- United States

- /

- Software

- /

- NasdaqGS:NTNX

Nutanix (NasdaqGS:NTNX) Shares Climb 16% Following Q2 Earnings With Revenue Reaching US$655M

Reviewed by Simply Wall St

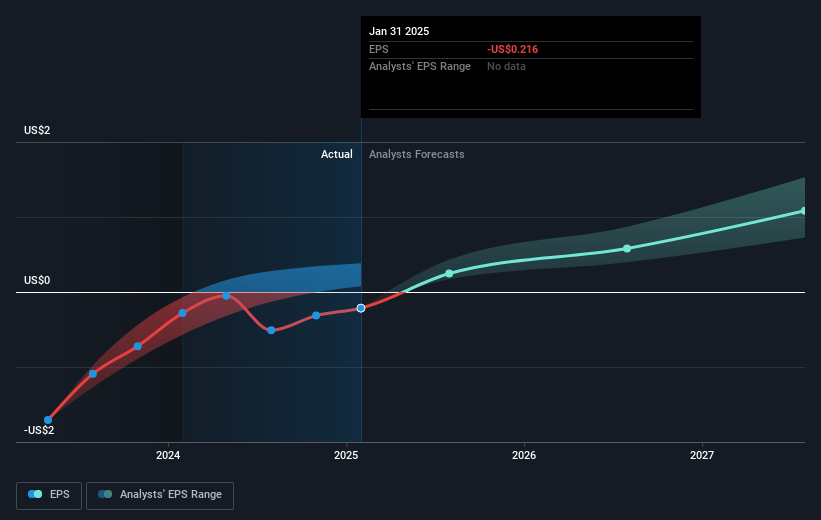

Nutanix (NasdaqGS:NTNX) recently reported positive earnings results for Q2 2025, with revenue increasing to $655 million and net income growing to $56 million. This financial performance likely played a role in the company's share price rising 16% over the last quarter. Additionally, the announcement of a $500 million credit facility adds financial flexibility, which may have supported investor confidence. Despite broader market concerns about economic conditions and slight declines in major indexes like the Nasdaq, Nutanix's positive forward guidance for Q3 and 2025 suggests stable outlook that may have helped buffer against the recent market volatility. With the Nasdaq experiencing a 1% drop amidst economic worries, Nutanix's strong quarterly performance and strategic corporate developments could be significant drivers in its stock's robust quarterly uptick.

Dig deeper into the specifics of Nutanix here with our thorough analysis report.

The last five years have seen Nutanix's total shareholder return surge by 339.37%, showcasing remarkable growth. This impressive performance can be partly attributed to the company's regular strategic initiatives, such as the share buyback program that concluded in October 2024, where Nutanix repurchased approximately 2.92 million shares for US$151.14 million. The recent expansion of their collaboration with Amazon Web Services in November 2024 to facilitate cloud migration has also likely played a role in driving investor interest.

Adding to these growth strategies, Nutanix has focused on enhancing its product offerings. Noteworthy developments include the launch of Nutanix Enterprise AI in November 2024, aimed at supporting AI workloads across diverse environments. Additionally, significant financial moves, such as securing a US$500 million credit facility in February 2025, have strengthened Nutanix's financial flexibility. Over the past year, Nutanix's return has exceeded both the market and industry averages, setting itself apart in a competitive landscape.

- Discover whether Nutanix is fairly priced, undervalued, or overvalued in our comprehensive valuation breakdown.

- Uncover the uncertainties that could impact Nutanix's future growth—read our risk evaluation here.

- Are you invested in Nutanix already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Nutanix might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:NTNX

Nutanix

Provides an enterprise cloud platform in North America, Europe, the Asia Pacific, the Middle East, Latin America, and Africa.

High growth potential and fair value.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Q3 Outlook modestly optimistic

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

MicroVision will explode future revenue by 380.37% with a vision towards success

Trending Discussion