Advertisement

- United States

- /

- Software

- /

- NasdaqGS:MTLS

These 4 Measures Indicate That Materialise (NASDAQ:MTLS) Is Using Debt Safely

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Materialise NV (NASDAQ:MTLS) does carry debt. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for Materialise

How Much Debt Does Materialise Carry?

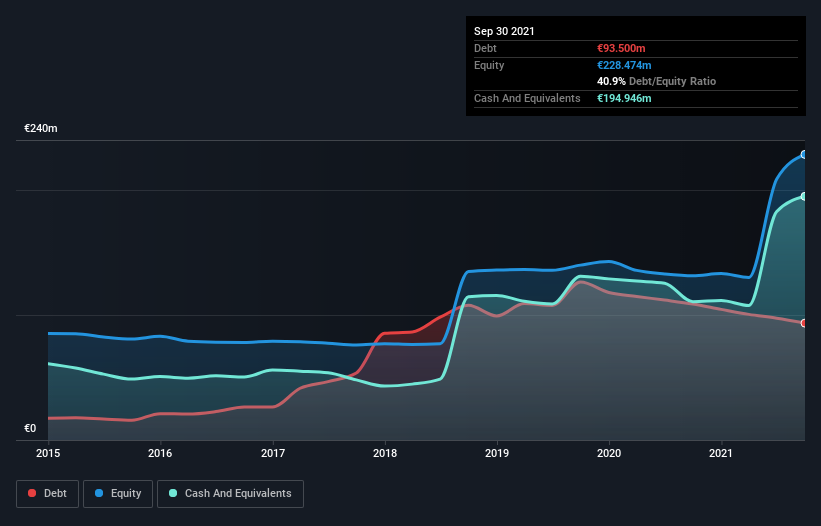

You can click the graphic below for the historical numbers, but it shows that Materialise had €93.5m of debt in September 2021, down from €108.7m, one year before. However, it does have €194.9m in cash offsetting this, leading to net cash of €101.4m.

How Strong Is Materialise's Balance Sheet?

According to the last reported balance sheet, Materialise had liabilities of €92.1m due within 12 months, and liabilities of €94.3m due beyond 12 months. On the other hand, it had cash of €194.9m and €38.5m worth of receivables due within a year. So it can boast €47.1m more liquid assets than total liabilities.

This short term liquidity is a sign that Materialise could probably pay off its debt with ease, as its balance sheet is far from stretched. Succinctly put, Materialise boasts net cash, so it's fair to say it does not have a heavy debt load!

Even more impressive was the fact that Materialise grew its EBIT by 13,998% over twelve months. If maintained that growth will make the debt even more manageable in the years ahead. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Materialise's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. While Materialise has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the last three years, Materialise actually produced more free cash flow than EBIT. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Summing up

While it is always sensible to investigate a company's debt, in this case Materialise has €101.4m in net cash and a decent-looking balance sheet. The cherry on top was that in converted 291% of that EBIT to free cash flow, bringing in €22m. So is Materialise's debt a risk? It doesn't seem so to us. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. Be aware that Materialise is showing 3 warning signs in our investment analysis , you should know about...

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:MTLS

Materialise

Provides additive manufacturing and medical software tools, and 3D printing services in the Americas, Europe, Africa, and the Asia-Pacific.

Excellent balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

A Quality Compounder Marked Down on Overblown Fears

Fair Value US$120.72|62.4% undervalued

BA

Community Contributor

Wyndham Continues Global Expansion with 19% Ancillary Revenue Growth

Fair Value US$105.80|19.2% undervalued

ZW

Community Contributor