSPICIOUS SILENCE!

Fair Value:US$39.2358.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FA

FA_Trader on IJM Corporation Berhad ·

IJM Corp: Has the market become too pessimistic on this blue-chip builder?

Fair Value:RM 2.715.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9829.2% undervalued

53 followersusers have followed this narrative

0 commentsusers have commented on this narrative

38 likesusers have liked this narrative

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3955.6% undervalued

40 followersusers have followed this narrative

3 commentsusers have commented on this narrative

39 likesusers have liked this narrative

RO

Robbo on Tesla ·

The academically fascinating Tesla

Fair Value:US$301.1k% overvalued

36 followersusers have followed this narrative

10 commentsusers have commented on this narrative

30 likesusers have liked this narrative