Advertisement

- United States

- /

- Software

- /

- NasdaqGS:NTNX

Nutanix, Inc.'s (NASDAQ:NTNX) Share Price Could Signal Some Risk

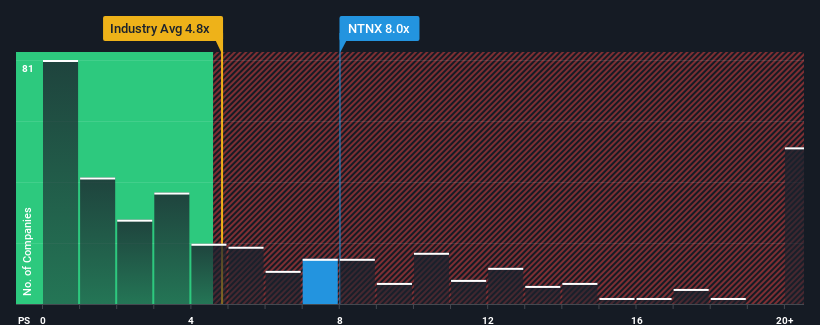

Nutanix, Inc.'s (NASDAQ:NTNX) price-to-sales (or "P/S") ratio of 8.1x might make it look like a strong sell right now compared to the Software industry in the United States, where around half of the companies have P/S ratios below 4.8x and even P/S below 1.7x are quite common. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

View our latest analysis for Nutanix

What Does Nutanix's P/S Mean For Shareholders?

There hasn't been much to differentiate Nutanix's and the industry's revenue growth lately. Perhaps the market is expecting future revenue performance to improve, justifying the currently elevated P/S. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Nutanix.How Is Nutanix's Revenue Growth Trending?

There's an inherent assumption that a company should far outperform the industry for P/S ratios like Nutanix's to be considered reasonable.

Taking a look back first, we see that the company grew revenue by an impressive 15% last year. The strong recent performance means it was also able to grow revenue by 54% in total over the last three years. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Turning to the outlook, the next three years should generate growth of 15% each year as estimated by the analysts watching the company. That's shaping up to be materially lower than the 20% per year growth forecast for the broader industry.

With this information, we find it concerning that Nutanix is trading at a P/S higher than the industry. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. There's a good chance these shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with the growth outlook.

The Final Word

Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

Despite analysts forecasting some poorer-than-industry revenue growth figures for Nutanix, this doesn't appear to be impacting the P/S in the slightest. The weakness in the company's revenue estimate doesn't bode well for the elevated P/S, which could take a fall if the revenue sentiment doesn't improve. This places shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

There are also other vital risk factors to consider and we've discovered 3 warning signs for Nutanix (1 doesn't sit too well with us!) that you should be aware of before investing here.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if Nutanix might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:NTNX

Nutanix

Provides an enterprise cloud platform in North America, Europe, the Asia Pacific, the Middle East, Latin America, and Africa.

Undervalued with high growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value US$282.83|31.8% undervalued

BL

Community Contributor

Planet Labs: At The Heart Of The Emerging New Space Boom

Fair Value US$11.31|44.7% undervalued

AN

Community Contributor

Exxon in Guyana 5 year forecast Low $135 to High $189

Fair Value US$174.00|35.8% undervalued

AG

Community Contributor