Advertisement

- United States

- /

- Software

- /

- NasdaqGS:PRGS

Is It Time To Reconsider Progress Software (PRGS) After Its 1 Year Share Price Slump?

Reviewed by Bailey Pemberton

- If you are wondering whether Progress Software is attractively priced or not, this article will walk through what the numbers are really saying about its current valuation.

- The stock closed at US$40.92, with returns of 3.6% decline over 7 days, 4.7% decline over 30 days, 0.4% decline year to date, 28.6% decline over 1 year, 26.2% decline over 3 years, and 1.7% gain over 5 years. This gives you a sense of how sentiment around risk and opportunity has shifted over different timeframes.

- Recent coverage of Progress Software has focused on its role as a provider of application development and infrastructure software, as investors reassess where it fits within the broader software sector. This context matters because moves in the share price are often tied to how investors feel about the resilience and relevance of its product portfolio.

- On Simply Wall St's valuation checklist, Progress Software scores a 5 out of 6 for being assessed as undervalued. Next, we will walk through the main valuation methods behind that score and then finish with a way to look at value that goes beyond any single model.

Find out why Progress Software's -28.6% return over the last year is lagging behind its peers.

Approach 1: Progress Software Discounted Cash Flow (DCF) Analysis

A DCF model takes estimates of a company’s future cash flows and discounts them back to today using a required return, aiming to translate those future dollars into a single present value per share.

For Progress Software, the model used is a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The latest twelve month free cash flow is about $228.5 million. Analysts provide several years of explicit forecasts, and Simply Wall St then extends those projections, with free cash flow for 2030 estimated at $334.35 million and further ten year projections stepping up modestly from there.

