Advertisement

- United States

- /

- Software

- /

- NasdaqGS:SNPS

Is Synopsys Trading Below Its True Value After Recent 20% Price Drop in 2025?

Reviewed by Bailey Pemberton

- Ever wondered if Synopsys shares are now a bargain, especially after all the recent volatility in tech stocks? This article examines where the current price stands compared to real value.

- While the stock rose an impressive 78.1% over five years, it has reversed course recently. Shares fell 3.0% in the past week, dropped 14.3% over the past month, and are now 20.5% lower year-to-date.

- The recent volatility comes amid increased discussion about large semiconductor deals and significant AI investments, putting a spotlight on core tech stocks like Synopsys. Broader shifts in investor interest, together with strong industry news, help explain some of the short-term price fluctuations.

- According to our analysis, Synopsys achieves a valuation score of 3 out of 6, indicating it is undervalued on half of the key measures. We will break down what goes into that number and, at the end, highlight a more effective approach to evaluating real stock value.

Find out why Synopsys's -28.1% return over the last year is lagging behind its peers.

Approach 1: Synopsys Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates a company's intrinsic value by projecting its future cash flows and discounting them back to today, reflecting the time value of money. This approach is popular for evaluating tech stocks like Synopsys, where future growth can make up a substantial portion of total value.

Synopsys reported a current Free Cash Flow of approximately $1.26 Billion. According to analyst estimates, the company’s Free Cash Flow is projected to continue rising annually, reaching $5.26 Billion by 2030. While direct analyst projections are available for the next five years, projections beyond that are carefully extrapolated to present a clearer long-term picture.

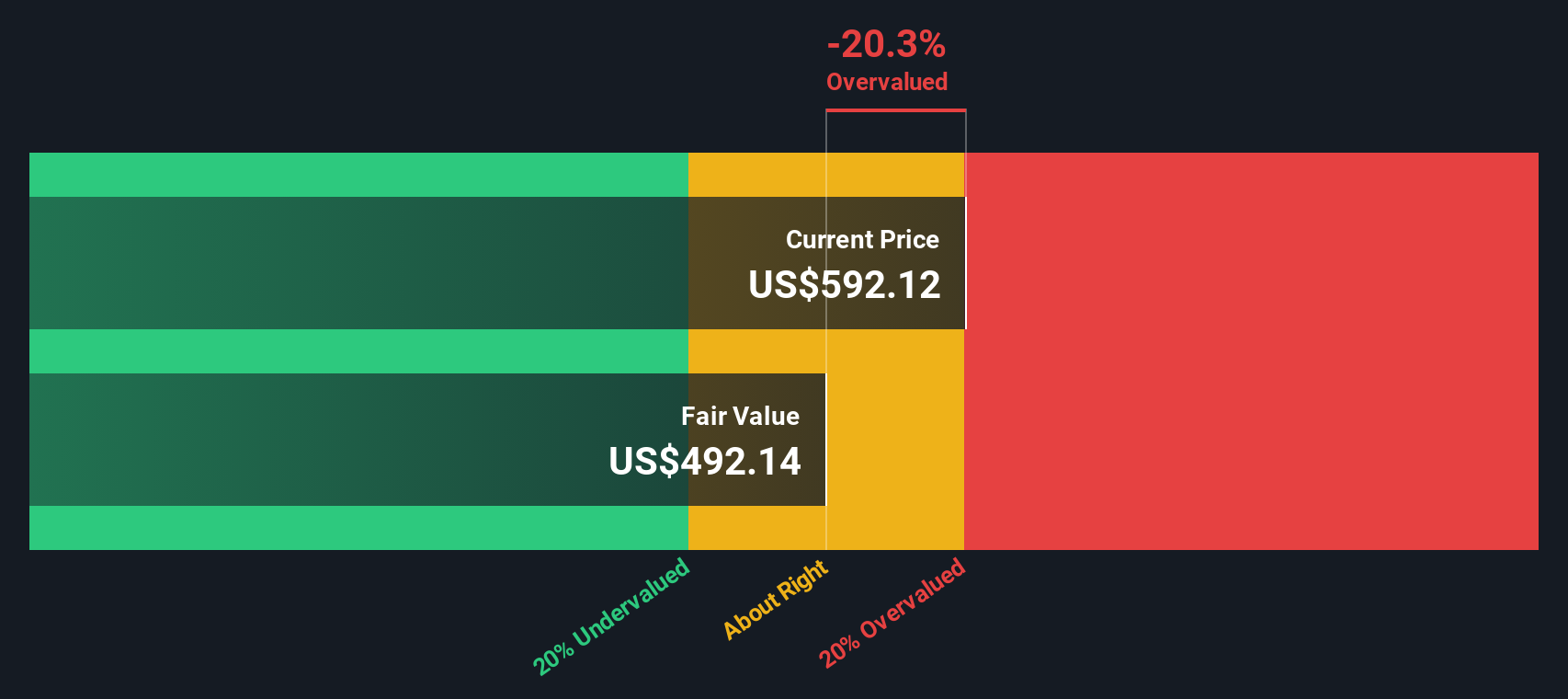

By applying the 2 Stage Free Cash Flow to Equity model and discounting the cash flow forecasts accordingly, Synopsys’ intrinsic value is estimated at $469.68 per share. This suggests the stock is currently trading at an 18.3% discount to its calculated fair value, indicating it appears significantly undervalued based on this model.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Synopsys is undervalued by 18.3%. Track this in your watchlist or portfolio, or discover 909 more undervalued stocks based on cash flows.

