Advertisement

- United States

- /

- Software

- /

- NasdaqGS:SPSC

Assessing SPS Commerce (SPSC) Valuation After Activist Pressure and Carbon6 Deal Challenges

The story around SPS Commerce (SPSC) shifted quickly after activist investor Anson disclosed a stake and began pushing for a potential sale, just months after the Carbon6 deal ran into new Amazon marketplace headwinds.

See our latest analysis for SPS Commerce.

The activist push has arrived after a bruising stretch for investors, with the share price down sharply year to date, even after a 16.1 percent 1 month share price return that hints at stabilizing sentiment and potential re rating if confidence in the strategy returns.

If this kind of catalyst driven setup interests you, it could be worth scanning for other opportunities using fast growing stocks with high insider ownership to see which fast growing, high insider ownership names are starting to build momentum.

With earnings still growing, a roughly 28 percent intrinsic discount and activists agitating for change, is SPS Commerce now mispriced value hiding in plain sight, or are investors already paying up for all the growth ahead?

Most Popular Narrative: 7.6% Undervalued

With SPS Commerce closing at $90.57 versus a narrative fair value of about $98, followers see modest upside anchored in steady, compounding fundamentals.

The analysts have a consensus price target of $152.364 for SPS Commerce based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $170.0, and the most bearish reporting a price target of just $120.0.

Curious how moderate growth, rising margins and a premium future earnings multiple can still add up to meaningful upside in a slower retail backdrop? The narrative breaks down the exact revenue path, profit expansion and valuation reset that underpin this fair value view, and the assumptions might be bolder than the current share price suggests.

Result: Fair Value of $98 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent macro uncertainty and slower supplier spending could delay revenue reacceleration, which may undermine margin expansion assumptions and limit potential multiple upside.Find out about the key risks to this SPS Commerce narrative.

Another Lens on Valuation

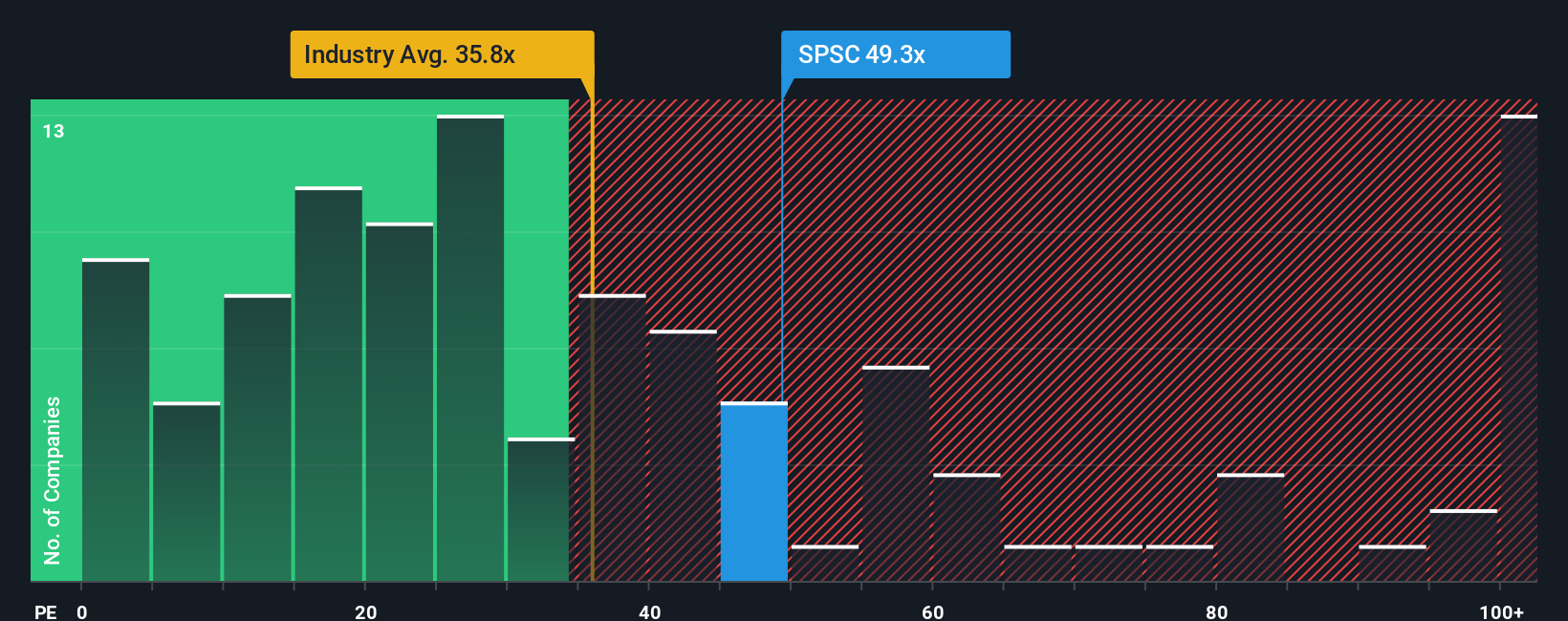

On earnings multiples, SPS Commerce looks far less forgiving. Its P E of about 40 times trails rich peers at roughly 67 times, but still sits well above the US Software industry at 31 times and our 30.8 times fair ratio, leaving limited margin for error if growth stumbles again.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own SPS Commerce Narrative

If you see the story differently or want to dig into the numbers yourself, you can build a complete view in minutes with Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding SPS Commerce.

Looking for more investment ideas?

If you want to stay ahead of the crowd, use the Simply Wall St Screener to uncover fresh opportunities before they become obvious to everyone else.

- Capture potential multi baggers early by scanning these 3623 penny stocks with strong financials that already back their tiny market caps with real financial strength.

- Position yourself for the next productivity boom by targeting these 29 healthcare AI stocks where data, software and medicine intersect to reshape patient outcomes.

- Explore reliable cash flow potential with these 13 dividend stocks with yields > 3% that combine attractive income streams with solid underlying fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:SPSC

SPS Commerce

Provides cloud-based supply chain management solutions in the United States.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Conexeu Sciences ·

This small biotech is developing technology that could potentially change how tissue is rebuilt

Fair Value:US$25.3447.6% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

HE

HedgeY on Quanta Services ·

The Picks-and-Shovels Leader of the Grid Supercycle

Fair Value:US$7101.1% undervalued

50 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

FU

FundamentalFlow on Karman Holdings ·

KRMN — Karman Space & Defense: Down 58% from Peak, Is the Market Mispricing a Hypergrowth Defense Compounder?

Fair Value:US$105.652.3% undervalued

28 followersusers have followed this narrative

2 commentsusers have commented on this narrative

13 likesusers have liked this narrative

DO

Double_Bubbler on Invinity Energy Systems ·

Invinity Energy Systems: All About That BESS

Fair Value:UK£162.2% undervalued

37 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on American Resources ·

American Resources, $263M Market Cap + 19% ReElement Stake, From Coal to Critical Minerals

Fair Value:US$557.0% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

HU

Hunter_Z on EPB Group Berhad ·

EPB: Strong Shareholder Backing, Continuous Insider Buying and Growth Opportunities Ahead

Fair Value:RM 0.548.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

YO

youwakeup on Harvest Strategy Enhanced High Income Shares ETF ·

MSTE: Turning Bitcoin Volatility Into Monthly Cash Flow

Fair Value:CA$11.7579.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7444.1% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9639.0% undervalued

57 followersusers have followed this narrative

9 commentsusers have commented on this narrative

17 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1928.5% undervalued

52 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative