- United States

- /

- Software

- /

- NasdaqGS:SAIL

Reassessing SailPoint (SAIL) Valuation After a Recent Share Price Rebound

Reviewed by Simply Wall St

SailPoint (SAIL) shares have quietly climbed about 12% over the past month even as three month performance remains weak, setting up an interesting reset in expectations around its identity security business.

See our latest analysis for SailPoint.

Zooming out, SailPoint’s 30 day share price return of about 12% contrasts with a still negative year to date share price return. This hints that sentiment is stabilising rather than fully turning bullish just yet.

If SailPoint’s recent move has your radar up, this could be a good moment to explore other high growth tech opportunities using our high growth tech and AI stocks.

With shares still below analyst targets despite solid double digit revenue growth, the recent bounce raises a key question: is SailPoint a misunderstood value in identity security, or is the market already pricing in its next leg of growth?

Price-to-Sales of 11.6x: Is it justified?

SailPoint’s latest close of $20.98 implies a rich valuation, with the shares trading on a price to sales ratio of 11.6 times revenue.

The price to sales multiple compares the company’s market value to its annual sales, a common yardstick for fast growing but unprofitable software names like SailPoint. At 11.6 times, investors are paying a premium today for each dollar of current revenue, effectively embedding expectations of strong future growth and eventual operating leverage into the share price.

However, that premium looks stretched when lined up against both peers and a fair value yardstick. The 11.6 times multiple sits well above the peer group average of 7.7 times and far beyond the estimated fair price to sales ratio of 7 times, suggesting the market could ultimately re rate the shares closer to that lower level if growth or profitability progress falls short.

Explore the SWS fair ratio for SailPoint

Result: Price-to-Sales of 11.6x (OVERVALUED)

However, risks remain if identity security spending slows or SailPoint struggles to translate rapid revenue growth into sustainable profitability, which could pressure today’s premium valuation.

Find out about the key risks to this SailPoint narrative.

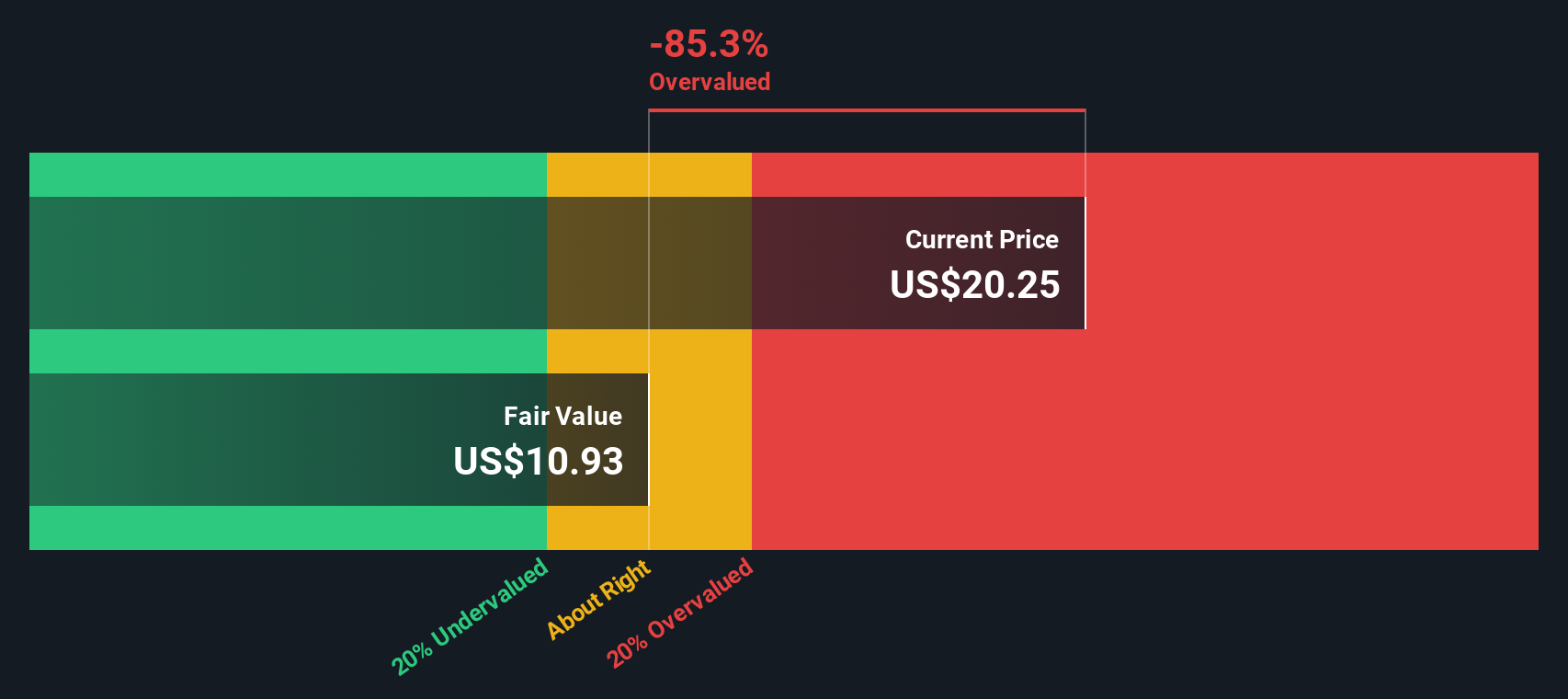

Another Take, Our DCF View

While the price to sales ratio paints SailPoint as expensive, our DCF model is even more cautious, pointing to a fair value of about $11.92 per share, well below the current $20.98. If both signals lean negative, is the market overlooking risk or betting on a sharper growth inflection?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out SailPoint for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 916 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own SailPoint Narrative

If this view does not quite match your own or you prefer hands on research, you can build a custom narrative in just minutes: Do it your way.

A great starting point for your SailPoint research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Before markets move on without you, put Simply Wall St’s powerful screener to work and line up your next set of high conviction opportunities today.

- Capture potential turnaround stories by targeting quality names trading below intrinsic value with these 916 undervalued stocks based on cash flows.

- Supercharge your growth watchlist by focusing on innovation driven businesses at the forefront of machine learning and automation using these 24 AI penny stocks.

- Lock in reliable income streams by scanning for companies with attractive yields and resilient cash flows via these 13 dividend stocks with yields > 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:SAIL

SailPoint

SailPoint, Inc. delivers solutions to enable identity security for the enterprise in the Americas, Europe, the Middle East, Africa, and the Asia-Pacific.

Excellent balance sheet with very low risk.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion