SPS Commerce (SPSC) shares have experienced a stretch of declines over the past month, with the stock trading around $80 as of the latest close. Investors are keeping a close eye on recent momentum and company fundamentals.

SPS Commerce’s share price momentum has faded considerably compared to earlier in the year, with this month’s sharp drop capping off a tough stretch. The stock has a year-to-date share price return of -56.3%, and has delivered a -54.7% total shareholder return over the past year. This recent weakness continues a longer-term trend rather than being an isolated event.

With shares now trading well below analyst targets and the company still showing profitable growth, could SPS Commerce be a bargain at current prices? Or are markets already accounting for all future upside?

Advertisement

Most Popular Narrative: 18.5% Undervalued

According to the most widely followed narrative, SPS Commerce’s fair value estimate stands notably above the last close price of $79.89. This gap between current trading levels and the calculated fair value calls for a closer look at the underlying assumptions driving this projection.

The accelerating digitalization of retail supply chains and rising compliance requirements are driving robust demand for SPS Commerce's cloud-based EDI and supply chain solutions, supporting sustained growth in new customer adds and recurring revenue. As the complexity of omni-channel retail and need for real-time, integrated supply chain analytics increases, SPS Commerce is well positioned to expand its average revenue per user (ARPU) through expanded network connections and the cross-selling of high-value products like analytics and revenue recovery solutions.

Curious what powers this bullish outlook? The fair value is built on ambitious targets for growth, profitability, and customer expansion that push the boundaries of typical projections. There is a key detail at the heart of the narrative that could surprise you; find out what it is by reading the full analysis.

However, ongoing caution from U.S. suppliers and persistent revenue pressure could still challenge the recovery and test investor confidence in the current narrative.

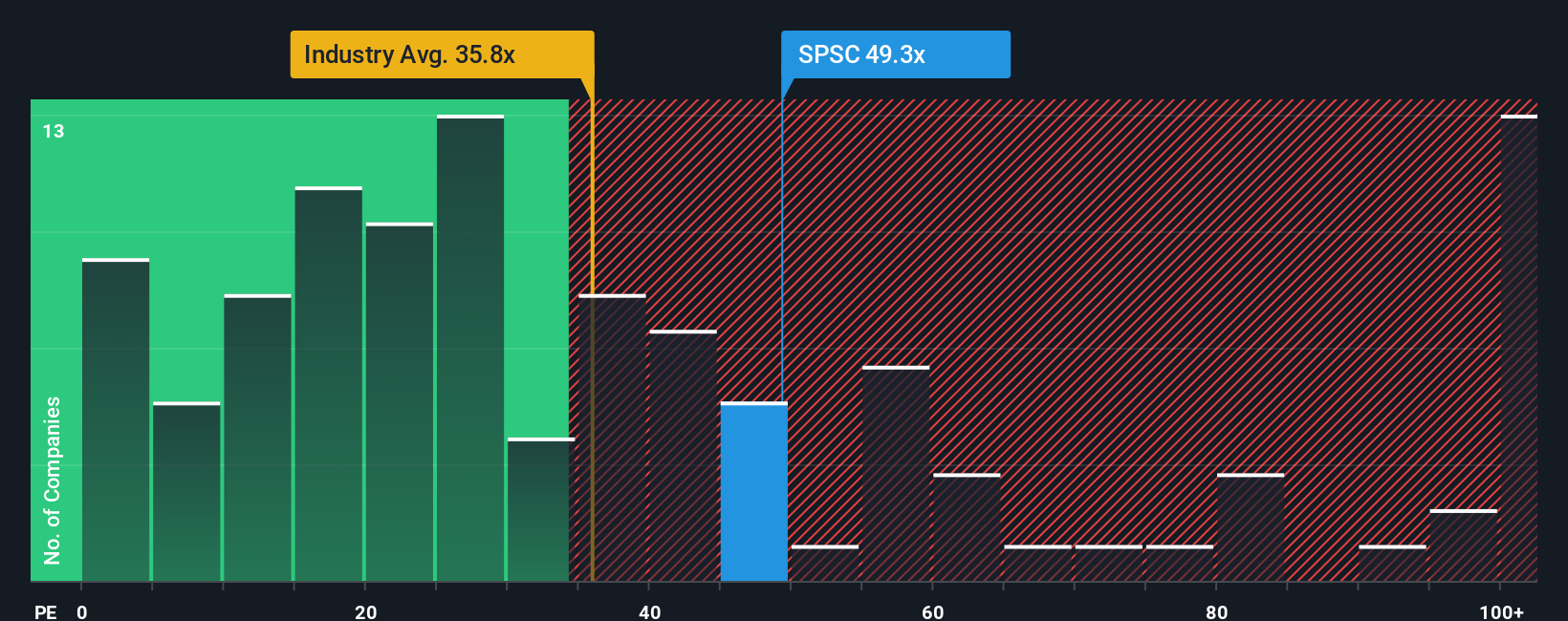

Looking from a different angle, SPS Commerce currently trades at a price-to-earnings ratio of 35.4x. This is higher than the US Software industry average of 31.2x, but still below its peers’ average of 51x. Compared to a fair ratio of 31.5x, the stock could appear a little pricey, which signals a risk that the market may reprice if expectations shift. Does this premium reflect justified growth, or is it a warning sign for value-conscious investors?

If you want to follow your own path or dig deeper into the numbers, you can easily craft your own view of SPS Commerce in just a few minutes. Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding SPS Commerce.

Looking for More Smart Investment Ideas?

Why stop here? Your next great investment could be just a click away. Take action now to uncover market movers you might regret missing.

Unlock the potential of tomorrow by checking out these 26 AI penny stocks, a resource for businesses shaping the artificial intelligence landscape.

Earn passive income and seek stability by reviewing these 18 dividend stocks with yields > 3%, a selection offering attractive dividend yields and robust fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks