- United States

- /

- Software

- /

- NasdaqGS:MSFT

Microsoft (MSFT) Settles Patent Lawsuit With Virtru Over Data Encryption Technology

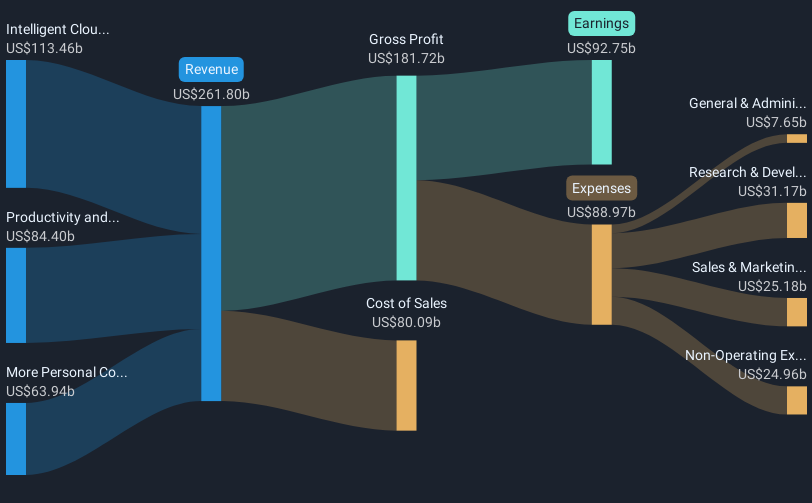

Microsoft (MSFT) recently marked a 9% rise over the last quarter, a movement influenced primarily by its legal settlement with Virtru Corporation over patent infringement claims. This event, coupled with strong earnings growth reflecting a significant revenue and net income boost, underpinned market confidence. Furthermore, Microsoft's announcement of a continued dividend and substantial buyback efforts added support to its share price. The company's partnerships, like the extended collaboration with the NFL, affirmed ongoing innovation. In a flat broader market, these developments added weight to Microsoft's positive performance.

Microsoft has 1 possible red flag we think you should know about.

The recent legal settlement with Virtru Corporation and Microsoft's commitment to dividends and buyback initiatives are significant in shaping investor sentiment and potentially bolstering the company's future performance. Over the past five years, Microsoft's total shareholder return was 133.19%, showcasing strong long-term growth and robust shareholder value appreciation. This contrasts with its 1-year performance, which outpaced the broader US market but fell short of the software industry average return.

Microsoft's forward-looking initiatives in AI and cloud services could see an uptick after the legal resolution, supporting revenue streams like Azure AI and enhancing enterprise cloud solutions. Microsoft's share price, currently at $504.26, shows potential relative to the consensus price target of $614.60, implying a possible upside. Earnings forecasts also point to substantial growth, considering this context of resolved legal proceedings and strategic focus, although analysts expect earnings to grow slower than the US market annually. This reinforces Microsoft's appeal to long-term investors looking for stable revenue and profit expansion.

Evaluate Microsoft's historical performance by accessing our past performance report.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:MSFT

Microsoft

Develops and supports software, services, devices, and solutions worldwide.

Very undervalued with outstanding track record and pays a dividend.

Similar Companies

Market Insights

Weekly Picks

This small biotech is developing technology that could potentially change how tissue is rebuilt

The Picks-and-Shovels Leader of the Grid Supercycle

KRMN — Karman Space & Defense: Down 58% from Peak, Is the Market Mispricing a Hypergrowth Defense Compounder?

Invinity Energy Systems: All About That BESS

Recently Updated Narratives

Strong in favor of diversity in value portfolio

Relatively mispriced taken into account its intrinsic growth profile, providing a defensive, cash-generative entry point for investors

Nova Ljubljanska Banka d.d. future looks bright with a profit margin change of 38%

Popular Narratives

Investment Analysis (May 2026)

Adobe: A Probabilistic Case for Undervaluation

Honeywell - The Demand-Side of the AI Infrastructure

Trending Discussion