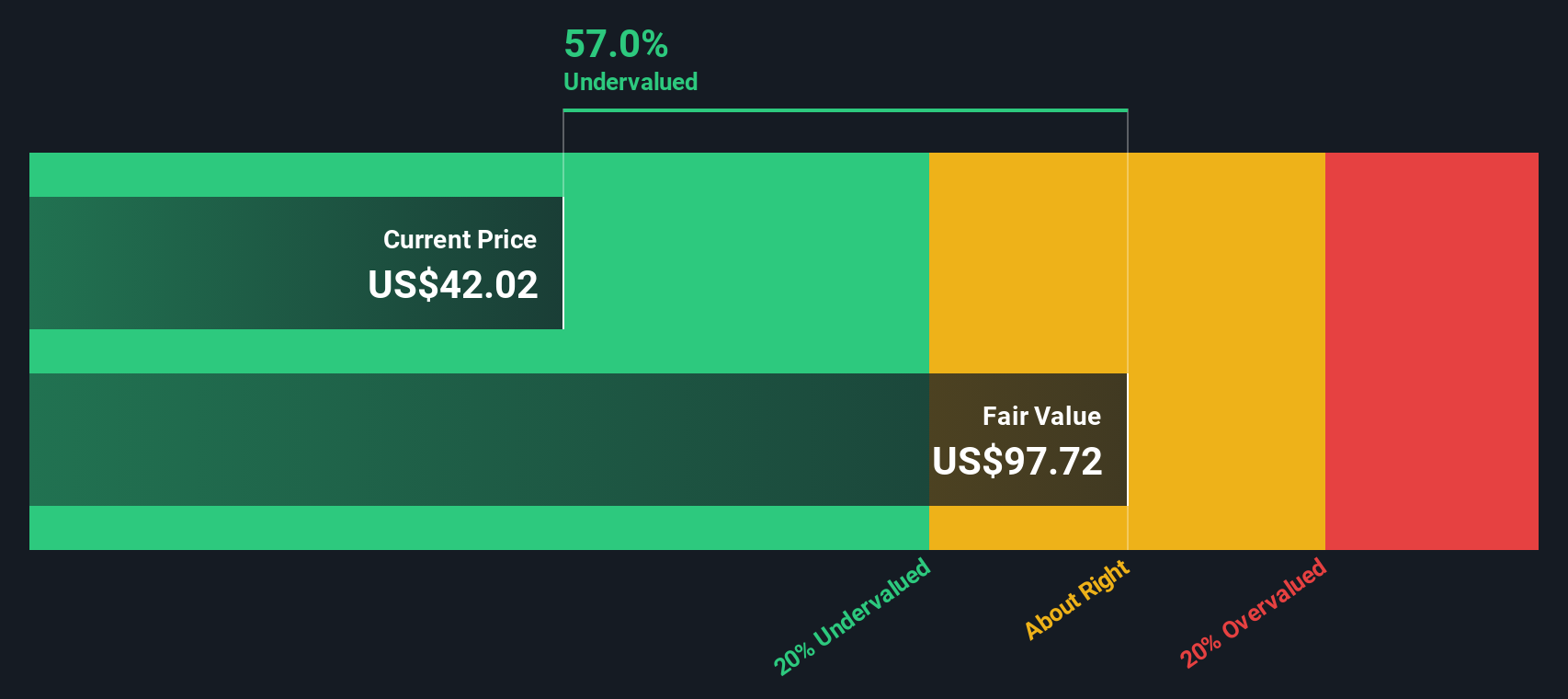

Putting all of those projected cash flows together, the DCF model arrives at an estimated intrinsic value of about US$89.94 per share. Compared with the recent share price of US$40.92, this implies the stock is trading at about a 54.5% discount to that DCF estimate. This indicates a material valuation gap based on these cash flow assumptions.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Progress Software is undervalued by 54.5%. Track this in your watchlist or portfolio, or discover 868 more undervalued stocks based on cash flows.

Approach 2: Progress Software Price vs Earnings

For a profitable company like Progress Software, the P/E ratio is a useful way to think about what you are paying for each dollar of current earnings. Investors usually accept higher P/E ratios when they expect stronger earnings growth or see lower risk, and look for lower P/E ratios when growth expectations are more modest or risks feel higher.

Progress Software currently trades on a P/E of 23.56x. That sits below both the Software industry average P/E of 28.00x and the peer average of 27.27x, which suggests the market is applying a lower earnings multiple than it does to many comparable names.

Simply Wall St’s Fair Ratio for Progress Software is 24.46x. This is a proprietary estimate of what the P/E might be given factors such as the company’s earnings growth profile, its industry, profit margins, market cap and specific risks. Because it adjusts for these company level traits, the Fair Ratio can be more tailored than a simple comparison with peers or the broad industry, which treat all companies as if they deserve similar multiples.

With the current P/E of 23.56x versus a Fair Ratio of 24.46x, Progress Software appears modestly undervalued on this earnings based check.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1417 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Progress Software Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to connect your view of Progress Software’s business with the numbers behind it.

A Narrative is your story for the company, where you spell out what you think its future revenue, earnings and margins might look like, and then link that forecast to a fair value estimate.

On Simply Wall St, Narratives sit inside the Community page and are designed to be easy to use. This means you can move from story, to forecast, to fair value without needing to build your own spreadsheet.

Narratives help you compare each Narrative’s Fair Value to the current share price. They automatically refresh when new information such as news or earnings is added to the platform.

For example, one Progress Software Narrative might assume a much higher fair value than the current price. Another might assume a lower fair value than the current price. This shows how different investors can look at the same company and reach very different conclusions.

Do you think there's more to the story for Progress Software? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:PRGS

Progress Software

Provides software products that develops, deploys, and manages artificial intelligence (AI) powered applications and digital experiences in the United States and internationally.

Undervalued with very low risk.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0775.1% undervalued

120 followersusers have followed this narrative

1 commentusers have commented on this narrative

21 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9822.7% undervalued

39 followersusers have followed this narrative

0 commentsusers have commented on this narrative

32 likesusers have liked this narrative

KO

Kouj on CSL ·

CSL: The Dip Is the Opportunity

Fair Value:AU$1559.0% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative

GA

GavrielH on DHT Holdings ·

DHT Holdings, inc: Strait of Hormuz Risk Amidst US-Israel vs Iran Tensions Spikes VLCC Rates.

Fair Value:US$3653.2% undervalued

12 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

Recently Updated Narratives

VE

Vestra on VEON ·

VEON Ltd. (VEON): The Frontier "Digital Operator" and the 84% Hypergrowth Inflection

Fair Value:US$67.825.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on Salesforce ·

Salesforce (CRM): The "Agentic Work Unit" Revolution and the $50 Billion Capital Pivot

Fair Value:US$34143.5% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on NVIDIA ·

NVIDIA (NVDA): The "Agentic AI" Pivot and the $2 Billion Sovereign Cloud Alliance

Fair Value:US$237.524.1% undervalued

24 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.378.4% undervalued

53 followersusers have followed this narrative

3 commentsusers have commented on this narrative

27 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59633.6% undervalued

1308 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9822.7% undervalued

39 followersusers have followed this narrative

0 commentsusers have commented on this narrative

32 likesusers have liked this narrative