Approach 2: Synopsys Price vs Earnings (PE)

For profitable companies like Synopsys, the Price-to-Earnings (PE) ratio is widely used because it directly compares a company's market price to its per-share earnings. This makes it a simple way to assess whether a stock is cheap or expensive relative to its profits. Generally, a higher PE ratio reflects greater growth expectations or lower risk, while a lower PE can signal modest prospects or higher risk. As a result, "fair value" largely depends on these factors.

Synopsys currently trades at a PE ratio of 61.1x. For context, the average PE ratio for software industry peers stands at 29.96x, and the peer average is 67.79x. On this basis, Synopsys appears notably more expensive than the broader industry but sits just below its immediate peer group.

However, rather than just comparing to sector or peer averages, Simply Wall St uses a proprietary "Fair Ratio" for each stock. For Synopsys, this Fair Ratio is 45.33x and reflects a blend of the company’s earnings growth outlook, its profit margins, industry dynamics, market cap, and risk factors. It provides a more nuanced benchmark for valuation than blunt peer or industry comparisons.

Comparing Synopsys’s actual PE of 61.1x with its Fair Ratio of 45.33x suggests the shares are trading above what would be considered fair given all these underlying factors. This points to Synopsys being potentially overvalued by this key metric.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1412 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Synopsys Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is your personal story of what you think will happen for a company like Synopsys. You combine your own view of the business, such as how fast it might grow, what margins it can sustain, or what risks matter most, with financial forecasts to arrive at your fair value estimate.

Unlike traditional models, Narratives connect the company's evolving story directly to financial outcomes, letting you update assumptions as new facts, like earnings or news, arrive. On Simply Wall St’s Community page, millions of investors can build and share Narratives, making it a practical and accessible tool for anyone seeking to make smarter buy or sell decisions by directly comparing their own fair value to the market price.

Narratives update dynamically, so your investment thesis is always anchored to the latest data. For Synopsys, some investors are bullish, focusing on AI-driven growth, the Ansys integration, and improved margins, driving higher price targets. Others stress uncertain IP segment recovery, China risks, or execution challenges, leading to more conservative valuations. Narratives make it simple to see how different viewpoints shape what each investor thinks the stock is really worth.

Do you think there's more to the story for Synopsys? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:SNPS

Synopsys

Provides design IP solutions in the semiconductor and electronics industries.

Reasonable growth potential with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

VA

valuebull on Eva Live ·

Is this the AI replacing marketing professionals?

Fair Value:US$7.4349.5% undervalued

44 followersusers have followed this narrative

0 commentsusers have commented on this narrative

10 likesusers have liked this narrative

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3956.3% undervalued

22 followersusers have followed this narrative

3 commentsusers have commented on this narrative

23 likesusers have liked this narrative

RO

Robbo on Tesla ·

The academically fascinating Tesla

Fair Value:US$301.1k% overvalued

29 followersusers have followed this narrative

5 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AH

AHaron on Eli Lilly ·

Eli Lilly: A Pipeline-Driven Growth Story Trading 30% Below What the Business Is Actually Worth

Fair Value:US$1.48k37.7% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

OS

osborne820 on Grid Metals ·

Grid Metals will see a transformative 21.5x future PE change

Fair Value:CA$0.7584.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FA

FA_Trader on Meta Bright Group Berhad ·

Meta Bright: Rising fuel costs could gradually accelerate the shift to EVs and rooftop solar

Fair Value:RM 0.1720.6% undervalued

1 followerusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

AL

alegget on Walt Disney ·

The happiest company on Earth, also perennially misunderstood.

Fair Value:US$134.6328.4% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Popular Narratives

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9830.9% undervalued

51 followersusers have followed this narrative

0 commentsusers have commented on this narrative

36 likesusers have liked this narrative

PD

pdixit1 on Vertiv Holdings Co ·

The Infrastructure AI Cannot Be Built Without

Fair Value:US$408.6438.7% undervalued

40 followersusers have followed this narrative

3 commentsusers have commented on this narrative

18 likesusers have liked this narrative

ZA

ZayaanS on Pro Medicus ·

Pro Medicus: The Market Is Confusing a Lumpy Quarter With a Broken Business

Fair Value:AU$196.7837.0% undervalued

34 followersusers have followed this narrative

7 commentsusers have commented on this narrative

21 likesusers have liked this narrative